3M: From Industrial Icon to Operational Reinvention

- CEO Brown targets $1B in cost-outs and 1,000 new product launches by 2027, signaling a rigorous shift toward margin-driven operational performance.

- 2024 saw a 32% YoY increase in product launches, with 215 expected in 2025—critical to rebuilding pricing power in commoditized markets.

- 3M’s global OEE remains in the low-50s, suggesting latent productivity gains as AI, digital twins, and predictive systems are rolled out.

- Q4 2024 EPS beat by $0.13; 118% FCF conversion and 23.8% adjusted margins reflect early success of tighter capital and pricing discipline.

TradingKey - A symbol of industrial diversification strength once, 3M (MMM) is at a critical juncture today. Decades of PFAS chemical litigation, reputational scars, and uninspired performance had slowly diminished investor trust. With a new leader in charge, however, and a detailed transformation plan already in motion, 3M’s revival could be one of the most interesting turnarounds in industrials, if execution proves up to the task.

Underpinning this thesis is a fundamental change in 3M's DNA. CEO William Brown has introduced the “new 3M": a performance-driven, operationally intense business dedicated to rigorously measured KPIs, margin-driven execution, and innovation-driven growth. This is not lip service from the corporation. Already, the firm is aiming for structural cost-outs of $1 billion, new product launches of 1,000 in three years, and cumulative return of capital of $10 billion by 2027. If these begin to take hold, the market might see a structurally higher-margin, cash-generating variant of 3M, quite a departure from the stagnation of the past few years.

Tailwinds, though, are by no means assured. The big-picture outlook is murky, and visibility into demand is protracted as buyers become risk-averse due to tariffs and weakened manufacturing activity. Despite strong backlog and ordering trends, Q1 organic growth is running at merely 1–1.5%, versus expectations. The firm is walking a tightrope: investing in new skills while trimming costs in a precise manner. Whether these competing objectives clash or catalyze profitability will be the ultimate test of this turnaround.

Source: 2024 Deck

Innovating Under Pressure: The Inside Story of 3M's Reth

Fundamentally, 3M is a three-segmented multi-industrial conglomerate: Safety & Industrial (SIBG), Transportation & Electronics (TEBG), and Consumer. Each contains a constellation of defensible, specialist products, from abrasives, tapes, and filtration systems through consumer adhesives to automotive materials. But in the past, it was not breadth but rather R&D capability, allied with a commercialization flywheel, that truly set 3M apart. Its engine, underutilized for decades, was finally revving up.

The firm's 3M eXcellence system today drives a culture of execution, from strict monitoring of KPIs to unyielding continuous improvement. CEO Brown is driving accountability with a performance management layer, and already the cadence of new-product launches is picking up speed: up by 32% year-over-year in 2024, with 215 product launches planned in 2025, on track to hit 1,000 in 2027. Here, early momentum is important, as innovation has traditionally been 3M's most enduring moat, driving pricing power in commoditized verticals.

Just as important, though, is the evolution of 3M’s operating model. With worldwide OEE (Overall Equipment Effectiveness) remaining in the low-50s, the firm has substantial latent manufacturing leverage. Underutilization, not only is a source of cost opportunity, but of strategic optionality as well: the potential, in the face of tariff uncertainty, to rebalance production or reallocate volumes nearer the tailends. 3M’s North American base, 45 U.S. factories plus three in Mexico, contributes a degree of flexibility its peers might not possess, if, say, tariffs increase further in 2025.

Furthermore, management is weaving AI and data analytics into its operating system. Though not an AI-first business, deployment of digital twins within manufacturing, predictive maintenance software, and AI-driven pricing optimization brings algorithmic strengths. These are not front-page-type offerings, but they drive productivity at scale, a key advantage in low-margin segments. According to the CFO, AI within 3M is “quietly compounding beneath the surface,” especially in supply chain and commercial analytics.

Source: 2024 Deck

Getting Ahead or Paddling in Place? Relative Positioning by 3M in a Dissevered Marketplace

3M's resurgence can't be measured in a vacuum. Its industrial peers, whether Honeywell and Parker Hannifin or DuPont or Illinois Tool Works, are all advancing leaner cost structures, digitization, and selective divestitures. The issue is: What specifically distinguishes 3M in this new phase?

On price, though, 3M has started to fight back. After a years-long slow-motion pricing discipline, management is actively introducing base price increases as well as selective surcharges, based on the elasticity of each business group. This new game plan, made possible by more accurate data systems, has offset $60 million of expected tariff hit in 2025. While the peer groups are also changing price, none has the same degree of upstream integration or domestic manufacturing duplication, so that 3M can fight share in a way that doesn’t precipitate customer defection.

