[IN-DEPTH ANALYSIS] Starbucks (SBUX): Can Niccol Bring the People Back to Starbucks?

Source: TradingView

Key Points

- Starbucks is the largest coffee chain in the world, boasting over 40,500 stores globally, both company-operated and licensed, where coffee and food are sold.

- Over the past year, Starbucks has been in a mini-crisis with declining same-store sales, caused by less foot traffic and aggressive expansion, ignoring the core customer satisfaction

- With the appointment of Brian Niccol as a CEO, the company plans to revitalize the operations with more advertising, simple menu options, store renovations and further digitalization

- There are certain challenges and risks, but Starbucks has the capability to limit the effects

- At the current price, the company is not exactly cheap, but the path to improvement in operations is clear, which will bring some upside potential

Company Overview

TradingKey - Starbucks Corporation is the leading roaster and retailer of specialty coffee globally. In addition to fresh, freshly brewed coffees, Starbucks’ offerings include many complimentary food items and a selection of premium teas and other beverages, sold mainly through the company’s retail stores.

Source: SEC Filings, TradingKey

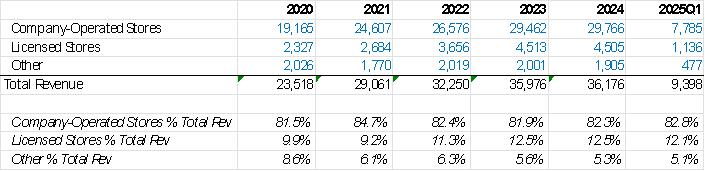

Starbucks currently has a network of over 40,000 stores – both company operated and licensed:

Company-Owned Stores: Starbucks' company-owned segment represents most of the company's revenue and includes all its stores worldwide. These are owned and managed directly by Starbucks. The company handles all aspects of operations, including staffing, inventory and store management. Revenue from company-operated stores is recognized when the sale occurs. This includes sales of beverages, food and other products directly to customers in the stores.

Licensed Stores: These are owned and operated by independent licensees. Starbucks provides the branding, products and operational guidelines, but the day-to-day management is handled by the licensee. The revenue here is generated through royalties, initial non-refundable fees and sales of products and equipment to the licensees.

A small amount of Starbucks-branded products such as packaged coffee, tea and ready-to-drink beverages are sold in grocery stores, convenience stores and other retail locations.

Source: SEC Filings, TradingKey

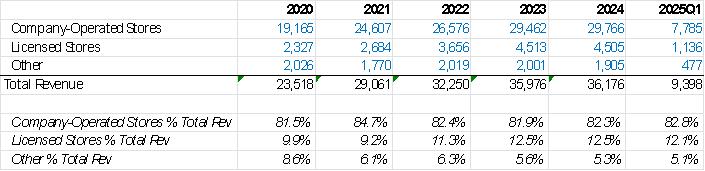

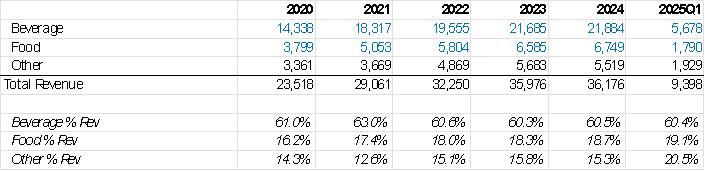

Within Starbucks stores, beverages are the main product, with over 60% of the total revenue. Food is the second highest revenue source with nearly 20% and the rest is from selling beverage-related ingredients, server ware and ready-to-drink beverages.

Source: SEC Filings, TradingKey

Despite its global outreach, Starbucks revenue is significantly concentrated in the US market, which represents 75% of the top line. China, another important market, represents less than 10%.

Source: SEC Filings, TradingKey

In the US, Starbucks market share has been between 64%-66% in terms of revenue and around 54%-55% in terms of stores. The higher revenue market share compared to the store market share implies that Starbucks is positioning itself as a rather high-end brand.

Recent challenges

Despite stable store growth in recent years, Starbucks' revenue has sharply decelerated to zero or slightly negative growth. This implies sales per store have taken a significant hit, likely due to lower traffic and eroded brand value.

Source: SEC Filings, TradingKey

There are a few reasons behind this sluggish performance:

Customer Experience Issues: Starbucks struggled with maintaining a consistent customer experience, which affected customer satisfaction and loyalty.

Increased Competition: In the U.S., Starbucks competes with players like Dunkin' Donuts and McCafé. In China, intensified competition from local brands like Luckin Coffee has impacted its market share and sales.

