Netflix Doubles Cash Flow While Rivals Stumble

- Netflix’s 2024 free cash flow hit $6.9B, projected to rise to $8B in 2025, outpacing rivals with 27% operating margins.

- Ad-tier signups surged 30% in Q4-24, driving over 50% of new subscribers, with ad revenue set to double in 2025.

- Content spend climbs to $18B in 2025, yet cost of revenue grows just 7% YoY, boosting efficiency and 16% revenue growth.

- Valuation at 49.25 P/E and 9.61 EV/Sales suggests optimism, with $540–$580/share potential if 14–15% growth holds.

TradingKey - Netflix has come a long way from its DVD-mailing roots. Today, not only is it the world's leading subscription-based entertainment network—it's the standard bearer for a global streaming revolution. After years of expansion and reinvesting in original programming, the firm is firmly in monetization mode now.

Netflix begins 2025 with record momentum, but also stratospheric expectations. The market believes this is a company that can do it all: scale ad-supported tiers, double free cash flow, own live entertainment, and even grab a share of gaming. The question is no longer whether Netflix can grow—but whether it can grow fast enough, efficiently enough, and consistently enough to deserve its premium valuation for years to come.

.png)

Source: Q4-24-Shareholder-Letter

The Competition Heats Up: Streaming Leaders, Tech Giants, and the Battle for Attention

In a market full of streaming competitors and tech behemoths, Netflix's status is still enviable but increasingly threatened. Disney+ may have slowed its global roll-out, but still controls some of entertainment's most valuable IP. Prime Video leverages Amazon's distribution might to stay sticky in the household. Apple TV+ has invested boldly in content and provides its service for free, essentially, with device bundles. And YouTube is the default video platform for billions of users globally.

Yet Netflix continues to lead on the measures that truly matter: profitability and engagement. It boasts nearly three times the weekly streaming hours of its nearest rival and more titles in the top 10 than all other streamers combined. This is not merely volume, but instead, it is a metric of sustained user interest. At a moment when rivals are slashing content budgets, withdrawing from territories, or licensing content back to third parties, Netflix continues to invest in scripted, unscripted, live, and gaming formats.

What makes Netflix stand out is not merely the size of its content budget but also the efficiency of its platform. Personalization data stretching back decades, advanced recommendation algorithms, and user-centric design make sure that content is reaching the right viewers faster. That translates to better engagement, stronger retention, and ultimately, fewer churns.

Yet the battle for attention is intensifying. Short-form competitors like TikTok and Instagram Reels are capturing growing portions of screen time, especially among Gen Z. Netflix is aware of the trend but sees it more as an opportunity than a threat. The platforms are emerging as scouting grounds for emerging talent. Netflix has already turned viral celebrities into mainstream hits, as with shows created from YouTube and social media influencers. It’s betting that the gravitational pull of long-form storytelling remains strong, and that its service can be both launchpad and destination.

Competition is also heating up regionally. Local players in India, Brazil, and Southeast Asia offer locally relevant content at a lower cost. Netflix's response has been to double down on localization. Delhi Crime and La Palma are not just critically acclaimed—they resonate with their target markets and increase subscriber stickiness in price-sensitive markets.

While the moat is still wide, the drawbridge is not permanently raised. Competitors are closing in fast, bundling services, and experimenting with formats. Netflix's strength lies in its single-mindedness and willingness to change, but leadership will have to be maintained through ferocious innovation, especially as the next billion users are acquired in lower-ARM lands.