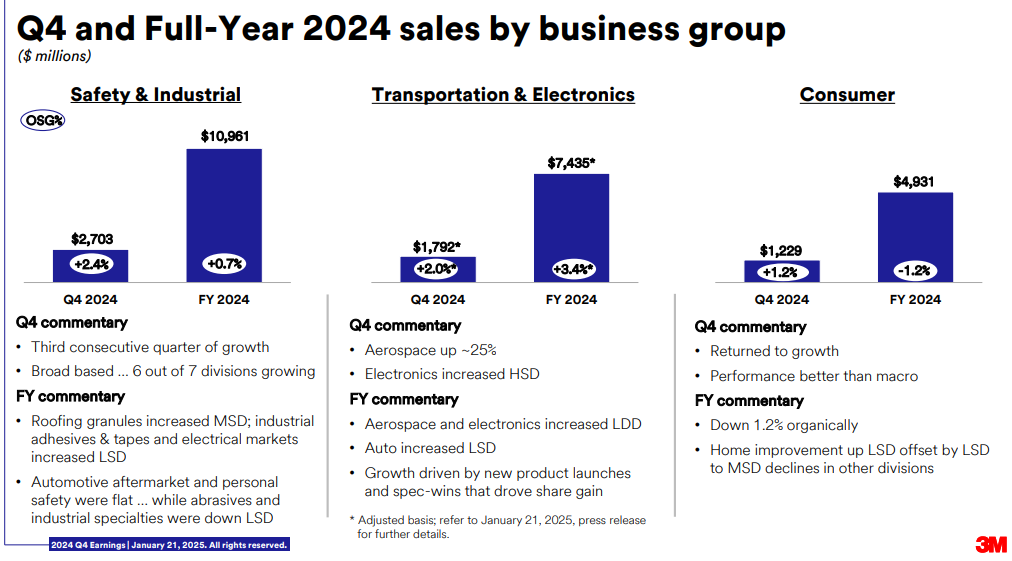

However, customer acquisition is unbalanced. The Consumer segment, anchored by heritage brands such as Scotch, Post-it, is underperforming, especially in retail and office supply channels. On the other hand, SIBG and TEBG are more resilient, supported by mid-single-digit growth in China, stable aerospace recovery, and strong electrical systems demand. Particularly, 3M's adhesives and tapes business, a leader in industrial assembly, is gaining from trends in machinery and electronics onshoring.

Relative to peers such as Honeywell (which has more software monetization strength) or Eaton (with more electrification exposure), the source of 3M's strength is in its breadth of product offerings as well as vertically integrated supply base. Though breadth previously diluted focus, it can perhaps become a source of differentiation, if execution within operating units is made consistent through the use of the 3M eXcellence system. This is subject in full to whether or not decentralization gives further way to systems thinking, and margin-building habits are ingrained.