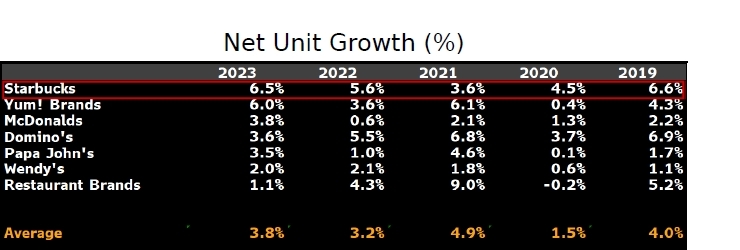

Rapid Expansion: Compared to other food chains, Starbucks' store growth has been relatively faster. Often, overly rapid expansion leads to quality control issues and brand value dilution.

Source: Bloomberg Intelligence

High Expectations from the New CEO

In September 2024, Brian Niccol joined Starbucks as CEO, a move seen as quite significant. Niccol was previously the CEO of Chipotle Mexican Grill. During his six-year tenure at the Mexican fast-food chain, he doubled the revenue and increased the profit sevenfold, with Chipotle's share price rising eightfold during that period.

Starbucks shares rose 25% on the day of the announcement, reflecting the high expectations investors have for Niccol. He introduced the "Back to Starbucks" plan, which focuses on simplifying operations, reducing menu complexity and improving efficiency and overall employee satisfaction.

Workforce Changes: As part of the restructuring, Starbucks laid off 1,100 workers and closed several unfilled positions to streamline operations and save on G&A expenses.

Less discounts but more TV promotions: Promotions have significantly reduced and the savings have been re-invested in national promotions/TV ads that are seen to have a higher return over time.

Menu simplification: The company discussed a 30% reduction in menu size for both beverage and food in order to cut the lower sales/higher waste items that add unnecessary complexity to the system. This will improve the speed and consistency with variety and customization at scale.

Investment in stores: This includes a well-stocked lobby and a grab-and-go section, as well as equipment such as seating and lighting. The expected capex for 2025 is around $2.8-3.0 billion, just a slight increase from 2024. If the majority of the capex is a maintenance capex, the assumed budget per store will be in the range of $100,000, a sufficient amount for this kind of renovation work.

Digital Innovation: Emphasizing on enhancing Starbucks' digital capabilities, including expanding mobile ordering and delivery service.

