Google’s AI Reset: Why Q1 Could Trigger a Valuation Rerate

Gemini Fuels Google’s Second Growth Driver

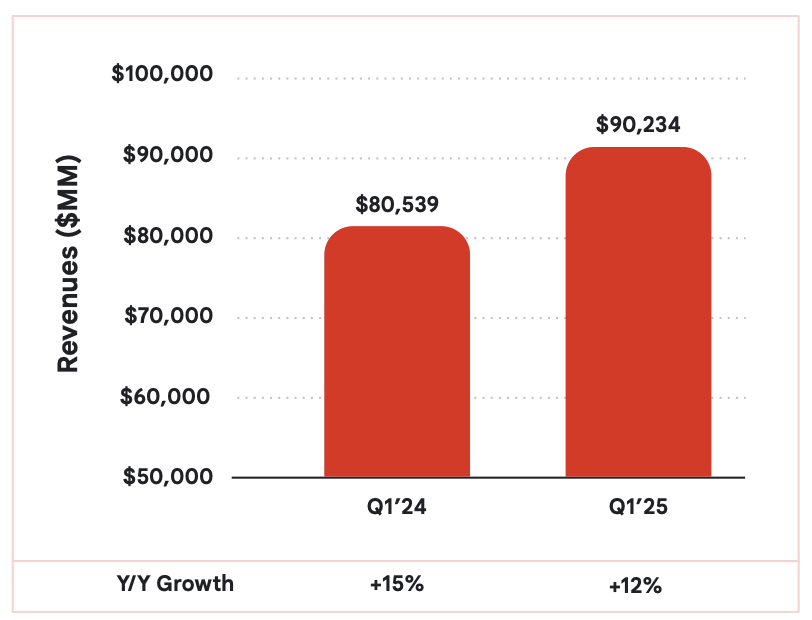

TradingKey - Alphabet’s Q1 2025 results make it official, that transition into an AI-first infrastructure platform is not theoretical anymore, it’s commercial. Irrespective of a crowded generative AI race and growing scrutiny of its market dominance, Alphabet’s stack of complete AI, monetized at scale on consumer and enterprise fronts, is hardening into a lasting second growth driver. Though the consensus takes Alphabet’s $90.2 billion quarter (+12% YoY) as robust but uninspiring, that observation shortchanges the degree to which Gemini is reworking business lines from Cloud to YouTube to Search’s very foundations and redefining monetization levers under the topline.

