Q1 2025 Market Forecast: What Bank Results Indicate About the Direction of the Stock Market

Q1 bank profits point to soft landing, not systemic strain ahead.

Rebalancing the Narrative: Why Markets Might Underestimate the Resilience of the Economy

TradingKey - As the first quarter of 2025 is wrapping up, investors are piecing together a more detailed view of the next direction of the stock market. The most recent earnings season, and the season is started, as always, by America's big banks, gave more than a mere health check of the financial system. It revealed important signals about the health of consumer balance sheets, the loan appetites of companies, capital markets action, and even some early warning signs of credit strains. In short, the pulse of the overall economy is steady, if with a few pressure points to watch.

Following a tumultuous 2024 with its stickiness of inflation, oil price shocks, and tighter money, most expected the early stages of 2025 to find banks disappointing all around. But the Q1 reports bucked predictions on a number of dimensions. JPMorgan Chase, Citigroup, Bank of America, Wells Fargo, Goldman Sachs, and Morgan Stanley each contributed a different piece to the puzzle, but the overall portrait is clear: this is not a market struggling in crisis, but one readjusting to a slower, more sustainable pace.

While there are headwinds, from rising delinquencies to weakening loan demand, there is also a quiet but powerful resilience embedded in the numbers. Credit losses remain well below historical norms. Deposit flows, while more competitive, have stabilized. Trading and investment banking are slowly waking up after a dormant stretch, and net interest margins, though off their 2023 highs, are normalizing in a predictable fashion. The key takeaway? The soft landing is still in play, and so is the possibility of a market re-rating in the second half of 2025.