Risks and Mitigants

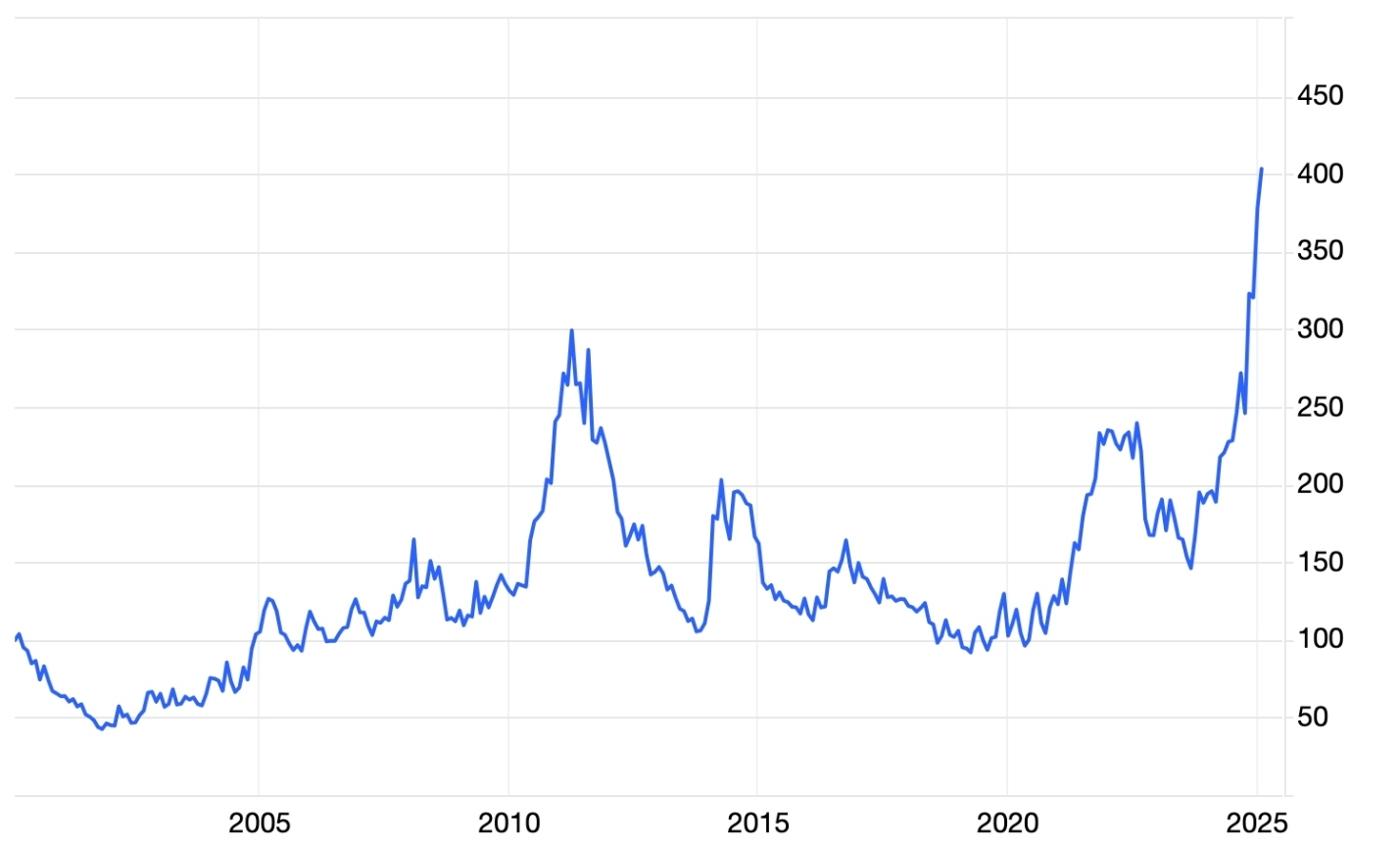

Coffee Prices Concern: The current spot price of coffee is at an all-time high of $400, well above the 10-year average of $150. Starbucks has coverage in place for the coming years, but in the past 5-6 years, the company has moved away from fully hedging the raw material price to avoid the collateral needed for such contracts.

Currently, green coffee represents 10-15% of the cost of goods sold, which is 3-4% of revenue. This means that a realized 100% increase in landed coffee prices could be offset by a 3-4% increase in menu pricing.

Source: Trading Economics

Competition: In recent years we have seen an increase in competition but somehow, the market share of Starbucks has remained rather stable, despite all the strategic missteps. With the number of new improvements, there is a high chance of seeing market share gains in the coming quarters.

Source: JP Morgan

Consumption Headwinds: An increasing number of companies have recently reported a slowdown in consumption, which could imminently affect Starbucks. However, there are several reasons to believe the negative impact may not be as severe:1) Even though Starbucks is a premium brand, the ticket size is relatively small compared to bigger-ticket items like clothing, cars and real estate. This implies that consumers may not immediately forgo buying coffee; 2 Starbucks' target customers are people with relatively higher education and earning power. This social group is likely to be less severely affected during economic downturns. 3) Starbucks has a robust loyalty program that helps retain customers long-term.

Outlook and Valuation

We expect the store count growth to decelerate from mid-single to low single digits, as management focuses on improving existing stores. Revenue per store will start to see positive growth in 2026, implying a high-single-digit increase in total revenue from 2026 onwards.

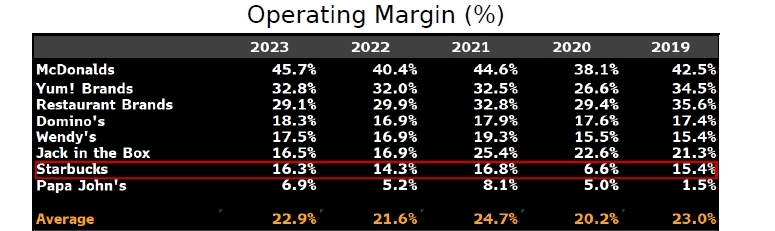

In terms of profitability, Starbucks has lower margins than other large chains, primarily because it operates a significant number of directly operated stores, unlike its peers that mostly use a franchising model. Starbucks' margin for 2024 dipped to 15%, but we expect a recovery in 2026 and 2027.

Source: Bloomberg Intelligence

With this number in mind, the expected earnings per share for 2026 is around $4.00. Currently, the company is traded at 26x 2026 PE ratio, which is within the historical average for the stock.

Recommended Articles