Source: 2024 Deck

Operational Reinvention or Short-Term Boost? Unpacking the Statistics

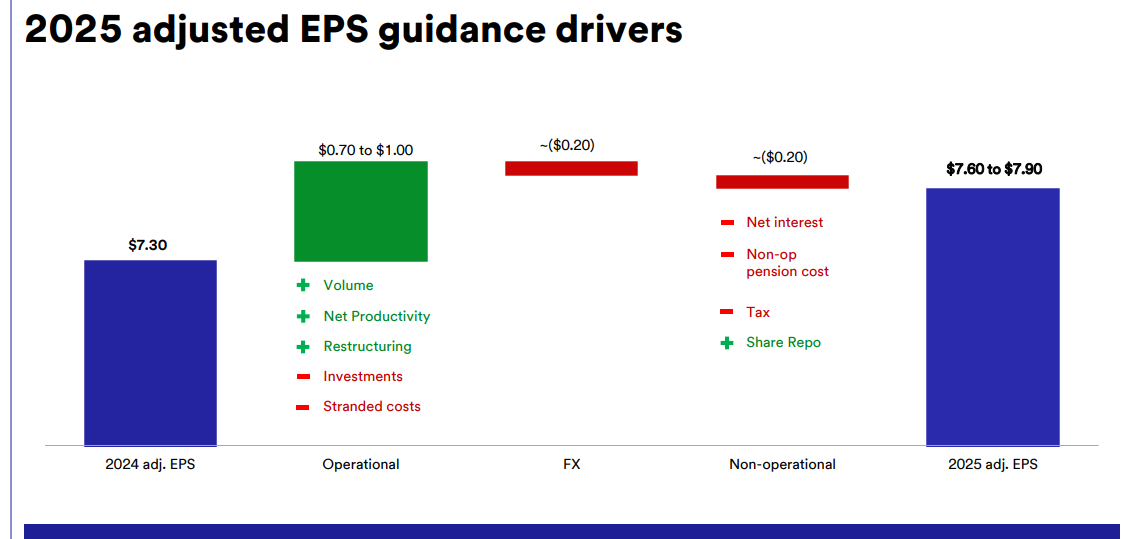

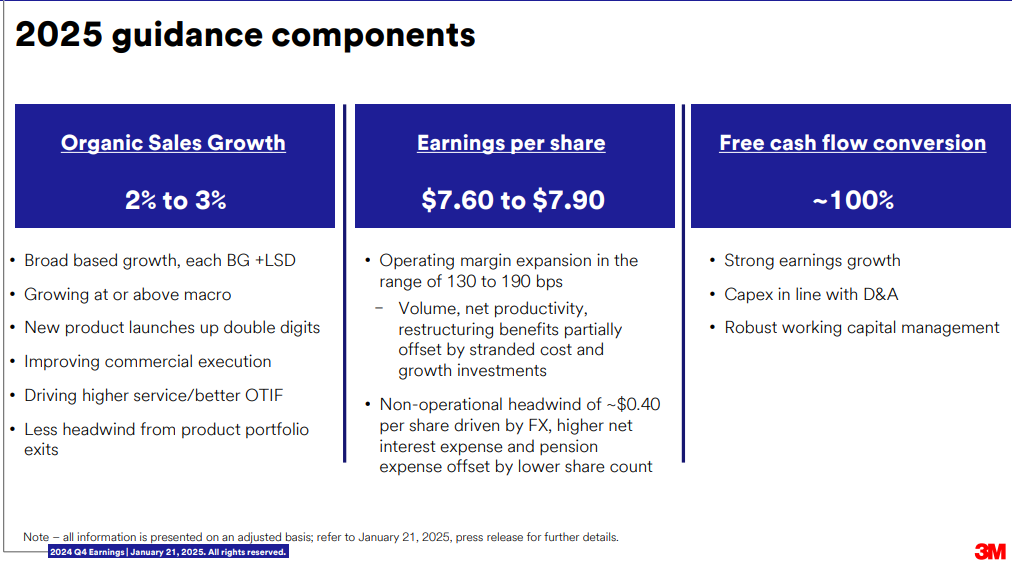

From a financial perspective, 3M's turnaround is in its early stage, but the momentum is gaining. The company reported Q4 2024 adjusted EPS of $2.42, a beat of consensus by $0.13, while adjusted operating margin was up at 23.8%, a 210 basis point increase from the same period last year. Full-year adjusted free cash flow conversion was a strong 118%, with FCF at $5.6 billion, indicating more stringent working capital discipline and CapEx. Notably, 3M maintained guidance for 2025: 2-3% organic growth, along with 4-8% adjusted EPS growth, powered by margin tailwinds and cost discipline.

The growth drivers are divided equally between new product launches and commercial greatness. The latter comprises broadened pricing stewardship, go-to-market renewal, as well as digital tools of sales enablement. Furthermore, management has set aside $250 million in productivity investment through fiscal year 2027, of which $80 million will be invested in 2025, flexible enough to throttle in response to macro conditions. This divide in offensive and defensive allocation of capital is important in as the firm navigates demand stretching.

The customer backlog is in good health, with February's order activity up year-on-year in all segments, but most notably in SIBG. Management warned, however, that delivery schedules are sliding as distributors ask for later shipping, a sign of prudent rather than absolute weakness. Reassuringly, order flow exceeds sales, meaning pent-up demand should see the light of day in H2 2025, subject to stabilization in macro trends.

Capex has stabilized at $1.2 billion a year, from higher levels experienced pre-restructuring. Meanwhile, $10 billion of cash is planned for return by 2027, half in dividends, half in share repurchase. This two-pronged policy of reinvesting and returning cash is a sign of a maturing cash machine, provided litigation threats don’t return in strength.

Valuation Based on Skepticism: Discount Signal or Structural Decline

In spite of perceptible momentum in operational achievement, 3M remains at a big discount in terms of valuation, a reflection of investor doubt regarding its litigation aftermath, commodities consumer demand weakness, and residual skepticism surrounding cultural transformation. Yet, the price-performance mismatch might be creating a skewed opportunity.