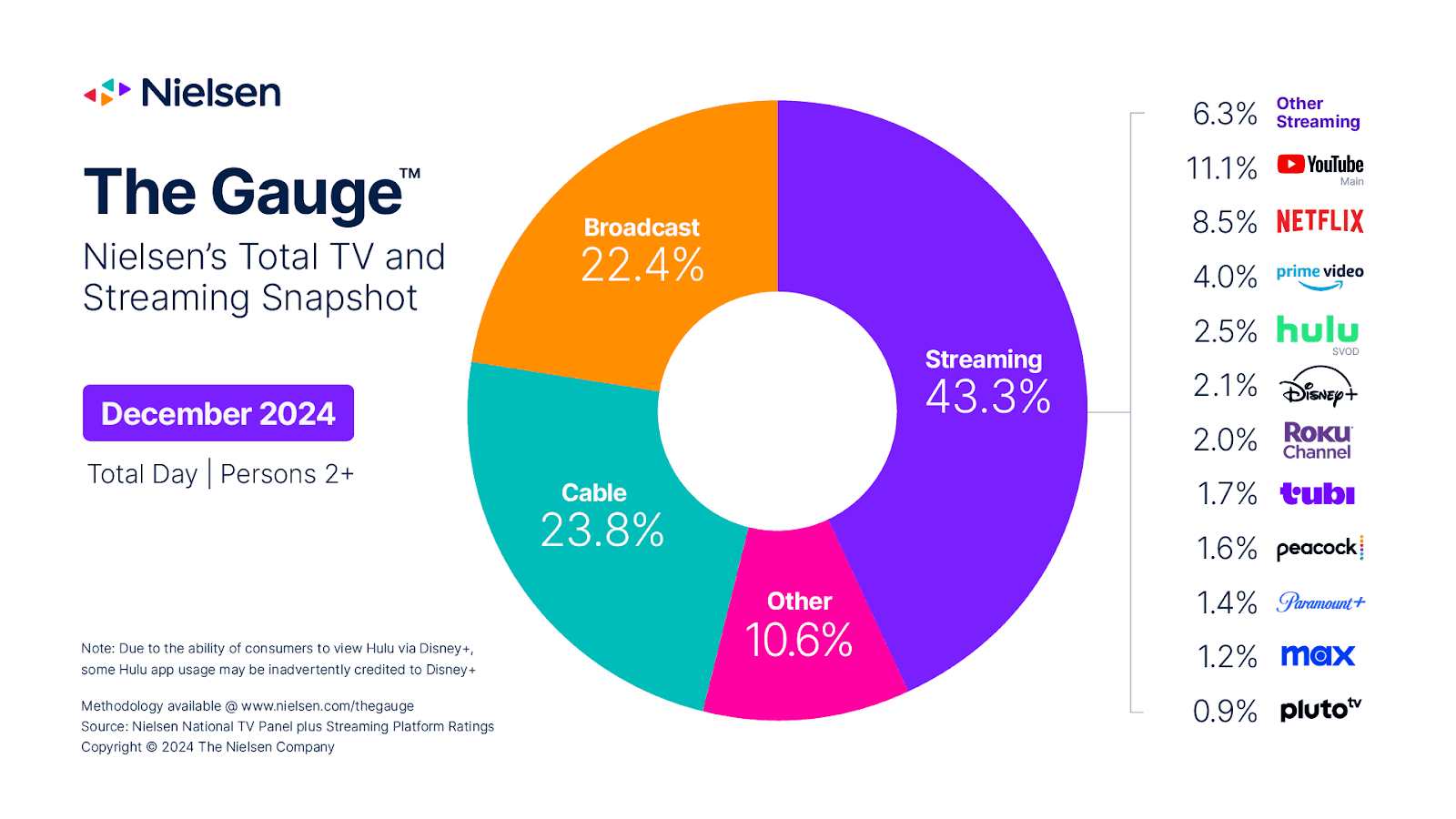

Source: Nielsen.com

Financial Engine at Full Throttle: Scaling Margins, Monetizing Inventory, and Defending Efficiency

Netflix's financial profile has changed structurally. It’s no longer a growth-at-all-costs story. Instead, it’s a case study in disciplined scaling. In 2024, he company produced $6.9 billion of free cash flow and thinks that number will increase to some $8 billion in 2025. Operating margin hit 27 percent last year, six percentage points above 2023, and management now sees 29 percent for the current year. These gains weren’t achieved through one-time cost-cutting, but through operating leverage across product development, marketing, and especially content amortization.

Despite increasing its cash content spend to roughly $18 billion for 2025, Netflix's cost of revenues increased only 7 percent YoY—well below revenue growth of 16 percent. That is testimony not just to more efficient production but to smarter windowing, licensing deals, and cross-format monetization. A hit show now creates a halo effect throughout the platform, influencing subscriber retention, merchandising, game development, and even live-event programming. The model is designed to recycle engagement back into financial returns.

Pricing has also become more surgical. Netflix now has a tiered strategy built for margin as much as affordability. The ad-supported standard plan, now priced at $7.99 in the U.S., has become a growth driver, powering over half of new signups in ad-supported markets. In the meantime, Netflix hasn't been afraid to push prices on premium plans, confident that the value-add—from superior programming to exclusive releases—justifies the hike. This two-pronged approach has kept churn in check while boosting ARM in core markets like the U.S. and Canada.

One such inflection point is advertising. Netflix is still in the early days of building a material ad business, but it’s already showing momentum. Ad-tier membership increased 30 percent sequentially in Q4, and the company is projecting to double its ad revenue again in 2025. With its in-house ad tech stack coming to the U.S. in April, Netflix is transitioning from scale to monetization mode. First-party data, improved targeting, and dynamic insertion capabilities should enable higher CPMs and more sophisticated campaigns. Longer term, the company has suggested ambitions for programmatic auctions, more granular audience segmentation, and self-serve tools—all the makings of high-margin ad revenue at scale.

The balance sheet health of Netflix is another source of flexibility. With $7.8 billion in cash, net debt of just $6.1 billion, and a long-dated maturity profile, Netflix can continue to repurchase shares—at a cost of $6.2 billion in 2024—while simultaneously investing in high-ROI content and technology initiatives. It’s a rare combination: strong FCF, durable margins, capital discipline, and platform monetization all reinforcing each other.