Source: Alphabet

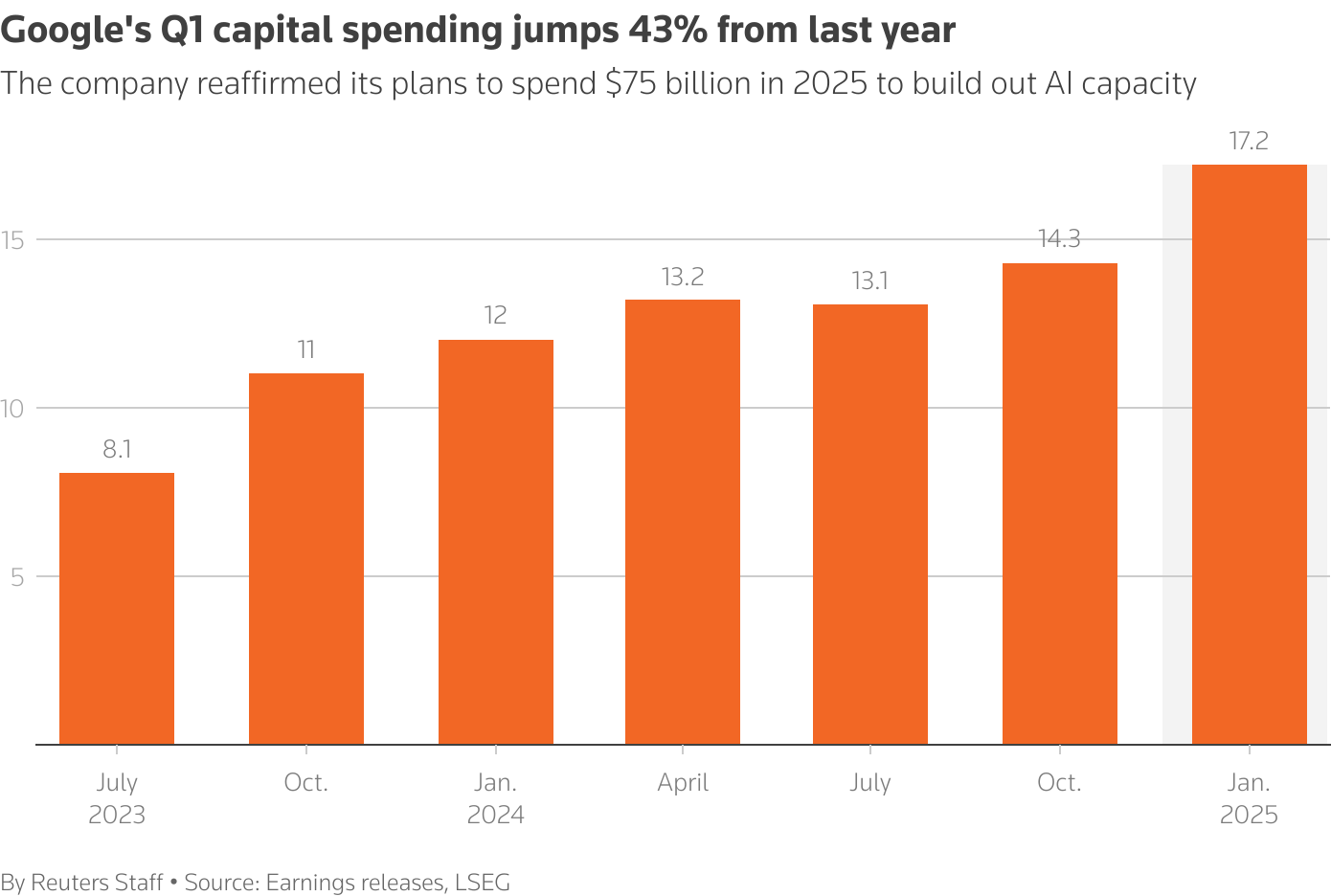

What is asymmetric about this moment, however, is not only the revenue path, but also the compression of monetization reward from AI infrastructure spending. Alphabet reported a whopping $34.5 billion in net income (+46% YoY), but CapEx spiked 43% to $17.2 billion over the same timeframe, with the management guiding to $75 billion in 2025. The key takeout is where it’s being spent: inference-first chips, AI agent platforms, and sovereign cloud footprints. This infrastructure drives Gemini’s 15-product deployment to more than 2 billion users and takes Alphabet’s moat from advertising into enterprise-grade compute, developer ecosystems, and AI-native consumer experiences.

In brief, the Street is holding Alphabet like a margin-resistant ad bellwether, but the company is transforming into something more vast: a hardware-software stack monetizing AI in the attention, enterprise, and creative economies. This article breaks down that transition along four essential dimensions of business model development, differentiation, structural financial resilience, and forward valuation, leading to a risk-adjusted perspective for institutional investors.

Gemini’s Ecosystem: Where AI isn't a feature, it's the product

Alphabet’s business model increasingly feels like a coherent AI operating system, with Gemini as its connective tissue across consumer, cloud, developer, and device ecosystems. Gemini 2.5 drives AI Overviews in Search, Gemini Nano on Pixel devices, Gemini Pro across Workspace, and API integrations in Google Cloud’s Vertex stack. This isn’t cross-sell, it’s recursive reinforcement. For example, Circle to Search and AI Mode are driving 2x longer queries than conventional inputs, deepening engagement and indirectly increasing ad yield in a macro environment where ad pricing is under pressure.

The 1.5 billion users of AI Overviews each month not only represent a distribution benefit but also a data flywheel. Alphabet monetizes such searches via adjacent ad surfaces and inference efficiency gains from proprietary silicon. Meanwhile, Google Workspace now provides 2 billion AI assists per month, deploying Gemini agents into Gmail, Docs, and Sheets, and all of that increases ARPU while shortening user churn. Simultaneously, YouTube Shorts saw 20% YoY growth in engaged views, with AI-driven assets now used in Demand Gen and PMax campaigns throughout.