Based on the most recent industry-relative metrics, 3M has a 15.90x non-GAAP TTM P/E and 16.27x forward P/E, a tad lower than the industrial sector median (–3.6% and –0.02%, respectively), but at a ~6% premium versus its own 5-year average of 15.04. This implies the market is not pricing in a breakdown, but also not factoring in a sustained operating upturn. The PEG ratio of 2.13 (compared with the sector median of 1.41) is a sign of higher forward earnings expectations, perhaps due to the firm's aspirational margin and R&D road map, but also reveals vulnerability to earnings miss.

On a forward-selling basis, the valuation difference is extreme. 3M rests at a price of 3.10x, more than 90% higher than industrial peers' median. This difference, also evident when looking at EV/EBITDA (10.88x vs. 9.83x), can partially be explained by more robust free cash flow metrics and cost leverage but also signifies danger of mean-reversion if top-line growth falters. EV/EBIT stands at 13.47x, just lower than the median of the peer group at 13.85x, bringing a degree of relative consolation that earnings quality, rather than mere appearances, is driving P/R.

Where 3M appears to be reaching is in terms of price/book and price/cash flow. The stock's forward P/B multiple of 14.32x and forward P/CF multiple of 15.04x are well in excess of industry medians (465% and 17% higher, respectively). This is reflective of 3M's asset-light, intangibles-rich business model, but it also constrains support if ROIC trends are a disappointment or litigation expense flares up once more.

Specifically, the 2.23% dividend yield continues to represent a 30% premium to peers, though down almost 47% from its five-year average, a reflection of how share price gains have tightened the cushion even during steady payouts. With $10 billion allocated for return of capital through 2027, the dividend has been a stabilizing anchor in a complicated story.

Overall, 3M's valuation is a story of two stories. On cash flow and headline P/E metrics, the stock looks fairly valued against execution opportunity. However, higher P/S and P/B multiples suggest a reluctant market in committing wholesale endorsement of the turnaround. That conflict, between past baggage and operational momentum, would be the rerating driver if 3M can deliver margin growth and free cash growth as forecast.

Source: Ycharts

Known Knives and Concealed Mines: Evaluating the Risk Matrix

Litigation risk is the single greatest overhang. In addition, while the Combat Arms Earplugs settlement and PFAS public water supply class action are moving towards resolution, ongoing environmental liabilities and regulatory attention can generate surprise liabilities. These historical risks also obscure investor sentiment even as operational performance continues to improve. Externally, trade tensions also present incremental margin headwinds.

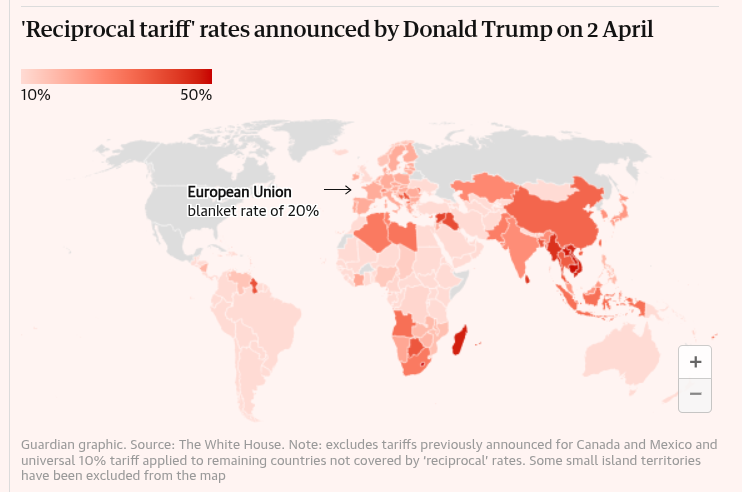

With half of exports at $4 billion, half from North America, and 10% from China, at $1.6 billion, tariffs on Chinese components,steel, or aluminum could clip margin expansion if not completely covered by pricing. Early indicators are encouraging, however, 3M has absorbed gross tariffs of $60-70 million and not missed earnings, but ongoing pressure (Trump Tariffs) might limit pricing power or elasticity in volumes.

Source: theguardian.com

Lastly, management's culture change remains untested. Execution risk is real due to 3M's large geographic reach and entrenched bureaucratic structures. Without performance-based culture taking hold across layers, early gains can erode under previous habits. Patience from investors will depend upon sustained cost leverage, improving productivity, and persistent execution against product launch and margin objectives.

Bottom Line

No longer a mere passive accretive story, 3M is a high-risk transformation saga in which asymmetric upside is realizable if operating and cultural reforms hold. Despite risks, early results bring guarded optimism. Those able to overlook heritage litigation and near-term macro shadows may see the beginnings of a resilient industrial compounder germinating.

Recommended Articles