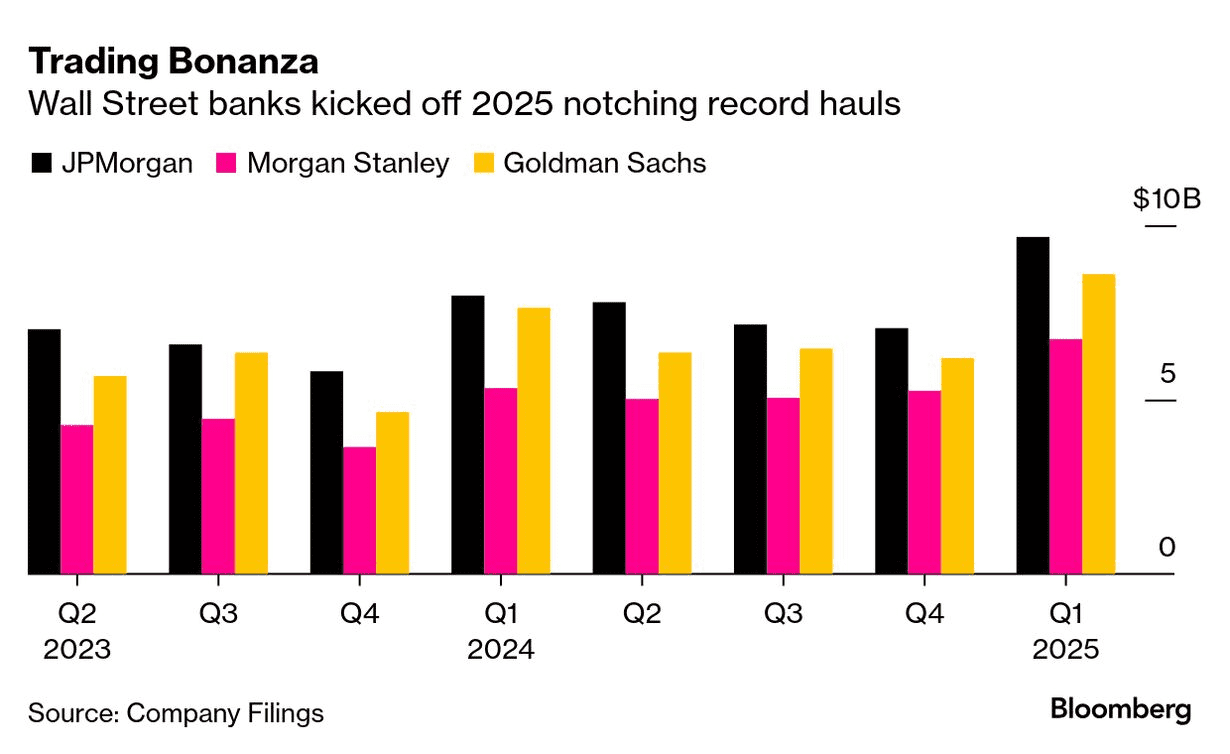

Source: Bloomberg

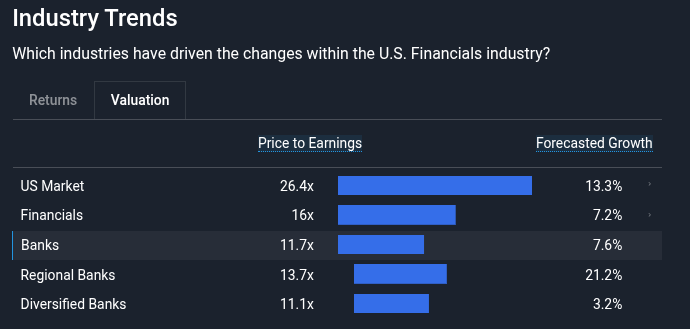

Banks as a trend barometer: Lending trends send a split but workable signal

Fundamental to any economic forecast is the availability of credit. That's why the Q1 2025 bank profits need to be carefully examined. Commercial and industrial (C&I) lending declined moderately year-on-year, led by regional banks, as firms continued to exercise caution and capital spending plans remained prudent. That said, the large-cap banks with international franchises showed a more positive tone, indicating that although domestic lending slowed, foreign demand for credit remained robust.

JPMorgan's loan book rose 2% from Q4 2024, boosted by more robust activity in corporate lending and card balances. Wells Fargo had comparable trends, with sequential increases in auto and home equity loans. Most banks, however, signaled tighter credit conditions, not because of erosion in creditworthiness, but as a result of pricing discipline and regulatory capital constraints.

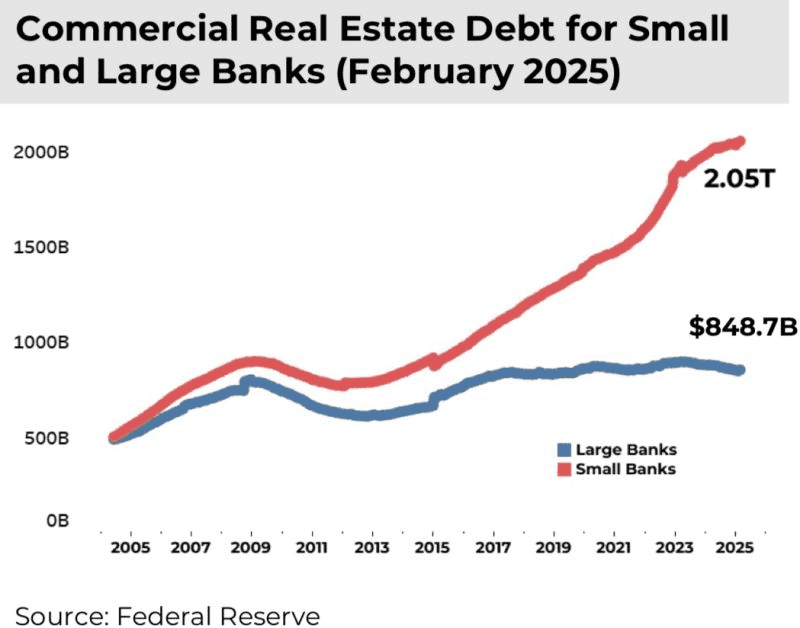

The one spot that concern is burgeoning in is commercial real estate (CRE). Major city offices still are struggling to maintain low vacancy rates, and a few banks already are initiating provisions for impairments in their old-loan books. That said, the absolute magnitude of the problem is still contained, with CRE exposure still comprising a very minor share of the loan book of diversified banks. Systemic cracks in the financial system that systemic investors hoped to find during the quarter were not to be found.

