2 Artificial Intelligence (AI) Stocks That Could Go Parabolic

Many companies have witnessed a tremendous increase in their share prices over the past couple of years thanks to the growing adoption of artificial intelligence (AI), which is not surprising as this technology has created massive demand for both hardware and software.

The good part is that AI is currently in its early phases of growth. IDC estimates that global AI spending could increase at an annual rate of 29% over the next five years, hitting $632 billion in value in 2028.

This robust increase in the adoption of AI could help make companies like Nvidia (NASDAQ: NVDA) and Snowflake (NYSE: SNOW) make a parabolic move, which refers to the rapid rise in the stock price of a company in a short time (just like the right side of a parabolic curve).

Nvidia stock has already gained immensely in the past couple of years thanks to its pioneering role in the AI hardware market, but Snowflake has headed south because of its slowing growth. More specifically, Snowflake stock is down over 42% in 2024, while Nvidia has jumped 152%.

Let's look at the reasons why AI could help one of these names make a parabolic jump and head even higher while also allowing the beaten-down Snowflake to rise rapidly.

Nvidia's new Blackwell chips could fuel its rally

The robust demand for Nvidia's data center graphics processing units (GPUs) based on the Hopper architecture has played an instrumental role in the company's outstanding growth in recent quarters. Demand for its H100 Hopper AI GPUs was so solid that the chip reportedly commanded a waiting period of as long as a year.

The company followed up this chip with the more powerful H200 processor, whose production ramp and shipments started in the previous quarter.

Nvidia points out that the shipments of its Hopper-based GPUs will increase in the second half of the current fiscal year thanks to improved supply and availability, suggesting that the H200 could continue to bring in more business for the company. However, all eyes are set on Nvidia's next generation of AI chips based on the Blackwell platform.

The company started sampling the Blackwell processors to customers last quarter. Nvidia says that the production ramp of the Blackwell chips will begin in the fourth quarter of the fiscal year. More importantly, Nvidia claims that the "demand for Blackwell platforms is well above supply, and we expect this to continue into next year."

Additionally, CEO Jensen Huang recently told CNBC that Blackwell is witnessing "insane" demand. That's not surprising as the company has already lined up multiple customers that include the likes of Microsoft, OpenAI, Meta Platforms, and others for this chip that's reportedly going to deliver a 4 times jump in performance over the Hopper chips.

Morgan Stanley estimates that Nvidia could sell $200 billion worth of Blackwell-based server systems next year. While that seems like an ambitious target, the pace at which Nvidia's data center revenue is growing suggests that it could indeed hit that mark. More specifically, Nvidia's data center revenue has more than tripled in the first six months of fiscal 2025 to $49 billion from $14.6 billion in the same period last year.

The current run rate suggests that Nvidia could end the year with $98 billion in data center revenue. That would be more than double its fiscal 2024 data center revenue of $47.5 billion. Morgan Stanley's forecast suggests that Nvidia may be able to double its data center revenue once again in the next fiscal year. If that's indeed the case, the semiconductor giant's top line could land well ahead of the $178 billion revenue that analysts are expecting from the company next fiscal year.

That could reignite Nvidia's stupendous rally once again following a flat performance in the past three months and could even help the stock go on a parabolic run.

AI is helping Snowflake build a solid revenue pipeline

Snowflake is a cloud-based data platform provider on which customers store and consolidate data so that they can derive insights using that data, build applications, and even share that data. And now, Snowflake is adding AI-focused capabilities to its data cloud platform.

The company has been renting GPUs so that it can "fulfill customer demand for our newer product features," suggesting that Snowflake's AI offerings are gathering momentum. Snowflake enables its customers to develop AI applications using large language models (LLMs) and deploy those models within the secure environment of its data cloud platform.

Snowflake customers can build custom chatbots, use the company's Copilot feature to speed up their tasks and extract data from documents, among other things. Snowflake management pointed out on the August earnings conference call that more than 2,500 customers were using its AI offerings in its fiscal 2025's second quarter (ended July 31).

It is worth noting that Snowflake ended the quarter with just over 10,000 customers, indicating that it is well-placed to upsell its AI services to a large customer base. The good part is that the growing adoption of its AI tools is leading to increased spending by existing customers.

The company's net revenue retention rate stood at 127% in fiscal Q2, a metric that compares the spending by its customers at the end of a particular period to the spending by the same customer base in the year-ago period. So, a net revenue retention rate of more than 100% means that it is winning a bigger share of customers' wallets.

Even better, the quality of Snowflake's customer base seems to be improving as well. This is evident from the fact that the number of customers who have generated more than $1 million in product revenue for the company increased by 28% year over year to 510 in the previous quarter, as compared to the 21% growth in the overall customer base.

This combination of higher spending by its existing customers as well as the addition of new customers explains why Snowflake's remaining performance obligations (RPO) shot up a remarkable 48% year over year last quarter to $5.2 billion. That exceeded the 30% year-over-year growth in the company's product revenue.

As RPO refers to the total value of a company's future contracts that are yet to be fulfilled, the faster growth in this metric as compared to its revenue growth suggests that Snowflake's revenue growth is likely to accelerate in the long run. Of course, the investments that the company is making are weighing on its margins, with its non-GAAP (adjusted) operating margin dropping to 5% last quarter from 8% in the year-ago period.

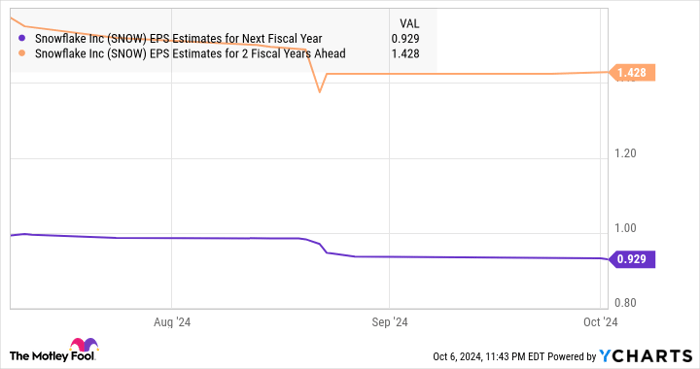

That's why analysts are expecting Snowflake's bottom line to shrink to $0.61 per share in fiscal 2025 from $0.98 per share in the previous year. However, it is expected to return to terrific bottom-line growth from the next fiscal year.

SNOW EPS Estimates for Next Fiscal Year data by YCharts

As such, investors should consider buying Snowflake stock while it is down, as the emergence of AI and the acceleration in its growth thanks to the adoption of this technology could send the stock flying.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $814,364!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of October 7, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms, Microsoft, Nvidia, and Snowflake. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles