Block: Value Trap or Investment Opportunity?

Source: TradingView

Key Takeaways:

· Financial Performance: Gross profit grew from $2.733B in 2020 to $8.869B in 2024, with an EBITDA margin of 34%, but stock underperformed peers.

· Square Challenges: GPV growth slowed to 10% due to U.S. market saturation (6.9% growth in Q4 2024) and competition from Clover and Toast; international markets and lending (22% of gross profit) offset declines.

· Cash App Slowdown: Growth stalled with monthly active users at 57M (2% YoY increase) and gross profit growth at 21.20%, pressured by Venmo, Zelle, Apple, Google, and economic challenges for lower-income users.

· Strategic Shift: Block refocused Cash App on user engagement, increasing inflows per user by 10% through Borrow and BNPL services, despite slower user growth.

· Valuation: Using SOTP, Square’s 2026 EBITDA of $1.913B at 11x EV/EBITDA and Cash App’s $7.05B gross profit at 2x EV/Gross Profit yield a $66 target price, reflecting competitive and regulatory risks.

1. Company Overview

TradingKey - Block is a leading global financial technology company founded in 2009 and headquartered in San Francisco, USA (formerly known as Square, renamed Block in 2021). Through cutting-edge technology, Block creates simple and efficient tools for merchants and individuals, revolutionizing the payment and financial management experience, and is committed to enabling everyone to easily integrate into the digital economy. However, over the past year, Block's stock price has significantly underperformed compared to its competitors and the broader market indices.

Core Business

Block's core business focuses on two flagship products:

· Square: A one-stop payment platform designed for merchants, providing mobile payment devices (Square Reader) and software to help small businesses easily accept credit card payments, manage sales, and inventory.

Square generates revenue by helping merchants process payments, primarily through three streams:

1. Payment and Tool Services: This is Square's main revenue source, including POS systems, invoicing tools, and online store features. These tools enable merchants to accept payments easily, with Square taking a small fee from each transaction.

2. Loan Services: Square provides loans to merchants, such as through Square Loans, allowing them to access funds for business operations. Square earns money by charging interest on these loans.

3. Manual Entry Transactions: When merchants manually enter card details into Square to process payments (instead of swiping a card), Square charges a small transaction fee.

· Cash App: A mobile financial application for individuals, supporting instant transfers, stock trading, and Bitcoin investments, simplifying daily financial operations.

Cash App generates revenue by facilitating user transactions, with income primarily coming from three sources:

1. Debit Card and Payment Services (largest contributor to gross profit): This is Cash App's primary revenue stream, including the Cash App Card (a debit card for shopping) and Cash App Pay (a payment feature). When users make payments with these, merchants pay Cash App a small transaction fee.

2. Instant Transfers and Bitcoin Services (declining share but still significant): Cash App charges a small fee, such as a transfer fee or trading fee, when users opt for instant deposits to transfer money to their bank accounts quickly or when they buy and sell Bitcoin.

3. Loan Services (rapidly growing): Cash App offers small loans to users (e.g., through Cash App Borrow) and earns money by charging interest, similar to how banks profit from lending.

Unique Advantages

Block's unique advantage lies in its innovative "ecosystem closed-loop" model. Simply put, the "ecosystem closed-loop" is like a self-sufficient family farm: Block provides payment services to merchants through Square and financial tools to consumers through Cash App. The two are seamlessly connected—merchants receive payments, and consumers make payments, forming a mutually beneficial cycle where funds circulate within the platform, reducing the loss of funds to external sources. At the same time, this seamless service enhances user stickiness, as users are more willing to continue using the platform due to its convenience, creating an efficient win-win situation.

2. Block Financial and Business Overview

Source: TradingKey, Block

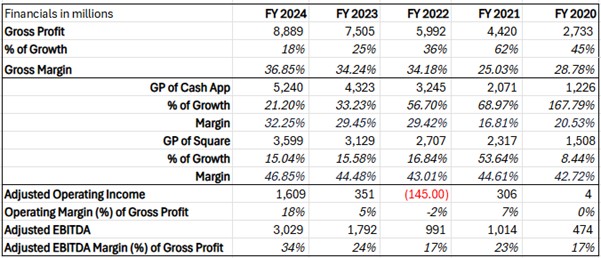

From an overall perspective of Block, over the past few years, gross profit has increased from $2.733 billion to $8.869 billion, with the gross margin rising to 36.85%. Operating income has grown to $1.609 billion, achieving an operating margin of 18%. EBITDA has risen from $474 million to $3.029 billion, with the EBITDA margin improving to 34%. This reflects a significant enhancement in profitability and operational efficiency.

