Billionaire Investor Pushes for Changes at CVS. Is Now the Time to Buy the Stock?

Billionaire investor Larry Robbins of hedge fund Glenview Capital Management has taken a large stake in healthcare company CVS Health (NYSE: CVS) and has met with management on ways to help turn around the struggling business. According to The Wall Street Journal, Glenview has amassed about a $700 million stake in the company.

Meanwhile, according to CNBC, CVS has met with advisors to conduct a strategic review of its business. The review started before Glenview became involved.

The question is: With a billionaire investor taking a large stake in CVS, should other investors follow suit?

CVS' struggles

CVS has three main businesses: Healthcare benefits, a retail pharmacy, and a pharmacy benefit manager (PBM). All the businesses have had their share of struggles.

The healthcare benefits business, which includes health insurer Aetna, has struggled because of higher healthcare costs and utilization. Its medical benefit ratio (MBR), a measure of claims to premiums earned, increased by 340 basis points last quarter, to 89.6%.

In short, the higher the number, the less money the company is keeping. Healthcare insurance providers must pay out 80% of premiums in healthcare costs and quality improvement activities, and 85% if they are selling to large groups of 50 or more employees.

CVS credited the large increase in its MBR last quarter to higher Medicare Advantage utilization, lower Stars ratings, and increased Medicaid acuity (illness severity). The Stars system is based on quality of care and is used to determine Medicare bonus payments. The higher MBR caused the segment to see a 39% decline in its adjusted operating income, despite a 21% increase in revenue and 5% increase in members.

The company also updated its guidance to reflect current medical cost trends, which it said could be higher than in the first half. It said if this occurs, it could be forced to take a premium deficiency reserve in its Medicare business, which means that current payment reserves and future premiums won't be enough to pay out unpaid claims and future claims. It now expects its MBR to be 90.6% to 90.8% for the full year, up 80 basis points to 100 basis points versus its previous guidance.

The retail pharmacy business has also been under pressure from reimbursement rates. This has been an industrywide problem, as PBMs have relentlessly pushed down reimbursement rates to the point where pharmacies lose money by filling some subscriptions. CVS does own the largest PBM in Express Scripts, so it has not seen the same type of effect as rival Walgreens Boots Alliance.

However, the segment's second-quarter adjusted income was down 12%, despite a 4% increase in revenue and 4% increase in subscriptions being filled.

CVS' PBM segment has been the best-performing of its businesses. It saw a slight 1% increase in adjusted operating income despite losing a large client, which caused the segment's revenue to decline by 9% and claims processed to sink by 18%.

Image source: Getty Images.

Turnaround potential

The company will have the opportunity to fix the Aetna business through better underwriting when it reprices the business next year. It appears to have underpriced its policies this year to win new business, which proved to be an error. CVS said there will be significant price increases in 2025 for individual businesses, while for Medicaid, price increases will go into effect on nearly half of its book at the start of the year. Overall, this issue should be fixable over time.

The retail pharmacy and PBM businesses, meanwhile, are intertwined in many ways. After all, it is PBMs like the company's Express Scripts business that are causing the reimbursement pressures at pharmacies. There eventually will need to be a more sustainable model put in place for pharmacies. But if this does happen, how much benefit the company as a whole will get is uncertain, given that it owns both a large retail pharmacy and a PBM.

At this point, I think the company prefers the reimbursement pressure to the benefit of its PBM and to the detriment of pharmacies, as it is hurting its rivals more, and they are reducing their store counts. CVS has already been taking pharmacy share as a result, and this will likely only increase as Walgreens closes stores.

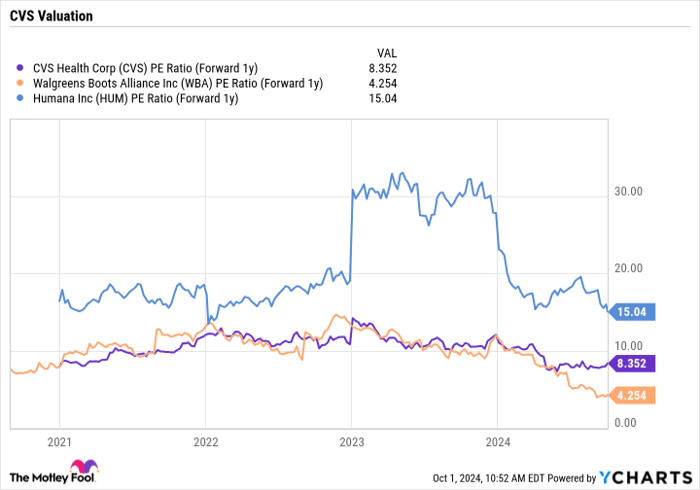

From a valuation perspective, the stock is inexpensive, trading at a forward price-to-earnings (P/E) of about 8.4 times based on 2025 analyst estimates. This falls in between a health insurer like Humana and struggling pharmacy Walgreens.

CVS PE Ratio (Forward 1y) data by YCharts.

The valuation gap between health insurers and pharmacies could make it interesting for the company to potentially spin out the Aetna business, where it should be able to get a higher multiple. Regardless, it does look like there are levers for the company to pull to help turn around the business and create shareholder value moving forward.

I think investors can follow Glenview into the name and be buyers of CVS stock.

Should you invest $1,000 in CVS Health right now?

Before you buy stock in CVS Health, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CVS Health wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $765,523!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 30, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool recommends CVS Health. The Motley Fool has a disclosure policy.

Recommended Articles