That said, there are boundaries to scaling efficiency. As Netflix goes deeper into lower-income markets, ARM growth will decelerate. Content costs can also rise with the push into live events and blockbuster IP. But for now, Netflix appears to be operating at a degree of financial discipline that few media companies can match.

.png)

.png)

Source: help.netflix.com

Peering Through the Valuation Lens: Risky Optimism or Justified Premium?

While Netflix’s fundamentals are strong, valuation remains an area of contention. At first glance, the numbers are raising eyebrows. Netflix trades at a trailing P/E GAAP of 49.25 and forward EV/Sales of 9.61—both roughly 4x higher than the sector median. On nearly every metric—P/E, EV/EBITDA, Price/Book, Price/Sales—Netflix ranks in the lower percentile for relative value. And yet the stock continues to trade at this premium, which suggests that investors are expecting a long runway of predictable, compounding growth.

Relative to its own five-year average, Netflix multiples have compressed somewhat, but nowhere near enough to alter the narrative. Its forward P/E ratio is still more than 130 percent above the sector median. Bulls argue Netflix deserves it because it’s no longer a media company—it’s a tech platform with unprecedented engagement and recurring cash flows. Skeptics argue even with margin expansion and growing free cash flow, the stock may be vulnerable if subscriber growth slows or ad monetization doesn’t deliver.

To assess Netflix’s valuation more quantitatively, let’s do a couple of models. First, on a simple EV/Revenue basis: if Netflix hits the midpoint of its 2025 guidance at $44 billion and maintains its current EV/Sales multiple of 9.6, its implied enterprise value is above $420 billion. Discounting that back using a WACC of 9 percent and assuming 14–15 percent top-line growth over five years provides a justified equity value of approximately $540–$580 per share. That suggests modest upside from current levels, but not much margin for error.

Peer comparisons cloud the issue. Disney trades at under 3x EV/Sales, with a mid-teens forward P/E. Warner Bros. Discovery and Paramount Global trade at even lower multiples. Of course, those companies have lower margins and declining businesses like linear TV. But the valuation gap is still disconcerting. Even compared to tech giants like Apple or Amazon, which have broader business lines and similar margins, Netflix still looks expensive on an earnings basis.

Lastly, Netflix's valuation is not today's numbers—it's a bet on five years out. If the company is able to scale its ad business, execute globally, and remain the streaming leader, the multiple can compress organically as earnings catch up. But with so much optimism already priced in, there is not much buffer for disappointment. Investors need to accept that this stock trades on narrative strength, execution precision, and forward-looking monetization—not just reported GAAP numbers.

.png)

Source: Q4-24-Shareholder-Letter

Risk Factors on the Horizon: Execution Challenges, Macro Shocks, and Platform Saturation

Even a well-oiled machine like Netflix is not without risk. The most imminent danger is one of execution. As the company attempts to juggle subscription, ad, gaming, and live formats, the risk of operational missteps grows. Rolling out an ad platform in multiple countries simultaneously and scaling engagement for original content while introducing narrative games is a high bar to clear—even for a veteran team. Should any of those components of the ecosystem fail to deliver, the platform flywheel could slow.

Currency exposure is also a risk waiting in the wings. With more than 60% of revenue generated outside the U.S., Netflix remains susceptible to foreign exchange volatility. While the company hedges about 50 percent of that risk, dollar volatility could nevertheless create reporting headwinds, especially in low-ARM markets.

Competition remains an issue as well, not as much in the old subscriber wars, but in attention. As younger viewers are flocking to short-form platforms, Netflix must continually evolve to remain culturally relevant. If programs like Wednesday or Stranger Things underperform or are delayed, that would reduce engagement and strain subscriber retention.

And finally, there's regulatory risk. As Netflix forays into advertising and interactive content, data privacy laws, content regulations, and local restrictions may make it more difficult for the company to scale efficiently. In markets like the EU, Netflix may face increased regulation of local content quotas, data usage, and tax obligations.

While none of these risks are individually existential, their convergence could materially affect margin expansion and FCF growth. Investors should remain mindful that Netflix’s current valuation embeds near-flawless execution—and perfection is rarely sustainable indefinitely.

Source: Q4-24-Shareholder-Letter

Final Thoughts: Strong Fundamentals, High Expectations, Narrow Margin for Error

Netflix has been among the most resilient and innovative entertainment companies worldwide. Its content, engagement, and monetization flywheel is firing on all cylinders. But with its stock now trading at elevated multiples, even minor disruptions could come at a high cost. The way forward will demand more than good execution—it will demand strategic agility, financial discipline, and incessant reinvention. For long-term investors, Netflix remains a compelling compounder, but one that will have to continually earn its valuation premium

Recommended Articles