US core PCE set to show continued disinflation trend, reinforcing Federal Reserve easing cycle

- The core Personal Consumption Expenditures Price Index is seen rising 0.2% MoM and 2.7% YoY in August.

- Markets have already priced in near 50 bps of easing in the next two Federal Reserve meetings.

- A firm PCE result is unlikely to move the Fed’s stance on policy.

The United States Bureau of Economic Analysis (BEA) is set to release the significant Personal Consumption Expenditures (PCE) Price Index, which is the Federal Reserve’s preferred measure of inflation, on Friday at 12:30 GMT.

While this PCE inflation data may influence the very-near-term trajectory of the US Dollar (USD), it is highly unlikely to alter the Fed’s course regarding its interest-rate path.

Anticipating the PCE: Insights into the Federal Reserve's key inflation metric

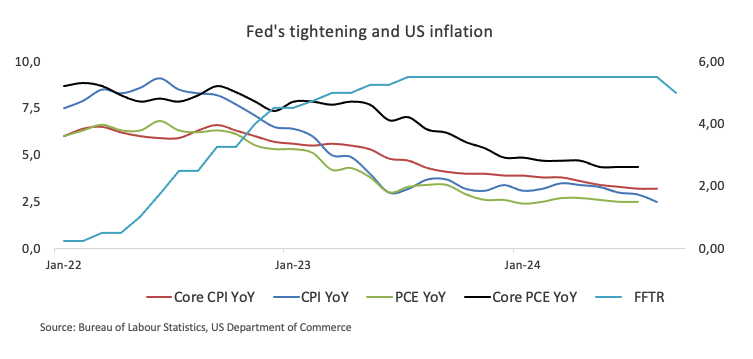

The core PCE Price Index is projected to rise by 0.2% in August compared to the previous month, aligning with July’s figures. Over the last twelve months, the core PCE is expected to increase by 2.7%, slightly up from July’s 2.6% rise.

This core PCE Price Index, which excludes the more volatile food and energy categories, plays a crucial role in shaping market expectations for the Federal Reserve's interest-rate outlook. Both the central bank and market participants closely monitor this measure, as it is not distorted by base effects and provides a clearer view of underlying inflation by excluding unstable components.

As for the headline PCE, consensus forecasts suggest that the downward trend will persist in August, with the monthly PCE expected to rise by 0.1% (down from 0.2% previously) and an annual increase of 2.3% (down from 2.5% previously).

Previewing the PCE inflation report, analysts at TD Securities argued: “Core PCE inflation likely stayed under control in August, with prices advancing at a soft 0.15% m/m pace. Given shelter price strength acted as a key driver of core CPI inflation, the core PCE will not increase as much. Headline PCE inflation likely printed an also soft 0.10% m/m. Separately, we expect personal spending to moderate, rising 0.2% m/m and 0.1% m/m in real terms.”

How will the Personal Consumption Expenditures Price Index affect EUR/USD?

The Greenback navigates the lower end of its multi-month range south of the 101.00 barrier, with initial contention around 100.20 so far.

Following the Fed’s jumbo rate cut at its September 17-18 gathering, investors now see around 50 basis points of easing for the remainder of the year, and between 100 and 125 basis points by the end of 2025.

A surprise at the PCE release should barely influence the Dollar’s price action, as market participants have already shifted their attention to next week’s crucial Nonfarm Payrolls amids the broader Fed’s shift to the labour market in detriment of the progress around inflation.

According to Pablo Piovano, Senior Analyst at FX Street.com, “further upside impulse should motivate EUR/USD to confront its year-to-date peak of 1.1214 (September 25). Once this region is cleared, spot could set sails to the 2023 high of 1.1275 recorded on July 18.”

“On the downside, the September low at 1.1001 (September 11) appears to be reinforced by the provisional 55-day SMA at 1.1009 ahead of the weekly low of 1.0949 (August 15)," Pablo adds.

Finally, Pablo suggests that “while above the 200-day SMA of 1.0873, the pair’s constructive outlook should remain unchanged.”

Economic Indicator

Personal Consumption Expenditures - Price Index (MoM)

The Personal Consumption Expenditures (PCE), released by the US Bureau of Economic Analysis on a monthly basis, measures the changes in the prices of goods and services purchased by consumers in the United States (US).. The MoM figure compares prices in the reference month to the previous month. Price changes may cause consumers to switch from buying one good to another and the PCE Deflator can account for such substitutions. This makes it the preferred measure of inflation for the Federal Reserve. Generally speaking, a high reading is bullish for the US Dollar (USD), while a low reading is bearish.

Read more.Last release: Fri Aug 30, 2024 12:30

Frequency: Monthly

Actual: 0.2%

Consensus: 0.2%

Previous: 0.1%

Source: US Bureau of Economic Analysis

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Artigos Recomendados