ASML: A Technological Gatekeeper in the Age of AI

- ASML generated €28.3B revenue and €7.6B net income in 2024, with 77% from system sales and 16% YoY growth in recurring services.

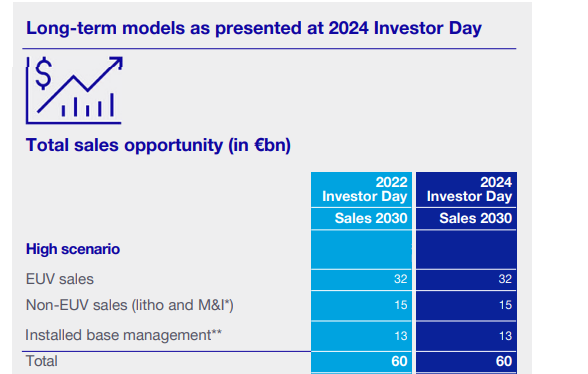

- Its €36B order backlog reflects structural demand, driven by AI compute growth and the transition to 2nm & sub-2nm chip nodes.

- High-NA EUV adoption is accelerating, but execution risk remains as only three systems were delivered in 2024.

- ASML’s valuation looks steep at 8.70x EV/Sales and 27.24x EV/EBIT, but trades at a 33% discount to its historical averages.

TradingKey - There are few businesses with as much structural leverage as ASML with regards to the worldwide semiconductor industry. Not only is it the sole manufacturer of high-volume EUV and High-NA lithography tools, the cutting-edge equipment used in chip production, completely controlling access to scaling in the future of both logic and memory, but it occupies the high end of the supply chain as well.

ASML reached €28.3 billion in revenue and €7.6 billion of net income in 2024, fueled by ongoing demand for its extreme lithography tools as well as a spike in upgrade programs. The narrative goes deeper than twelve months of performance, however. Its singular role in sustaining Moore’s Law is building a structural growth runway until 2030, and perhaps longer. Yet, under the surface of this high-tech wonder lies an underlying conflict between its significant potential and risks associated with geopolitical exposure, customer concentration, and cyclicality.

ASML is more mission-critical infrastructure builder of the AI era than cyclical piece of equipment provider. It's this nuance that makes this name a high-conviction long-term bet for those who want to play the confluence between physical tech and exponentially rising demand.

.png)

Source: Bloomberg

Behind the Machines: How Business Works and Succeeds with ASML

ASML's business model is designed for disruption as well as longevity. At its foundation are lithography tools used to transfer transistor patterns to silicon wafers, tools without which no advanced chip can be fabricated. They comprise its Deep Ultraviolet (DUV) legacy tools, its Extreme Ultraviolet (EUV) tools for 5nm and lower, and its cutting-edge High-NA EUV platforms to enable sub-2nm production.

New system sales accounted for 77% of ASML's €28.3 billion 2024 revenue, with the remainder coming from its Installed Base Management segment, comprising servicing, field upgrades, and spare parts. The latter segment accelerated 16% YoY to €6.5 billion, marking a recurring revenue source that insulates the company when it's in downcycles. The company delivered and recognized revenue from 44 EUV systems in 2024, and three High-NA EUV tools, the latter of which are currently in active customer production and generating encouraging feedback.

This combination of intense R&D and intimate customer interaction makes ASML a strategic partner, not just a supplier. While most industrial equipment companies design tools so advanced that it takes multiple years of working with foundries such as TSMC, Samsung, and Intel to incorporate them into production streams, ASML's products are guarded by patents, as well as by time, duplicating them would take a decade and billions of sunk R&D costs.

And as it continues to layer more metrology and inspection into its value stack, such as with its new eScan1100 multi-beam inspection system, it's not only providing tools, but defining the very processes by which chips are manufactured, qualified, and tuned.

.png)

Source: Q4-Deck

Competition, Differentiation, and AI-Driven Demand Shift

ASML doesn't have traditional competitors in its highest-profitability niche. Canon and Nikon, its early lithography competitors, ceded the EUV segment long ago. Tokyo Electron, Lam Research, and Applied Materials are still prominent players in deposition and etch but not in patterning, where ASML dominates.

Differentiation, and not price, provides the competitive advantage. EUV tools are over €200 million each and are not substitutable in logic scaling. The transition to AI workload, especially in data centers, HBM memory, and advanced-leading-edge GPUs, is pushing demand for new advanced logic and DRAM nodes, each with increasingly challenging lithography steps. ASML directly benefits because each new layer in chip complexity implies more exposures, more upgrades, and greater system utilization.

