Amazon’s AI & Cash Flow Boom: What’s Next?

- 2024 net sales hit $638B (+11% YoY), but operating income surged 86% to $68.6B, shifting Amazon’s focus to margin expansion.

- AWS Q4 revenue grew 19% YoY to $28.8B, contributing 58% of total operating income, as AI workloads drive demand for Amazon’s Trainium2 chips.

- Same-day delivery scaled 65% YoY, helping North America operating income rise 43% to $9.3B, while international turned profitable at $1.3B.

- AI fuels cloud dominance, while Amazon’s retail media business, with 70%+ gross margins, is now a multi-billion-dollar ad powerhouse.

- Trading at 32.4x earnings and 3.2x EV/Sales, Amazon's future hinges on AWS growth, AI execution, and macroeconomic resilience.

The Sleeping Giant Awakens: Amazon's Underappreciated Strategic Flywheel

TradingKey - Amazon (AMZN) has been a bellwether for digital commerce for years, but in the last few quarters, the narrative has changed subtly from “growth at all cost” to “profitable reinvention.”

While the market has been obsessed with trendy AI-native bets, Amazon has been infusing artificial intelligence into its sprawling empire, subtly incorporating machine learning into its logistics, retail personalization, and more importantly, turbocharging AWS with its own Trainium2 chips and foundation models. It’s less about the hype, and more about deployment scale.

The financial results for 2024 reflect this transformation. Net sales rose 11% year-on-year to $638 billion, but operating income jumped 86% to $68.6 billion, and net income almost doubled to $59.2 billion.

Amazon has now become a margin story, cash flow story, and AI infrastructure story. And the more efficient and capital-light it becomes across segments, the market may be underestimating the sum-of-its-parts opportunity, especially considering AWS’s ramping moat in the base AI stack.

.png)

Source: Q4-Deck

From Retail Chaos to Engineered Efficiency: Inside Amazon’s Business Model

Amazon's business model remains deceptively complex, operating under three segments, North America, International, and Amazon Web Services (AWS), each with its particular strategic role in enabling the larger ecosystem. North America, accounting for 61% of TTM net sales, has emerged as the profitable scale model. The segment contributed $115.6 billion in sales and $9.3 billion in operating income in Q4 2024, up 10% and 43% year over year, respectively.

Most significantly, its retail flywheel, fulfillment, Prime, third-party sellers, and advertising, shifted from being a driver of growth to being a driver of margin, helped by same-day delivery and logistical densification.

International operations, long a drag on consolidated profitability, contributed a Q4 2024 operating profit of $1.3 billion, a stark turnaround from the $419 million loss the year before. This suggests that Amazon's playbook of localized logistics and Prime-driven loyalty is now starting to produce cash outside the United States. But the crown jewel, AWS, contributed just 17% of TTM sales but a staggering 58% of operating income. AWS revenue for Q4 rose 19% year-on-year to $28.8 billion, while operating income rose 48% to $10.6 billion.

AWS today not only sits atop the cloud leaderboard but as the platform for global AI rollouts with clients as diverse as Deloitte and Palantir and the U.S. Army. Having silicon in-house (Trainium2), base models (Nova), and working with the likes of Anthropic, Amazon is transitioning from cloud provider to AI-enablement platform.

.png)

Source: Q4-Deck

Fighting the Goliaths: Amazon's Competitive Strategy

Though its scale, Amazon does not stand alone. It must contend with intense competition in almost every business line, be it Walmart in e-commerce and shipping, Microsoft Azure and Google Cloud in AI infrastructure, and Meta/Google in digital advertising.

In retail, Amazon remains the U.S. price leader, according to Profitero, but Walmart's omni-channel edge and the increase in e-commerce penetration represent a formidable threat, especially with consumers seeking value under macro headwinds. Amazon's hyper-speed delivery, 65% more overnight or same-day products YoY, and Amazon Haul and “Buy with Prime” on third-party sites, however, are increasing its moat in convenience and access.

In the cloud, AWS and Microsoft, with its OpenAI partnership, are battling for AI dominance. Microsoft has led the hype cycle with its OpenAI partnership, but AWS has created arguably the more durable offering, own chips, its dense foundation model marketplace (Bedrock), and cost-optimized AI tooling like SageMaker and Amazon Q. The 30–40% price-performance advantage of Trainium2 over GPUs and the newly released UltraServers for large-scale inference demonstrate AWS’s end-to-end cost and performance control.

