Is It Time to Load Up on Aurora Cannabis Stock?

The global cannabis market stands on the cusp of a remarkable period of growth. Industry projections suggest it could grow from $57 billion in 2023 to $444 billion by 2030. This potential 7.7-fold increase over seven years translates to a compound annual growth rate of 34%, dwarfing the growth rates of many traditional industries.

Against this backdrop of industrywide potential, Canadian marijuana titan Aurora Cannabis (NASDAQ: ACB) has emerged as an unexpected bright spot in 2024. While most of its Canadian counterparts have wilted this year, Aurora's shares have blossomed with a 13% gain year to date. This performance starkly contrasts with industry peers Canopy Growth Corp. and Tilray Brands, which have seen their stocks wither by 18.5% and 28.2%, respectively.

Image source: Getty Images.

Aurora's resilience in a challenging market for marijuana stocks raises an intriguing question for speculative growth investors: Is Aurora Cannabis stock still ripe for the picking after its strong performance over the first three quarters of 2024? Let's dig deeper to unearth the answer.

Medical cannabis: A high-margin focus

Aurora Cannabis has carved out its niche primarily in the medical cannabis market. This strategic focus appears to be bearing fruit. In the first quarter of FY 2025, Aurora reported record global medical cannabis net revenue of $47.2 million Canadian dollars, marking a 13% increase from the same period a year ago.

The medical cannabis segment offers higher margins, compared to its recreational counterpart. To wit, Aurora's adjusted gross margins for medical cannabis have consistently hit or exceeded the company's 60% target in recent quarters, reaching a healthy 69% in Q1. This emphasis on high-margin medical sales could be a sturdy foundation for Aurora's future growth and profitability.

Financial health improving

Aurora Cannabis has made significant strides in improving its financial position. The company achieved positive free cash flow of CA$6.5 million in Q1 FY 2025, a milestone Wall Street wasn't expecting until at least calendar year 2026. This achievement is particularly noteworthy given the company's history of cash burn and shareholder dilution.

Aurora has also worked to strengthen its balance sheet. As of the close of Q1 FY 2025, Aurora had approximately CA$182 million in cash and cash equivalents. This cash position provides the company with financial flexibility as it navigates the evolving cannabis market.

Global expansion and market potential

Aurora Cannabis has established a presence in key international markets, including Germany, Australia, and the United Kingdom. Germany recently became the largest European Union (E.U.) country to legalize cannabis for recreational use. However, the initial phase of this legalization focuses on personal possession and cultivation, along with non-profit "cannabis clubs" for distribution, rather than commercial sales.

This structure limits immediate opportunities for large-scale commercial operators like Aurora. Despite these current restrictions in Germany, Aurora's strong position in the country's medical cannabis market may offer significant advantages as regulations evolve. This international footprint could prove valuable as the global cannabis market continues to develop and grow.

Challenges remain

Aurora Cannabis still faces significant challenges despite these positive developments. The company operates in a highly regulated industry with ongoing legal uncertainties in multiple key geographies. Competition from both legal and illicit sources remains fierce. The Canadian market continues to be burdened by high excise taxes and costly regulations.

Perhaps most importantly for stock investors, Aurora has a history of diluting shareholders to raise capital. The company has more than doubled its outstanding share count in the past three years. The recent positive free-cash-flow news is encouraging, but investors should be aware of the potential for future dilution.

Time to buy?

Aurora Cannabis has been making some impressive moves lately. Its turnaround strategy is starting to pay off, with a smart focus on high-margin medical cannabis and a push for better efficiency. The company has even managed to achieve positive free cash flow -- no small feat in this industry. Plus, their strong international presence and the bright outlook for global cannabis growth are points in the marijuana titan's favor.

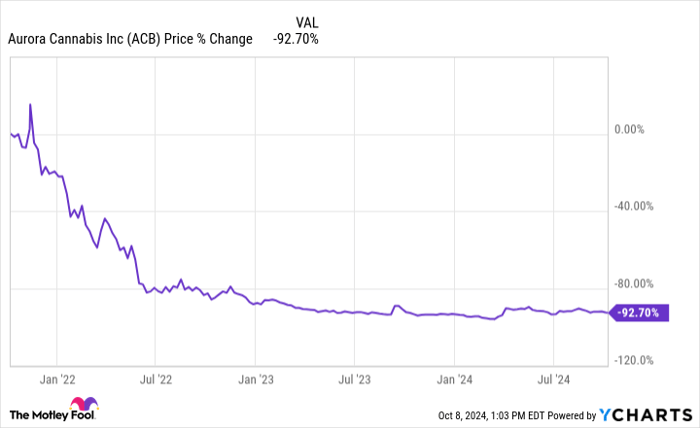

But let's not get ahead of ourselves. The cannabis industry is still in its nascent stages, with regulations that can change at the drop of a hat. While Aurora's stock has seen some nice gains in 2024, it's worth remembering that it's taken quite a beating over the last several years (see graph below). Growing pains in the industry have been real, and Aurora hasn't been immune.

ACB data by YCharts.

What's the bottom line? If you're thinking about investing in Aurora Cannabis, you need to go in with your eyes wide open. This isn't a stock for the faint of heart -- it's for those who can handle stomach-churning volatility in the hunt for unusual growth opportunities.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $20,363!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,938!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $378,539!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of October 7, 2024

George Budwell has no position in any of the stocks mentioned. The Motley Fool recommends Tilray Brands. The Motley Fool has a disclosure policy.

Recommended Articles