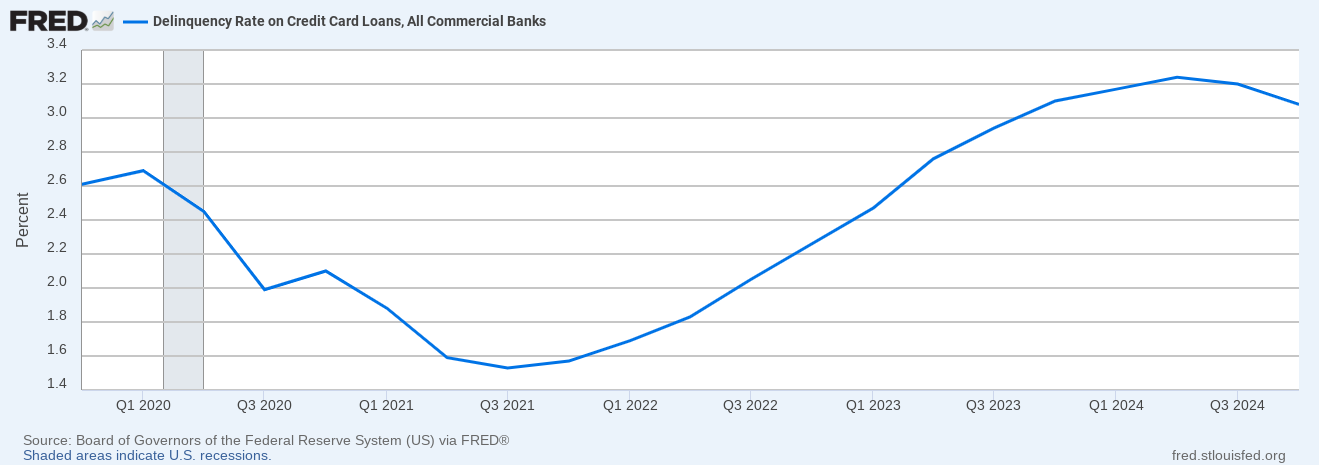

Perhaps most encouraging, consumer credit trends continued to be in decent health. Credit card and personal loan delinquencies did rise, particularly among low-income borrowers, but the numbers were consistent with pre-pandemic levels. There is no sign, so far, of a credit spiral. Families, supported by a still-robust jobs market and increasing wage growth, are still paying down debt, but with narrower budgets.

Source: Federal Reserve Bank of St. Louis

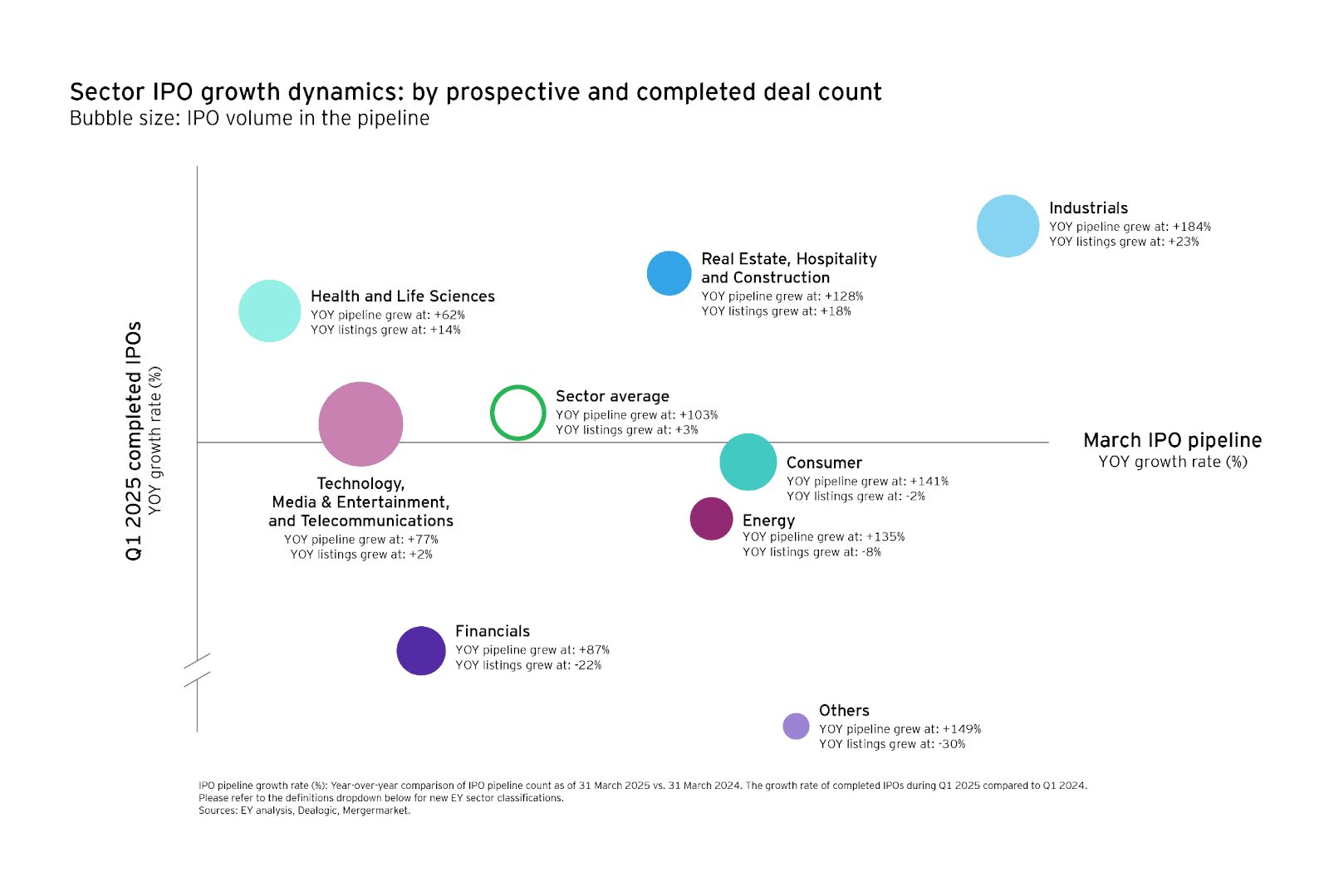

Capital markets awakening: Green shoots for risk appetite

Some of the more positive developments of Q1 came from the capital markets arms of big banks. Following a multi-quarter hiatus, initial public offering activity picked up, while bond underwriting volume bounced back sharply in anticipation of interest rate declines during the second half of the year. Goldman Sachs and Morgan Stanley, in turn, saw notable increases in equity and debt issuance revenue, indicating a thaw in corporate risk-taking.

While M&A remained muted, deal pipelines grew more visible, and commentary from management teams suggested growing confidence among CFOs and private equity sponsors. The cost of capital remains high relative to the 2020-2021 cycle, but with clarity emerging around the Fed’s terminal rate, strategic transactions may accelerate into the summer.

Trading revenue was another source of surprising strength. Fixed-income desks profited from increased volatility in global rates markets, and equities trading got a lift from retail participation and increasing volumes in derivatives. These gains won’t be replicable each quarter, but they remind that banks' fee-generating businesses are more cyclical than damaged, and that markets are beginning to price in the next stage of economic growth.

All of this renewed action in the capital markets also is positive for overall equity sentiment. More robust IPO and deal activity in the past has correlated with a risk-on mood, with the ability for participants to put capital into small- and mid-cap stocks, as opposed to taking shelter in defensive large-caps. If that trend continues, Q2 may be the start of sector rotation into under-loved niches in the market.

Source: EY

Margins in Motion: Surfing the Interest Rate Crosscurrents

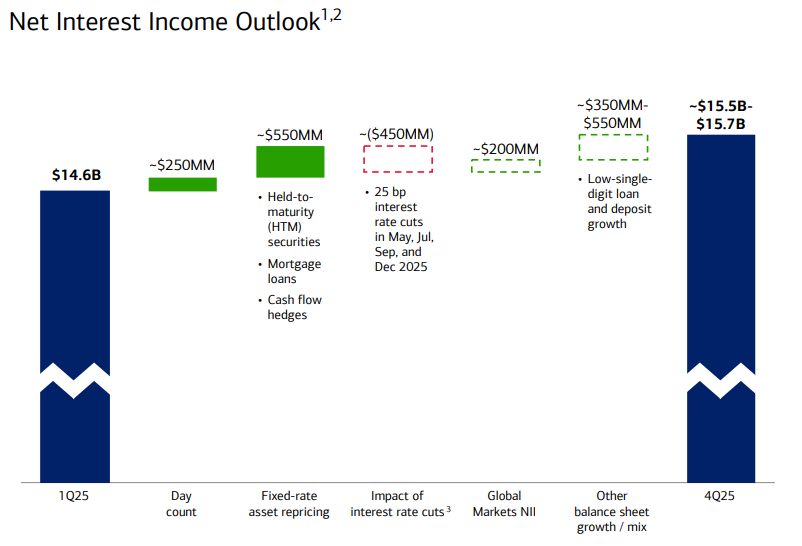

Fed policy dominated the 2024 story, and to a big degree, 2025's narrative will be defined by its wake. Net interest income (NII) of the major profit driver for banks captured that change in Q1. The days of explosive margin growth are gone, but the margins are in no freefall, they're merely normalizing to more reasonable levels.

Take the case of Bank of America. The bank's 4% sequential decrease in NII, driven by slower loan growth and higher funding costs, was reported by the company. Management guided to stability in the second half of 2025, subject to the Fed initiating the cycle of easings. Most of the big banks concurred with that view, indicating that although the tailwind related to higher rates is dissipating, the floor under the margins is quite sturdy because of prudent asset-liability management. In such an environment, deposit betas, how rapidly the banks must lift rates on customer deposits, are still a point of prominence. The fight for sticky retail deposits is intense, largely for the regional and digital-first banks. However, the established banks with large retail networks and high brand loyalty, including U.S. Bank and JPMorgan, are in a better position to maintain their profit margins.

The steepening that took hold in March 2025 has brought some respite as well. As long-dated Treasuries rose relative to their short-term peers, banks now enjoy greater pricing flexibility in their loan pricing, particularly for commercial credit and mortgage debt. Though super-normal earnings days may now be over, the structure still favors decent mid-single-digit profit growth for good-quality banks.

Source: Bank of America Q1 Deck

Sentiment and Valuation: Discounting the Upside, Valuing in Stability

All the positive indications notwithstanding, bank stocks are still cheaply valued. The industry still hovers beneath historical price-to-book levels, even as return-on-equity measures approach the upper boundary of their post-GFC range. The discount in the valuation is a result of lingering fears from the 2023 regional banking crisis, as well as doubts about sustained profitability in a slowing economy.

However, the gap may be temporary. Q1 profits established that banks have successfully stabilized their deposit pools, complied with regulation, and diversified their revenue streams. Further, with the Federal Reserve ready to ease policy in the third quarter of 2025, market views are looking for two rate decreases that commence in July, banks may experience a boost in credit volumes and trading.

Equity investors have also been rotating back into cyclicals, including financials, as soft-landing expectations firm up. If macro data continues to support a “not-too-hot, not-too-cold” thesis, the broader S&P 500 could see a re-rating, led in part by a rebound in sectors that lagged in 2024, such as financials, industrials, and small caps.

The benefit isn't purely theoretical. Dividend yields in the big banks are still attractive, frequently greater than 3%, with high potential for repurchases. Capital levels are strong, with CET1 levels comfortably in excess of regulatory requirements, providing boards with the ability to return capital even in a reserved economic climate. The risk-reward for long-term shareholders is tilting in their direction.

Source: simplywall

The Risks Remain: From CRE to Regulation and Geopolitics

That notwithstanding, investors should be careful not to get too euphoric. The perils are very real, and unevenly distributed. Commercial property still stands as the most obvious fault line in the system, most notably among regional banks with high concentrations. While the big banks are insulated, prolonged pressure in the valuation of offices can result in mark-to-market losses and added provisioning sector-wide.

Regulatory overhangs also are a concern. The Basel III Endgame, to be concluded later in the year, would radically change capital demands, most notably in trading books and operational risk. Large banks are already better-capitalized, but investor optimism may be tempered by uncertainty over the implementation timelines and ultimate thresholds.

Geopolitical threats also figure prominently. Escalation in the Middle East and the 2025 U.S. election uncertainty may add to the volatility of both equities and credit markets. Banks, being leveraged participants in the economy, are by their very nature vulnerable to such macro shocks.