Cloud also has a key role to play in such a union. Google Cloud revenue jumped 28% YoY to $12.3 billion, and operating income more than doubled to $2.2 billion as margin rose to 17.8%. More than 200 foundation models are offered by Vertex AI alone, and Gemini 2.5 Pro tops the rankings for reasoning, code generation, and scientific inquiry. Google’s differentiated value comes in the ability to deliver open models such as Llama and its own such as Gemini with sovereign, high-performance compute. This enables Alphabet to emerge as a platform of platforms, both one that orchestrates others’ models and captures rents in the plumbing.

Competitive landscape: From Ad Empire to AI Infrastructure Arbitrator

Alphabet is increasingly situated not merely in opposition to ad-based competitors such as Meta but to cloud hyperscalers, AI model labs, and hardware incumbents. Its structural difference in defensibility comes from the capability to merge all such areas through vertically integrated infrastructure.

Nvidia, to cite an example, ships chips to all the hyperscalers but Google's TPUs are specially optimized for its AI applications and now widely used by third-party developers. Ironwood TPUs, the newest from Google, deliver 10x the performance with 2x the energy efficiency over the previous generation, optimized for inference, not training, which equates to the larger TAM when the models transition from development to production.

In Cloud, Google’s AgentKit, Gemini Flash, and sovereign AI solutions make it the most open and secure provider, something especially important as business customers require AI agents to run in-region and maintain data sovereignty. This is a compelling counter-fact to the closed nature of AWS and the deeply coupled nature of Azure with OpenAI’s roadmap.

Even with Meta’s advantage in consumer AI interaction, Alphabet has a trump card in monetization. Although Meta has the benefit of tens of millions of LLM users through Facebook and WhatsApp, it doesn’t have Alphabet’s twin monetization mode, ad yield through query depth and business ARPU through Gemini agents. This provides Alphabet with a structural advantage in compounding of the two factors of attention and usage, on paid and free surfaces. Nevertheless, Google holds over 90% global search market share, giving it a powerful data and monetization base to scale AI features like Overviews and Gemini Search.

Source: Oberlo

Strategic & Financial Deep Dive: Scaling AI with Efficiency

Alphabet’s revenue in Q1 2025 came in at $90.2 billion, a 12% YoY growth, while EPS climbed 49% to $2.81. Under the top line, however, lies a controlled cost structure, with the operating margin widening 230bps to 33.9%. This happened while CapEx went up 43% YoY at $17.2 billion, driven by data centers, servers, and AI infrastructure. Depreciation rose 31% YoY, but margins rose owing to the operating leverage in Search and Cloud.

