ExxonMobil’s Industrial Renaissance: Profitable Scale in a Decarbonizing World

- ExxonMobil generated $34.4 billion in 2024 free cash flow, fully covering $36 billion in shareholder distributionsfor the year.

- The company projects $30 billion in incremental cash flow and $20 billion in earnings growth by 2030 under flat pricing.

- Product Solutions and Low Carbon Solutions segments are expected to add $3 billion in annual earnings by 2026through new projects.

- Shares trade at ~11x earnings, while sum-of-parts valuation implies $145–165/share fair value, signaling 20–40% upside potential.

TradingKey - Global energy is trending toward climate imperative, digital disruption, and capital stewardship. But in the background of these secular changes, ExxonMobil (XOM) is writing a different narrative. Often interpreted through the prism of fossil-fuel decline, ExxonMobil has subtly remolded itself not merely as a low-cost oil and gas giant but also as a diversified, capital-frugal energy infrastructure giant with structural exposure to decarbonization mega-trends.

The latest fourth-quarter 2024 results only show a company independent of price cycles but steadily unleashing shareholder value through operational scale, conservative capital deployment, and high-margin adjacencies in chemicals, low-carbon molecules, and special materials. Where rivals are racing to adapt business models or pursue green headlines, ExxonMobil's makeover is yielding bottom-line results, overtaking international oil companies in earnings power as well as free cash flow and constructing resilient infrastructure for a multipolar energy world.

By restructuring its business in terms of advantaged production, high-value downstream products, and end-to-end carbon capture capacity, ExxonMobil is doing something few in the industry have: growing sustainably in an environment free of margin destruction. With over $3 billion in incremental project earnings to come by 2026, record levels of structural cost savings, and transitioning to specialty product volumes and decarbonization services, the company is creating a capital-light, platform-like business model. This article analyzes the meat of ExxonMobil's reinvention and how, with its redesigned portfolio, is accruing underappreciated equity value in an imperfect macro backdrop.