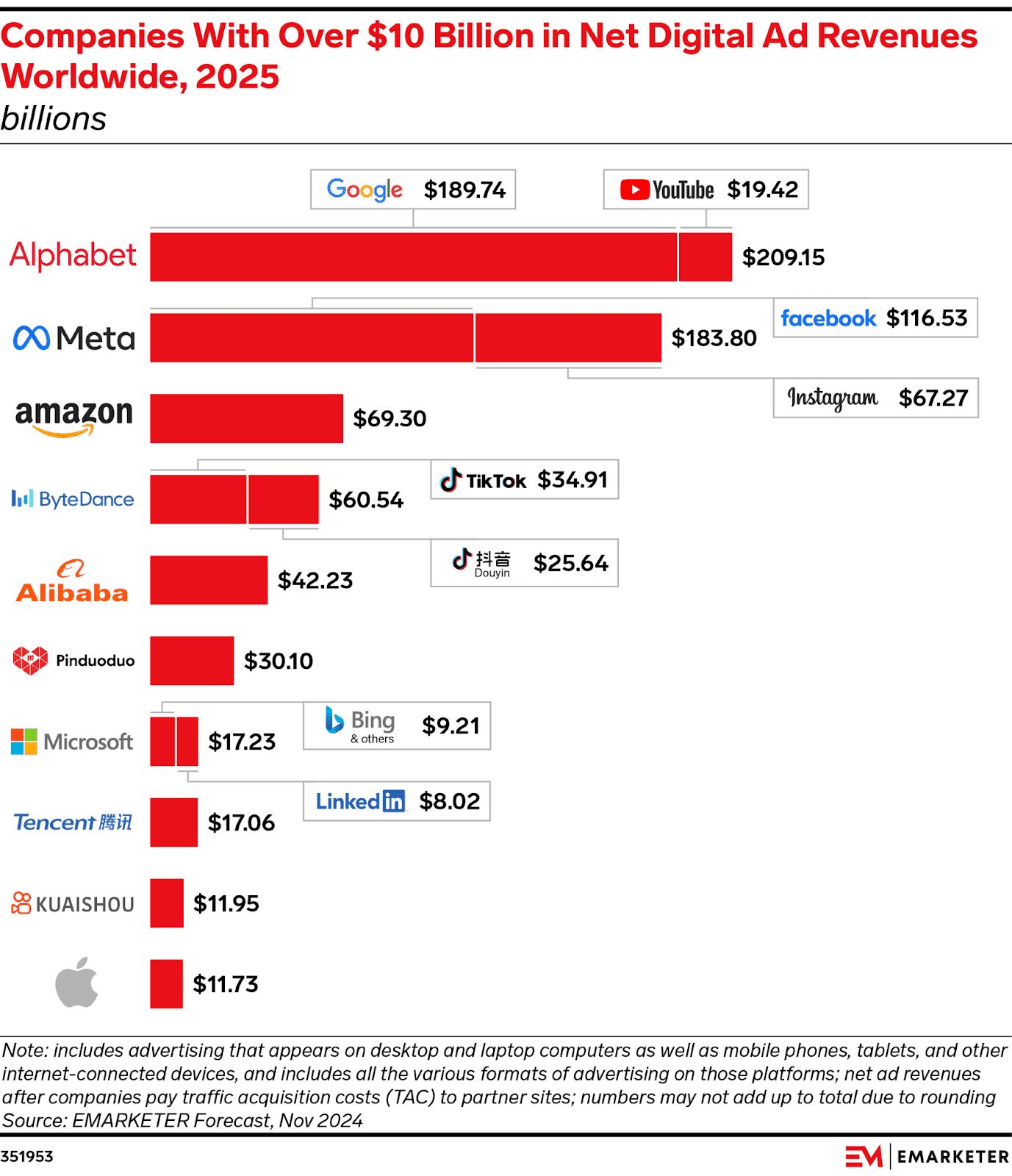

Amazon is now the third-largest after Google and Meta in digital advertising, with its retail media business leveraging first-party shopper data at scale. Its ad business, though not reported separately in this filing, is now a multi-billion-dollar business with healthy margins that helps offset retail pressure. The result? Amazon isn't just competing, it's structurally different from its competitors by integrating vertically across cloud, AI, logistics, and retail media. That's not an easy model to replicate.