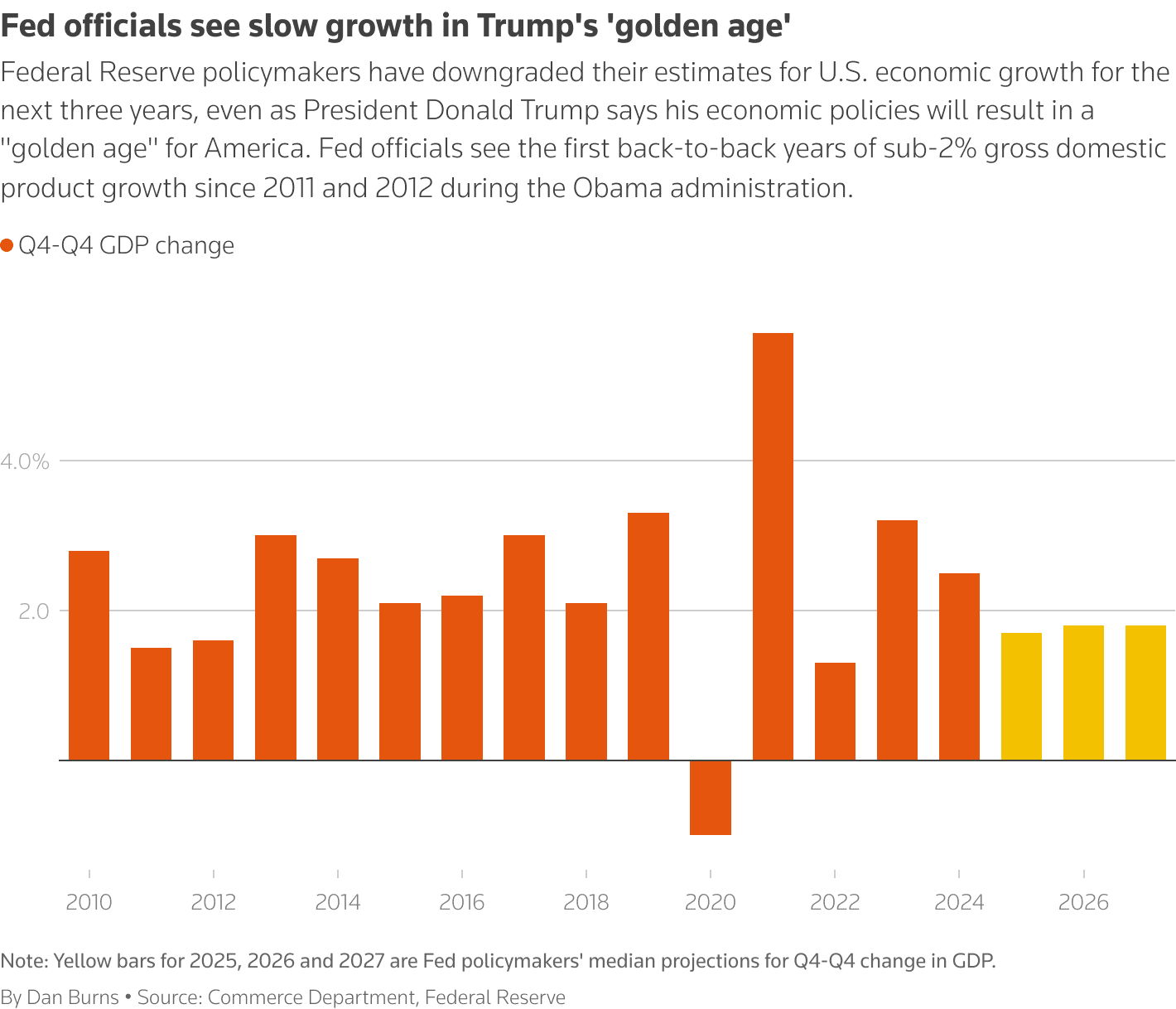

Lastly, the possibility of a policy error still lurks. Should inflation be stickier than thought, or the Fed wait to cut rates into 2026, credit demand may decline further, and asset prices may falter. On the other hand, excessively aggressive loosening can revive the specter of inflation, steepening the curve but augmenting long-term uncertainty.

Source: Lawrence Yun, Chief Economist at National Association of REALTORS

Looking to the Future: Restoring Confidence, Quarter by Quarter

The early part of 2025 provided a subdued but compelling refutation of the pessimism of late 2024. Rather than evidencing symptoms of systemic pressure, the banking system demonstrated an economy that is readjusting occasionally lumberingly, but not ruinously, to a more normal interest rate environment. Consumers continue to spend, firms are slowly rousing, and capital markets are once more showing the stirrings of life.

For equity markets, this translates to a base case of cautious optimism. If the Fed begins its rate-cutting cycle by midyear and inflation continues to ease, investor confidence could steadily rebuild. The ingredients for a second-half rally are falling into place, not through speculative fervor, but through durable, data-backed progress. Banks may not drive the market up in a sensational way, but they're setting the stage. Their profits are a glimpse into what's most important at the moment: stability, flexibility, and the gradual resumption of growth. And that's a narrative the market is only just starting to price in.

Source: Reuters

Recommended Articles