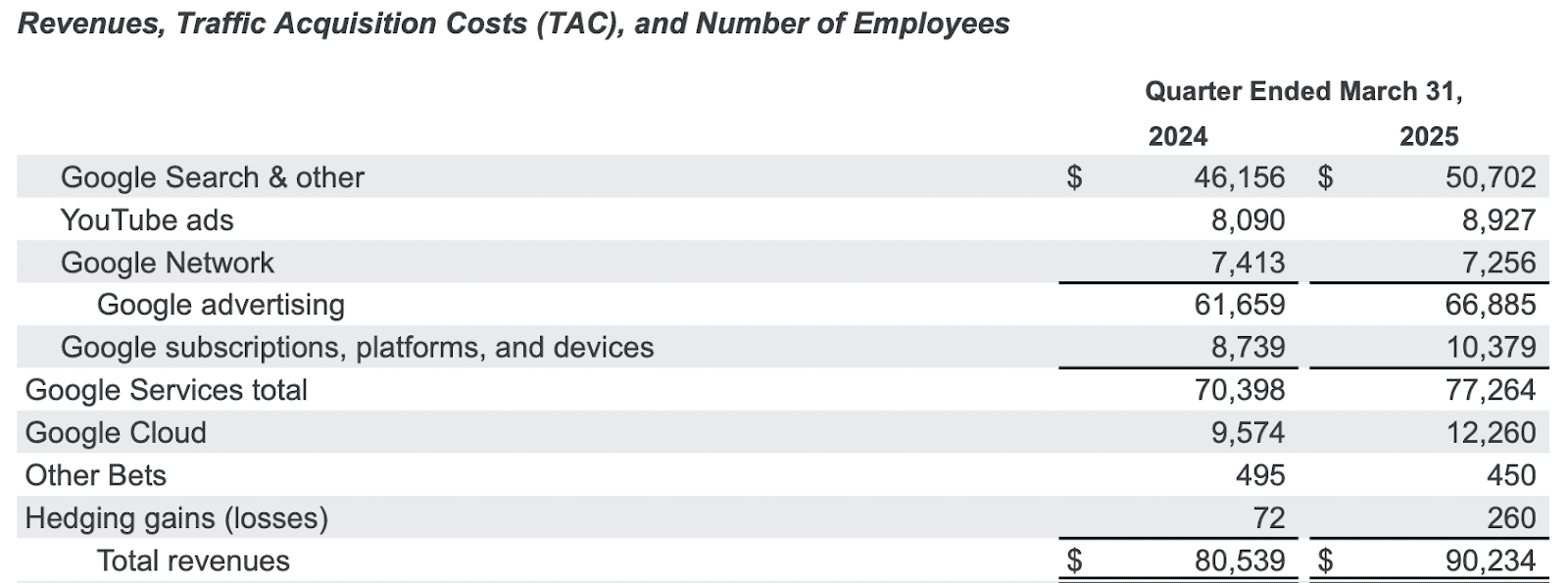

Google Services brought in $77.3 billion in revenue (+10%) and $32.7 billion in operating income (+17%), increasing its segment margin to 42.3% from 39.6%. Google One and YouTube subscriptions, at more than 125 million users, powered the consumer subscription business 19% YoY. Search held monetization flat despite the AI Overviews release, and it's margin-neutral. This indicates that the AI compute costs are being absorbed by Alphabet through efficiencies, not through the rise in ad prices.

Source: Alphabet

Google Cloud's inflection warrants particular recognition. Topline leapt to $12.3 billion, propelled by skyrocketing demand for GCP and AI platforms. Operating income of the segment increased to $2.2 billion, >2x YoY, with better utilization helping to mitigate CapEx drag. Google Workspace's ARPU also improved, indicating capture of AI agent value. Crucially, Cloud now represents 13.6% of the total revenue of Alphabet but merely 8% of opex, indicating that its journey to profitability will not be subsidy-fuelled.

Free cash flow in the quarter was $18.95 billion, while twelve-month trailing FCF was $74.9 billion, all despite historic CapEx. This means that the company, in addition to funding its AI pivot from within, is returning $17.5 billion to shareholders through buybacks and dividends. No other player in the AI space, cloud, search, or consumer platform, is able to match the combination of AI intensity and balance-sheet strength of Alphabet.