Source: Q4 Deck

Reconstruction of the Energy Engine: ExxonMobil's New Model

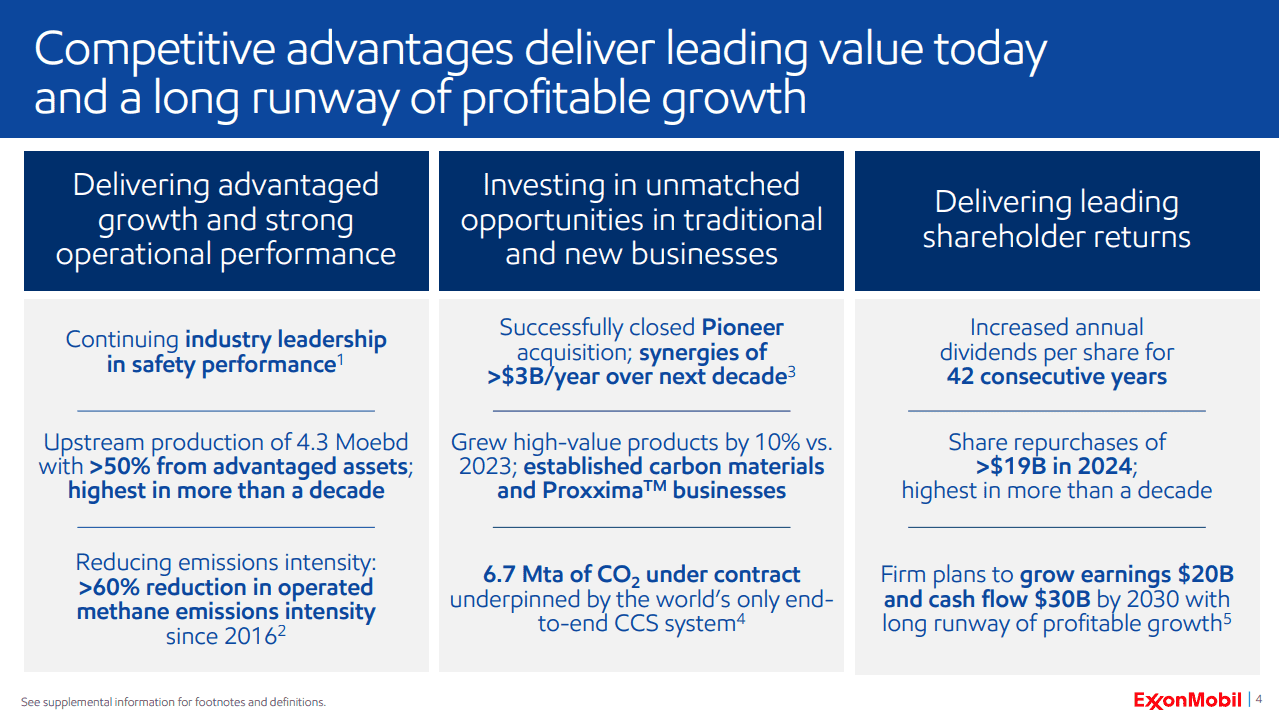

ExxonMobil's existing business framework is the outcome of an eight-year strategy overhaul that maximized scale, rationalized operations, and targeted future-proofed growth. The organization operates through three core segments: Upstream, Product Solutions (including refining and chemicals), and Low Carbon Solutions. Supporting these is a focus on capital discipline and choosing advantaged projects, which have to date yielded increasing structural returns even in backdrop commodity price softness. In 2024, the organization produced 4.3 million oil-equivalent barrels per day, the largest in over ten years, with over 50 percent from advantaged assets such as Guyana, Permian Basin, and LNG megaprojects.

The Upstream portfolio is an example of ExxonMobil's capital strength. Guyana, for instance, is now an offshore development benchmark with growth from first discovery to 650,000 barrels per day in ten years. In Permian, Exxon hit record production of 1.2 million barrels per day with expectation to hit 2.3 million by 2030. The volumes are not only low costs but also more integrated with the downstream and emissions capture infrastructure of the company, expanding even more margin capture along the value chain. It is worth mentioning that over $3 billion annual synergies are expected from Pioneer Natural Resources integration, maintaining its long-term cost advantage in production.

Aside from hydrocarbons, Exxon's Product Solutions business is also proving to be a high-margin, innovation-driven growth catalyst. Historic volumes of specialty products and high-value chemicals in 2024 are indicative that Exxon's investments in performance polymers, such as Proxxima thermoset resins and carbon material advances, are taking commercial root. New Singaporean and Chinese facilities that are coming online will also continue to contribute to margin gains through optimized positions in feeds, in addition to regional demand balance.

ExxonMobil's Low Carbon Solutions business is arguably most strategically differentiated. Unlike other peers toying with renewables, Exxon has concentrated on value capture through infrastructure-led decarbonization. Its in-chain CCS network is the largest in the world, with contracted capacity of 6.7m tons annually in ammonia, steel, and gas processing markets. The network is being built out as a decarbonization service layer for energy-intensive customers such as data centers and industrials emitters. With other hydrogen and lithium projects in development, Exxon is constructing a portfolio of cash-paying, policy-backed businesses with infrastructure economics intact rather than subsidized margins.

Source: eia.gov

Measuring Up: Competitive Moats in an Ever-Changing Energy Landscape

In an industry where legacy capital-intensive promises blur with energy transition promises, ExxonMobil is distinct from comparable groups such as Chevron, Shell, BP, and TotalEnergies. All these companies have transition strategies to their credit, but those pursued by Exxon have generated stronger fiscal results with less fluctuation. Through five years, ExxonMobil's compound annual earnings growth rate was 30 percent, with cash flow CAGR estimated at 15 percent compared to mid-single digits by most European majors. Adjusted return on capital employed in 2024 hit 13 percent, increasing to 17 percent with cash and construction assets excluded, the highest adjusted ROCE by international oil companies.

In contrast to Shell and BP, which chased aggressive divestments and exposure to utility-like renewables, Exxon emphasized portfolio high-grading. Divestments in Argentina and underperforming European refineries, including Fos-sur-Mer, reduced non-core assets without sacrificing operational size. Chevron maintained upstream size, but is without chemical and specialty product leverage Exxon is now leveraging through Proxxima and circular polymers. TotalEnergies, with good exposure to LNG, has suffered execution lags in decarbonization. Exxon's targeted build-out of CCS and hydrogen facilities, with anchor bases and partners, represents an accelerated route to scaled decarbonization returns.

