Better Semiconductor Stock: Taiwan Semiconductor vs. Intel

Among companies in the semiconductor contract manufacturing space, two stocks that have gone in opposite directions this year are Taiwan Semiconductor Manufacturing (NYSE: TSM), or TSMC for short, and Intel (NASDAQ: INTC). The latter has struggled with its stock down more than 50% this year, while the former is up more than 70% over the same period.

While TSMC has been the clear winner this year, the question is which will be the better stock moving forward. Let's take a closer look at each and decide.

Taiwan Semiconductor Manufacturing

As the largest semiconductor contract manufacturer in the world, TSMC has been a big beneficiary of the artificial intelligence (AI) infrastructure buildout, as its customers clamor to make more advanced AI chips to try to keep up with demand. The company counts AI chipmakers Nvidia, Broadcom, and Advanced Micro Devices among its largest customers, and it is estimated that it has a 90% market share when it comes to making advanced chips.

With large tech companies continuing to ramp up their AI-related capital expenditures (capex), and AI models needing more and more graphics processing units (GPUs) and other chips such as CPUs (central processing units) as they advance, TSMC appears to have a long runway of growth in front of it. At the same time, more powerful smartphones and PCs will be needed to run AI functionality on edge devices, which will also benefit the company. TSMC's largest customer remains Apple, which is rolling out a new AI-powered iPhone.

With demand for its service high and capacity tight, TSMC has also been seeing strong pricing power even as it adds production capacity. According to Morgan Stanley, the company has already told customers it is raising prices next year, including by 10% for AI semiconductors.

Meanwhile, Bain & Company recently predicted that there could be a chip shortage in high-end chips in the coming years due to soaring demand for GPUs and AI-capable smartphones. Such a scenario would only improve TSMC's already strong position in the semiconductor supply chain and lead to more pricing power and capacity expansion opportunities.

TSM PE Ratio (Forward 1y) data by YCharts.

With the stock trading at a forward price-to-earnings ratio (P/E) of only about 21 based on next year's analyst estimate, and a price/earnings-to-growth ratio (PEG) of about 1, the stock is attractively valued given the opportunity in the growth in AI-related chips. A PEG under 1 is typically considered undervalued, and growth stocks often have PEGs well above 1.

Intel

While running a semiconductor contract manufacturer in this environment may sound easy, Intel's story is a testament that it is not. The company launched its third-party foundry business in 2021 to kickstart growth, but instead it has just been an anchor on Intel's results.

In addition to needing the latest leading edge technology, foundries also need scale and high utilization rates to be successful. In addition, this is a capital-intensive business as it costs a lot of money to build and equip a new foundry. While Intel has poured money into the business, the results have been a large drag on the company.

In the second quarter, its foundry business only grew its revenue 4% year over year to $4.3 billion, while its operating loss jumped from $1.87 billion to $2.83 billion. The unit has lost $5.3 billion through the first half of this year. These mounting losses in its foundry segment have played a big role why the stock has struggled.

Image source: Getty Images.

While Intel's other businesses aren't lighting the world on fire, they are doing OK. Its overall product revenue rose 4% to $1.8 billion, while product operating income climbed 16% to $2.9 billion. The company is seeing solid results from its Client Computing Group, where it recently launched its new AI CPU, Lunar Lake.

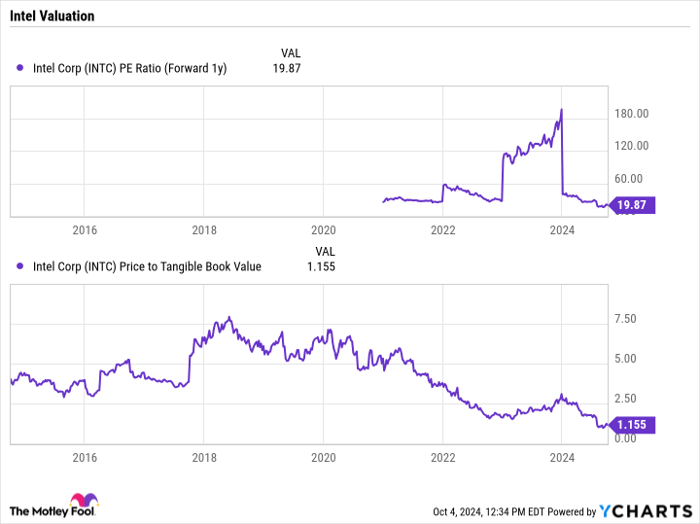

After its most recent earnings report, Intel announced plans to turn its foundry business into an independent subsidiary, where it could eventually pursue outside funding. This could be the first step in eventually spinning off the struggling business, which could be a benefit for its stock. Intel currently trades at a forward P/E of 20 times next year's analyst estimates, which isn't cheap given its struggles. However, the foundry business is a huge drag on the earnings part of that equation.

If its core product business could generate $2.10 in earnings per share (this assumes about $12 billion in product segment operating income, a 25% tax rate, and 4.3 billion shares), its core business would be worth closer to an 11 times forward P/E. There is also value in its stake in Mobileye and Altera, and the foundry business still has a lot of asset value given the money invested into it.

Intel's inexpensive valuation can also be seen in its price-to-tangible book value ratio, which is under 1.2. That shows that the stock is trading just above the liquidation of its assets, which is rare to see in a large tech stock.

INTC PE Ratio (Forward 1y) data by YCharts.

TSMC vs. Intel

When deciding between investing in TSMC and Intel, I think the match-up is a bit closer than it might appear.

TSMC is the growth story that should continue to benefit from the AI infrastructure buildout and strong pricing power. As AI models advance and leading tech companies continue to pour money into AI, the company is very well positioned to benefit.

Intel, meanwhile, is a potential turnaround play. The stock is very cheap, trading near asset value, and management has some levers to pull to extract value, such as spinning off its foundry business down the road.

I give the slight edge to TSMC given its growth, but I would not count Intel's stock out. Luckily, investors don't have to decide and can own both stocks.

Should you invest $1,000 in Intel right now?

Before you buy stock in Intel, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Intel wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $765,523!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 30, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom, Intel, and Mobileye Global and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

Recommended Articles