Source: Alphabet

Valuation: Hidden Optionality in Plain Sight

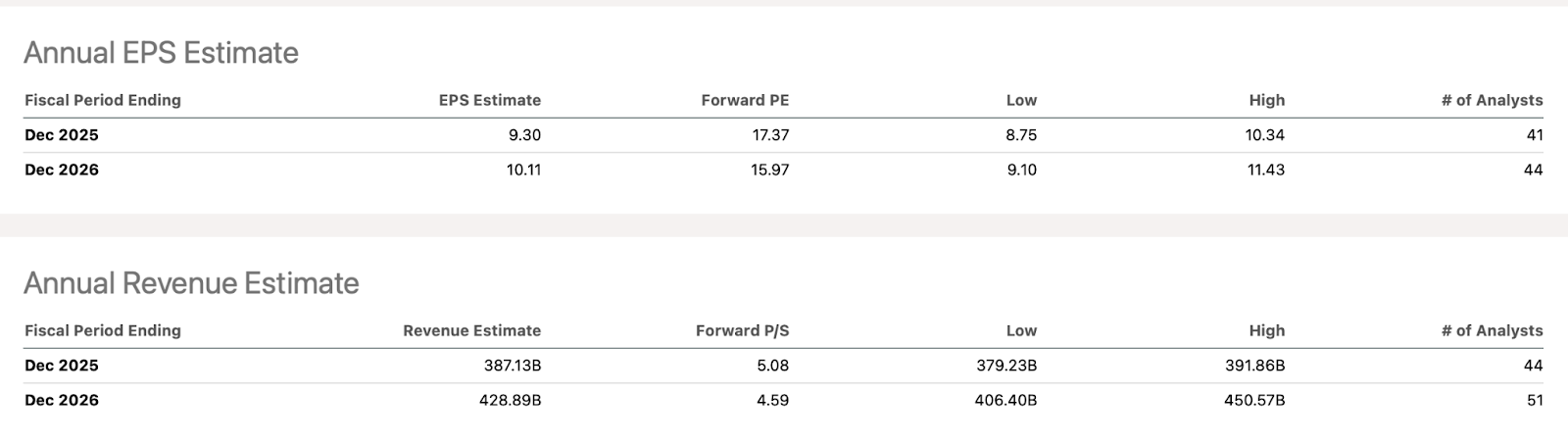

Alphabet's forward valuation indicates investors continue to value it as a mature ad business and not a compounder with plays in consumer AI, cloud infrastructure, and enterprise software. The forward P/E in FY 2025 is 17.37 with the use of an EPS estimate of $9.30 and falls yet lower to 15.97 in FY 2026 with estimated EPS of $10.11. Such levels command a PEG ratio at or below 1, without the use of overly optimistic earnings growth estimates of ~9%.

This double compression comes in the face of upward revenue guidance and structurally better business mix. With revenue projected to increase from $387.1 billion in 2025 to $428.9 billion in 2026, Alphabet is at a forward EV/Sales of only 4.89x, substantially lower than AI peers in the face of 20%+ margins and increasing free cash flow. The FCF yield hovers above 4.5%, and Alphabet's CapEx ramping is self-funded from $75 billion of operating cash flow.

Source: Seeking Alpha

Relative to its peers, Alphabet seems to be overvalued. Microsoft, with comparable exposure to the cloud and to AI, sells at 27–30x forward P/E. Meta, with a more concentrated revenue envelope, sells at about 21x forward P/E. Nvidia sells at about 40x as investors pay for future rents on the infrastructure, while Alphabet is monetizing end-to-end across AI, from Gemini agents to inference silicon to enterprise APIs.

If Alphabet were to re-rate to 22–25 times forward earnings, a modest premium to today but a discount to Microsoft, the estimated fair value would be in the range of $205 to $233 per share. This valuation also doesn't account for optionality in Waymo, Gemini consumer applications, or Gemini Live integrations into the Android ecosystem, each of which could become significant cash generators over time.

Risk Assessment: Infrastructure Heavy, Expectations Heavier

The key risks for Alphabet come from the trio of macro ad sensitivity, regulation, and AI execution. Ads remain about 74% of revenue, and though diversifying, such industries as financial services and retail enjoyed tailwinds in Q1 that could revert in the second half. Regulatory stress, from DOJ antitrust suits to EU DMA enforcement, has the potential to put limitations on including Gemini into Search and Android over time.

Capital intensity is also increasing rapidly. With CapEx guidance of $75 billion in 2025 from ~$55 billion in 2024, margins come under increasing pressure if monetization of AI disappoints. Depreciation should ramp faster, potentially impacting income margins, according to management. And with Gemini having 35 million DAUs compared with about estimated 100 million DAUs of ChatGPT, consumer adoption of AI is still in the early stages despite widespread take-up. Nevertheless, risks remain operational, not existential. Alphabet possesses the platform reach and cash to weather volatility without losing AI momentum.

Source: Reuters

Conclusion

With structural growth in Cloud, Gemini, YouTube, and Search, and a deep moat in sovereign and silicon infrastructure, Alphabet will be able to command not only attention, but also enterprise workflows and consumer behavior. Through market din and regulatory anxiety, the signal is clear: it’s a compounder masquerading as a cash cow.

Recommended Articles