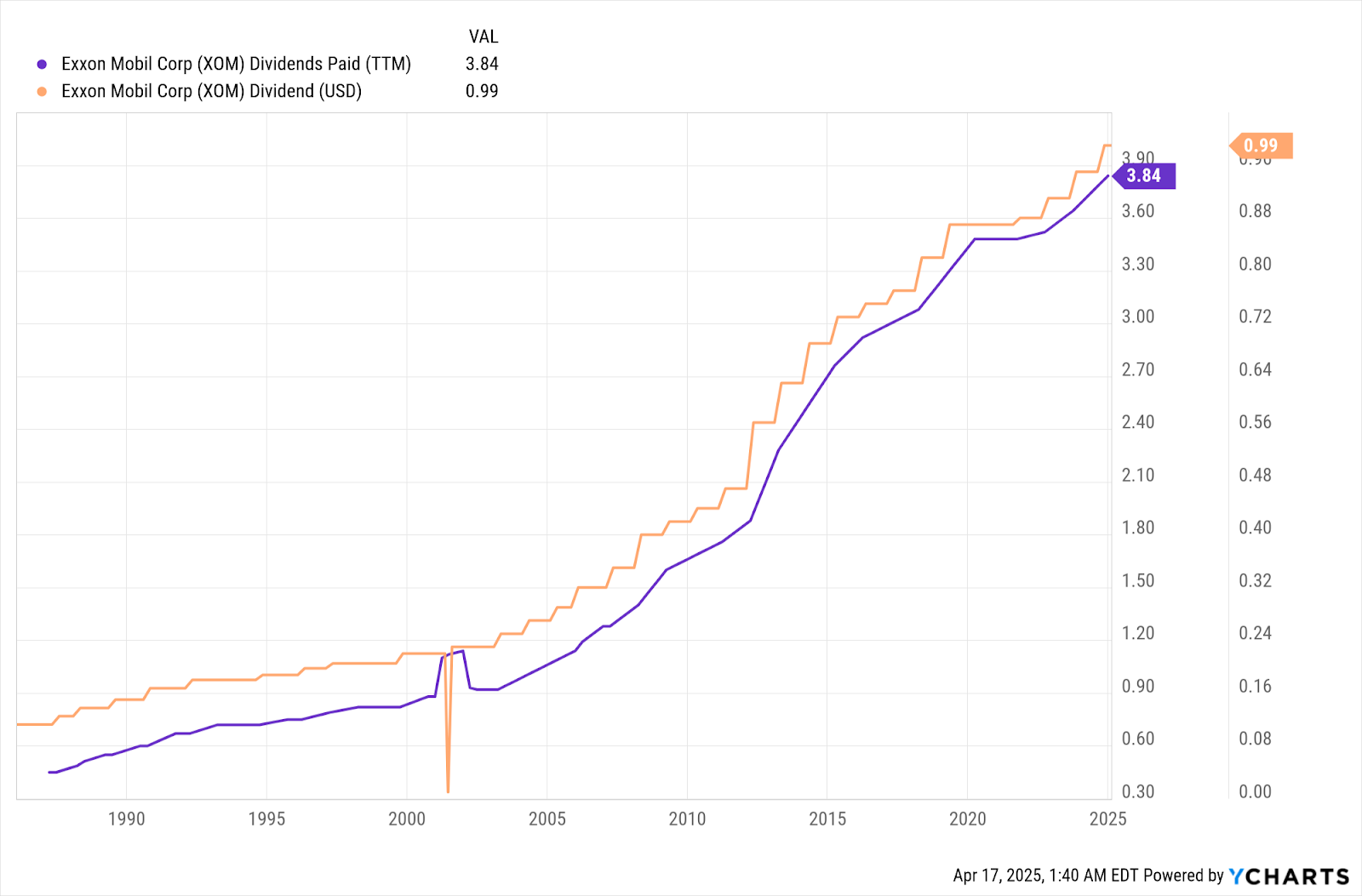

ExxonMobil's capacity to fund expansion through internal means while supporting an increasing dividend as well as an active repurchase program is unrivalled. Its dividend payments of $76 billion coupled with share repurchases of $52 billion over five years demonstrate a nimble capital return strategy that accommodates market conditions. European competitors have less demonstrated payout ratio consistency, frequently linked to cyclical earnings or policy constraints. The advantage that Exxon possesses is not in speculative expansion, but in reproducible, margin-enhancing infrastructure that is complementary to existing operations.

Source: Ycharts

Where Structural Efficiency and Strategic Leverage Meet ExxonMobil's next chapter is based on project execution and platform monetization. Ten of its most important project start-ups have been put in place in 2025, such as the Yellowtail offshore development, China Chemical Complex, Singapore Resid Upgrade, and two Baytown advanced recycling facilities. Altogether, these are set to add more than $3 billion annually to earnings from 2026, and under existing commodity prices and margins. Most importantly, these projects are loaded with higher-value products, demonstrating Exxon’s shift in volume mix to performance materials over refined fuels.

