TradingKey - The year 2025 started off on a pretty solid footing for investors with the key indices in the US – the S&P 500 Index and the tech-focused Nasdaq Composite Index – both posting gains in the first few days of trading. That followed on from some huge double-digit gains for 2023 and 2024.

However, investor sentiment turned rather sour yesterday (7 January) after the release of the latest key economic data. As a result, the S&P 500 Index finished the day down 1.1% and the Nasdaq did even worse, falling 1.9% for the day.

Here’s what investors should know about what caused the most recent sell-off and whether investors should be worried going forward.

Hot data spark market sell-off

Right now, the market is laser focused on economic data coming out of the world’s largest economy. That’s because these data points are guiding crucial decisions on where interest rates are headed in the US.

Why? Well, the US Federal Reserve (Fed) keeps telling the market it is “data dependent” when it comes to whether the central bank will cut or hold interest rates steady.

As investors saw with the sell-off immediately following the Fed’s FOMC meeting in December, markets do not like the prospect of higher interest rates. And that’s, unfortunately, exactly the message they got with yesterday’s data.

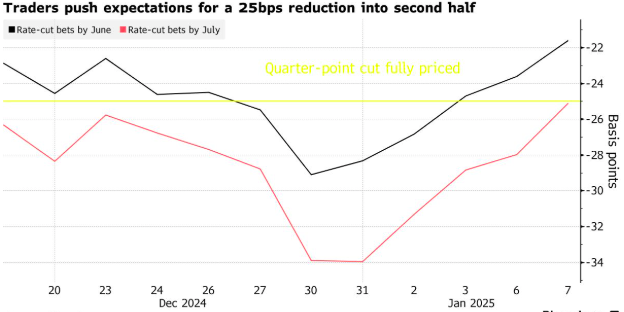

Likelihood of Fed rate cuts pushed out

On Tuesday, two key data points – the Job Openings and Labor Turnover Survey (JOLTS) and services PMI – both came in hotter than the market was expecting.

The Bureau of Labor Statistics (BLS) reported that job openings rose to just over 8.09 million as of the last business day of November 2024, higher than the 7.7 million that the market was expecting.

The big surprise was from the ISM services purchasing managers index (PMI) that increased to 54.1 in December, from 52.1 in November. Remember, any figure above 50 indicates expansion but the real story was buried in the rise in the prices paid index (or input prices) that jumped to 64.4 in December from 58.2 in November.

What did all that mean? Well, hotter input prices and a robust labour market are both giving the Fed the signal that it may not need to cut interest rates by all that much in the near term. The market has now priced in just one 25-basis point (bp) cut in the first half of this year.

Fed rate cut projections pushed back

Source: Bloomberg

Indeed, the odds of a January interest rate cut at the next FOMC on 28-29 January fell to just 4.8%, from 8.6%, after the data released, according to the CME FedWatch Tool.

What does it mean for investors?

While the sell-off was rather sharp in the equity markets, there was actually more action in the bond markets as bonds sold off. The US 10-year Treasury yield hit 4.69%, its highest since April 2024 and the US 30-year yield hit a 12-month high of 4.91%.

With the Fed looking increasingly likely to keep rates steady in the foreseeable future, both stock and bond markets sold off. That was particularly true for tech stocks that have enjoyed a strong run up and are typically the first ones to get punished when the market thinks rate cuts are further away than initially expected.

The large cap names that made headlines yesterday with sizable falls included Tesla Inc (NASDAQ: TSLA), which was down 4.1%, and chip giant Nvidia Corp (NASDAQ: NVDA), which fell 6.2%. For investors, the next big data release comes on Friday (10 January) morning, when the latest US employment report will be released.

If that comes in much higher than expected, then investors should brace themselves for some more volatility on Friday at the market open.

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.