Among its segments, Cash App’s gross profit has surged from $1.226 billion in 2020 to $5.24 billion in 2024, with its gross margin improving from 20.53% to 32.25%. This demonstrates a notable strengthening of its profitability in the consumer financial services sector. However, its gross profit growth rate has declined from 167.79% in 2020 to 21.20% in 2024, indicating that after an initial explosive growth phase, the pace of expansion has gradually slowed. This could suggest that bottlenecks in product innovation have constrained its growth momentum, which is a primary reason for the overall slowdown in Block’s gross profit growth.

Square, on the other hand, has shown steady performance, with gross profit growing from $1.508 billion in 2020 to $3.599 billion in 2024, maintaining a stable gross margin of around 45%. This reflects its consistently high profitability in the merchant services sector. While Square’s growth rate remains steady at around 16%, it is not as rapid as Cash App’s. Nevertheless, its high gross margin and sustained growth provide a solid foundation for the company.

3. Square Business Challenges and Strategic Responses

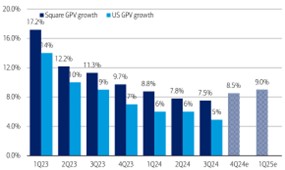

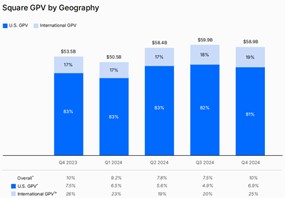

Since Q1 2023, the growth rate of Square's GPV has steadily declined, dropping from 17.2% to 10%, primarily due to intense competition from players like Clover and Toast. Growth exhibits clear geographic divergence: the U.S. market, accounting for over 80% of GPV, saw its growth rate fall from 14% in Q1 2023 to 6.9% in Q4 2024, signaling market saturation and intense competition. Meanwhile, the international market’s GPV share is steadily rising, with growth rates significantly outpacing the U.S., emerging as the primary growth driver. Against the backdrop of a weakening U.S. GPV, the robust performance of international markets has partially offset the overall slowdown. Collectively, the rapid expansion in international markets is becoming the core driver of Square’s GPV growth, potentially enabling a rebound in the Square business segment’s GPV.

Source: BofA Global Research, Block

Specifically, to drive Square's business recovery and growth, Block is addressing challenges through multifaceted strategic adjustments:

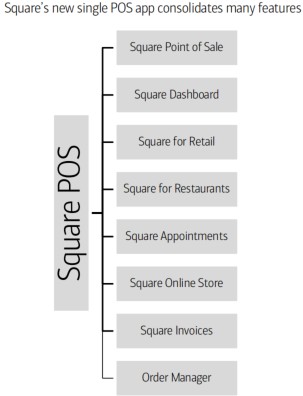

· Product Innovation: Through product innovation, Block has integrated functions such as invoicing, retail sales, restaurant management, and appointments into a single "Square Point of Sale" application, simplifying merchant operations and enhancing flexibility, which is expected to increase merchant adoption rates and boost transaction volume growth.

Source: BofA Global Research, Block

· Improved Market Strategy: In its market strategy, Block is focusing resources on the restaurant, retail, and service sectors (accounting for 60% of GPV in 2024), optimizing customer acquisition through localized sales teams and multi-channel B2B marketing (e.g., brand promotion and trade shows). Additionally, Block has established partnerships with companies like US Foods, Sysco, T-Mobile, and others to promote its hardware and software solutions. For instance, its collaboration with Sysco covers 40% of U.S. restaurants, significantly expanding market reach.

Source: Block

· International Expansion: Block is promoting banking services and payment solutions in Canada, Australia, Japan, the UK, Ireland, France, and Spain. New initiatives include streamlining bank account integration for UK merchants and partnering with Japan’s JCB and Mercari to introduce QR code payments, which are expected to further penetrate international markets and enhance market presence.

· Lending Business: The lending business has become a key growth driver for Square. Square Loans accounted for 22% of Square’s gross profit in Q3 2024, with year-over-year growth exceeding 20%. Globally, Block has underwritten over $22 billion in loans, maintaining a loss rate below 3%. Leveraging POS payment data to gain insights into sellers’ financial health, Block effectively manages credit risk, while simplifying repayment by deducting a portion of sales proceeds directly, enhancing merchant stickiness.

Overall, Square’s stable profitability and high gross margins provide a solid foundation. Amid U.S. market saturation, international expansion and innovative strategies are emerging as core drivers of Square GPV growth, potentially propelling Block’s overall performance back onto an upward trajectory.

4. Cash App Growth Bottleneck and Strategic Transformation

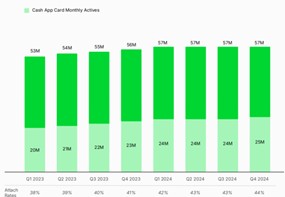

Source: Block

Block has positioned Cash App as the primary financial service platform for households earning less than $150,000 annually, covering 80% of U.S. consumers and over half of American families, highlighting its vast market potential. However, Cash App's growth has significantly slowed in recent years, with key metrics signaling a bottleneck: monthly active users grew only from 53 million in Q1 2023 to 57 million in Q4 2024, a mere 2% year-over-year increase, far below its earlier high-growth phase; gross profit growth has also sharply declined, reflecting pressures on user acquisition and profitability. Despite remaining attractive to lower-income groups, the weakening growth momentum poses a significant challenge.

The slowdown is primarily driven by intensifying competition in the P2P payment market. Venmo and Zelle boast user bases of 68.3 million and 73.2 million, respectively, far surpassing Cash App’s 57 million. Additionally, Apple and Google are escalating threats through innovative features and their extensive user bases, making it increasingly difficult for Cash App to attract new users and boost transaction volumes. Meanwhile, high interest rates and an economic slowdown have heightened financial stress for lower-income users, reducing their frequency and volume of funds added or transactions via Cash App, thus constraining platform activity and revenue growth.

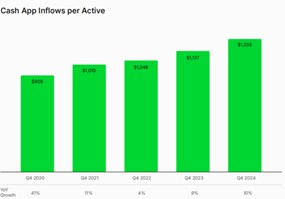

To address this, Block has shifted its strategy, focusing on enhancing engagement and revenue contribution from existing users rather than solely pursuing user base expansion. The company introduced financial services like Cash App Borrow and BNPL, with Borrow reaching 5 million monthly active users by the end of 2024—43% of loans were used for bill payments and 38% to ease cash flow pressures, reflecting strong demand. Although user growth slowed, inflows per active user rose 10% year-over-year, indicating improved user value. By boosting user stickiness, Cash App has laid a foundation for sustainable growth in a competitive market.

5. Block's Valuation and Opportunities

Source: FactSet, Visible Alpha, Morgan Stanley Research

When valuing Block, distinct valuation methods were applied to its two core business segments, Square and Cash App, to reflect their unique business characteristics and development stages. Square, as a mature payment processing business with stable cash flows and strong profitability, is better suited for the EV/EBITDA valuation method, which effectively measures its operational efficiency. In contrast, Cash App, in a high-growth phase with a heavy investment model that suppresses short-term profits, is more appropriately valued using EV/Gross Profit, as this metric better captures its revenue potential and future scalability.

· Specifically, for Square, the valuation is based on a projected 2026 adjusted EBITDA of $1.913 billion, applying an 11x EV/EBITDA multiple, slightly below the industry average. This multiple reflects Square's real-world challenges: despite its established position in payment processing, its market share is under pressure from competitors like Toast, Clover, and Shift4, which are eroding Square’s share through more targeted product features and competitive pricing strategies. Additionally, Square’s product improvements are more about catching up with peers rather than leading through innovation, limiting its valuation premium.

· For Cash App, the valuation uses a projected 2026 gross profit of $7.05 billion, applying a 2x EV/Gross Profit multiple, also below the industry average. This conservative multiple accounts for Cash App’s long-term regulatory risks (e.g., potential restrictions on BNPL and lending products) and competitive pressures, as rivals like Venmo and Zelle have significantly larger user bases, while Apple and Google’s payment services continue to encroach through innovative features and extensive user reach.

· Through a sum-of-the-parts (SOTP) calculation, Block’s target price is set at $66. This target price reflects a cautious market outlook on Block’s growth potential while capturing its exposure to competitive and macroeconomic risks.

Notably, the $66 target price is not the ceiling for Block’s valuation. If Block achieves the Rule of 40 target (where gross profit growth rate plus operating income margin equals 40%), it would significantly boost market confidence in its ability to balance growth and profitability, potentially driving an expansion in valuation multiples. Furthermore, if Block is included in the S&P 500 index, its valuation could see additional upside. S&P 500 inclusion typically increases market visibility and liquidity, attracting more institutional investors, with historical cases suggesting a potential 5%-10% valuation premium. Combining these factors, Block’s target price in an optimistic scenario could exceed $80, highlighting its potential upside upon achieving strategic goals and gaining greater market recognition.

Recommended Articles