Free cash flow generation is healthy. In 2024, ExxonMobil produced $34.4 billion of free cash flow and $36.2 billion of free cash flow excluding working capital, more than sufficient to pay for its $36 billion of total shareholder distributions. With 2025 cash capex guidance of $27 to $29 billion, the company is still on track to deliver its goal of $30 billion of incremental cash flow and $20 billion of incremental earnings by 2030, based on flat pricing. Notably, only 10 percent of Exxon's capex is designated for policy-specific markets such as hydrogen or CCS, keeping exposure minimal in case incentives change.

Cost discipline has also been a hallmark. Cost savings of $12.1 billion versus 2019 have already accumulated with another $6 billion to come by 2030. Many of these come from centralized procurement, optimized project designs, and deployment of technology in the Permian and Guyana. Depreciation and amortization in 2025 will swell with Pioneer consolidation and project startup, but this more than compensates for contribution to earnings from incremental volumes. Finally, Exxon's Proxxima expansion, from 25,000 tons in 2025 to 200,000 tons by 2030, is adding a high-margin, non-cyclic growth direction with uses in packaging, construction, and mobility.

In the future, management is anticipating normalized working norms in 2026, with lowered start-up expenses and turn-around spending moderation. This would help in margin renewal and improved cost absorption in particular in those segments where margins are still under 10-year levels. Worth mentioning is that even under bottom-of-the-cycle chemical circumstances, Exxon registered positive earnings in this segment based on portfolio optimization and North American-feed advantages for crude, a good indication of hidden strength.

Source: Q4 Deck

Repositioning Valuation: Market Discount versus Intrinsic Value

Its existing equity valuation does not adequately reflect its enhanced earnings model. At around $115 a share, the stock supports a trailing price earnings ratio of about 11 and an EV/EBITDA of less than 7. Both are lower levels than comparable industrials with comparable returns on capital, such as Union Pacific or Caterpillar, which are priced more in the range of 15–18 times earnings. The market seems to place a structural discount on Exxon due to fossil exposure, even with more investment in high-margin, non-cyclical businesses.

On a sum-of-the-parts valuation, Exxon's upstream business, producing more than 4.3 million barrels per day with ~$10 per barrel in unit profitability, would conservatively account for $400–450 billion in enterprise value. The Product Solutions business, with growing contribution from specialty products and projected $6 billion in 2030 earning, would be worth $60–70 billion in standalone value. A discounted $30–40 billion assigned to Low Carbon Solutions and CCS optionality yields an implied fair equity valuation in the range of $145–165 per share. This does not include upside revision from outperformance on projects, which has long represented Exxon's floor.

Source: Q4 Deck

Navigating the Headwinds: Risks to Watch

Although fundamentals in ExxonMobil remain solid, there are a few risks to watch. Uncertainty regarding CCS permits and hydrogen tax credits might slow investment payback in Low Carbon Solutions. The Baytown hydrogen venture, for instance, is reliant upon Section 45V incentives to become economically feasible. Volatility in commodities also poses downside risk, specifically in chemicals, where excess capacity in Asia again dampers margins. The commercialization and execution risks in ramping up newer initiatives such as Proxxima and lithium extraction also present downside to expected returns if demand catch-up slows or technical obstacles occur.

Another possible headwind is political pressure. Legal challenges to Exxon's plastic recycling and wider ESG pushback by activists will likely bring about reputation or regulatory barriers, particularly in Europe and U.S. coastal markets. Nevertheless, Exxon's legal stance and communication strategy demonstrate an intent to fight such pressures, framing itself as a capital allocator rather than political player. Such an action, controversial as it is, might protect it from goal-salient policy changes that hit more compliance-oriented peers.

ExxonMobil's evolution from old-fashioned supermajor to high-performance, diversified energy infrastructure player is firmly established. With earnings quality enhanced, costs streamlined, and returns on capital ramped up, the group is demonstrating how size and innovation are not an oxymoron. For those institutional investors looking for durable yield, capital discipline, and optionality in structurally growing earnings, ExxonMobil presents an intriguing long-hold opportunity at significantly below intrinsic value.

Conclusion

ExxonMobil’s transformation is no longer theoretical, it’s translating scale into resilience, complexity into cash flow, and fossil legacy into diversified infrastructure. With record free cash flow, expanding high-margin adjacencies, and structural exposure to decarbonization, Exxon offers institutional investors a rare blend of yield, durability, and upside, still mispriced against its redefined fundamentals.

Recommended Articles