That aside, customer concentration is a real risk. Samsung, TSMC, and Intel are the lion's share of ASML's business, and a lag in their capex cycles causes ripples in ASML's results. China is also complicating factors: although it was 27% of system shipments in Q4-24, it will presumably trend toward normalization in 2025 as export controls ease. Political tensions are also reducing access to tools, particularly advanced ones, and putting the company at risk of regulatory whiplash.

Yet, its deep immersion in customer roadmaps and its €36 billion backlog provide insulation. In the medium term, no other firm will be in a position to provide the gear necessary for 2nm or sub-2nm production at volume. And it's not just a competitive advantage, it's systemic significance.

.png)

Source: Q4-Deck

Valuation: Overpriced but There Is Room to Rerate Depends on Execution

ASML trades at a premium across nearly all valuation multiples, sometimes significantly so, and that has long been the case. At first glance, the valuation profile looks stretched. The company’s EV/Sales multiple stands at 8.70x trailing and 7.21x forward, more than 180% above the sector median. Its Price-to-Sales ratios tell a similar story: 8.98x trailing and 7.45x forward, both over 180% above peers. Even the EV/EBITDA (24.93x TTM) and EV/EBIT (27.24x TTM) sit 20–50% higher than sector norms.

A nuanced picture unfolds upon close inspection that supports more constructive interpretation. ASML's 5-yearAverage EV/Sales of 11.72x implies its current 7.21x forward multiple translates to a 33% discount vs its own historical precedent. Also, its forward P/E of 25.75 trails its 5-year average of 39.86 by 35%. Briefly, although ASML isn't cheap relative to its competitors, it isn't overpriced relative to itself, particularly against the backdrop of structurally higher profitability due to High-NA EUV, metrology, and service monetization

Additionally, conventional screening doesn't factor in ASML's near-monopoly position. There isn't another company that has an EUV or a High-NA EUV system. All this pricing leverage, combined with close to 27% net margins and stable free cash flow conversion, underpins a premium multiple. The PEG ratio also provides guidance: ASML's non-GAAP based forward PEG of 1.34 is actually below 1.56, the industry median, meaning investors are not significantly overpaying for its growth.

A conservative base-case DCF model based on a 9% WACC, 11% CAGR in revenues by 2030, and 56% terminal margins results in a fair value estimate of between €950–1,050 per share. The upside case with more aggressive adoption of High-NA and higher AI capex tailwinds drives intrinsic value towards €1,200. But this is premised on macro stability, execution without hiccups, and continuity in semiconductor leadership.

Overall, although ASML doesn't price cheap by any measures, its valuation appears more reasonable when measured against its defensibility, generation of cash, and long-term applicability in a compute intensity- and node miniaturization-defined world.

.png)

Ycharts

Strategic Risks and The Future Path

Even with its dominance, ASML is not without risk. Export restrictions on high-end tools to China may jeopardize sales opportunities, particularly if U.S. regulations become more restrictive. While 2023-2024 featured oversized shipments to China as backlogs were filled, this tailwind has limited duration. A sudden drop in Chinese demand may put pressure on bookings and require more dependence on U.S. and Korean clients.

There's also the challenge of High-NA EUV adoption. While early feedback is encouraging and first-generation systems are processing wafers, full-volume production remains complicated and expensive. If clients push back on their roadmap due to technical or financial challenges, ASML's revenue composition and margin structure may temporarily plateau.

Finally, wider macro risks, everything from foundry capex reductions to slower AI monetization, might mute demand. The valuation of the company relies on long-term growth, and if the industry falls back into mid-cycle spending habits or sees another semi-slump, multiples would compress significantly.

Source: 2024 Annual Report

Conclusion

Yet with all these risks, ASML remains at the heart of chip production, and increasingly, of what constitutes technological sovereignty. It may prove to be the ultimate hedge of all. Catlin ASML is not just a semiconductor equipment firm, but the unappreciated engine of the AI and HPC revolution. With unparalleled IP, deeply entrenched customer relationships, and a strategy pegged to long-term industry trends, it's one of the more attractive long-term assets in tech. To institutional investors, it's an attractive combination of monopolistic economics and structural growth, albeit with some associated geopolitical risk to watch out for.

Recommended Articles