Source: Emarketer.com

AI, Free Cash Flow, and Efficiency: The Strategic Flywheel Gets Momentum

The most striking thing about Amazon in 2024 is not the topline, it is the margin and cash flow narrative. Operating income doubled in just a year, driven by a 48% rise in AWS profitability and significant retail margin expansion. Net income stood at $59.2 billion, while operating cash flow stood at $115.9 billion, up 36% year-on-year. Even accounting for CapEx, the company's free cash flow stood at $38.2 billion, up 4% despite the huge investment in data centres and AI infrastructure.

This financial inflection is aided by several convergent tailwinds. Firstly, AWS is aided by operating leverage as AI workloads expand, while the mix of CapEx shifts from fulfillment to compute infrastructure. Secondly, Amazon removes unprofitable international businesses and rationalizes fixed costs. Thirdly, advertising, with 70%+ gross margin, gains share from consumer packaged good companies seeking retail data.

From the cost perspective, Amazon is better at managing dilution and CapEx. Investment in equipment and property has gone up significantly to support AWS, but principal repayments are moderating, and stock-based comp has declined YoY. This indicates a more disciplined model of investment, more specific, less sprawling.

Additionally, Amazon’s AI strategy extends across business lines. Bedrock and Trainium2 allow for the training and deployment of models more cost-effectively than with Nvidia-based infrastructure. Within the organization, AI optimizes delivery routes, warehouse robotics, and personalization in both Alexa and Prime Video. These AI optimizations, hard to model, likely are creating the “invisible margin” in Amazon’s retail and cloud businesses.

.png)

Source: Q4-Deck

Valuation Check: Pricy, but maybe worth it

Amazon now trades at 32.4 times forward GAAP earnings and 3.2 times forward EV/Sales, both premiums to the sector medians of 16.8 times and 1.2 times, respectively. On the EV/EBITDA multiple, AMZN trades at 13.3 times forward EBITDA, above its peer group average of 9.6 times but below its 5-year average of approximately 20 times.

The market is clearly pricing in operating leverage, AWS AI tailwinds, and margin expansion. But are they actually?

Let us assume our estimate of the company's fair value based on the sum-of-the-parts (SOTP) approach. If AWS's top line of $107.6 billion deserves a multiple of 9 times its operating income of $39.8 billion, then the company is worth around $358 billion. Put six times multiple to retailing on operating income of $25 billion ($150 billion) and value advertising at $120 billion (with Meta/Google retail media comparables). That equals $628 billion, before considering cash and netting out debt.

With Amazon's enterprise value standing around $1.8 trillion today, the implied multiple reflects not just base performance, but also long-term growth in AWS, advertising, and AI leadership. That's a tall order, yet one Amazon may plausibly meet, especially as AI adoption accelerates across verticals and AWS capitalizes on model fragmentation and inferencing demand.

DCF models assuming 15% CAGR in AWS, 8-10% growth in retail, 25% long-term FCF margins, and the discount rate of 9% can justify the target price in the $210–225 range, which implies moderate upside from the current level.

.png)

Source: marketscreener.com

Dangers Lurking in the Shadows: Valuation, Macro, and Margin Stress

There is a multifaceted risk profile for Amazon. The most apparent is valuation, fairly priced, any slowdown in AWS or retail margins would compress the multiple. Macro risks are also looming large. Consumer spending remains fragile, and retail, is Amazon's efficiencies aside, is still cyclical in nature. Overseas operations, while improving, remain exposed to currency fluctuations, regulatory risks (e.g., in the EU and India), and geopolitical tensions in China, where the majority of sellers and suppliers are based.

There is also a risk of execution with AI. While Trainium2 and Bedrock are promising, there is fierce competition from Nvidia, Microsoft, and Google, all of whom already have established ecosystems. Amazon's success with foundation models is not guaranteed. Finally, antitrust and regulatory pressure is increasing globally, particularly on Amazon's platform policies and use of seller data. Although these have not impacted profitability so far, they could increase compliance costs or restrict retail and advertising monetization.

Closing Statement

Amazon isn't just a growth story any more, it's now one of reinvention. With margins expanding, AWS leading the charge of AI infrastructure, and retailing cash-flowing smoothly, the market may actually be underappreciating Amazon's nascent operating model. While valuation remains rich, structural profitability and permanent AI moats show that Amazon has now transitioned to its next phase, no longer the disruptor, but the digital commerce and AI infrastructure pillar.

Recommended Articles