You'll Never Guess the Best-Performing Stock in the Nasdaq-100 Last Quarter. Is It Still a Buy?

With the surge in tech stocks this year, it may be surprising that the best-performing stock in the tech-heavy Nasdaq-100 index last quarter wasn't a chipmaker or software company riding the artificial intelligence (AI) wave. It was PayPal (NASDAQ: PYPL).

The stock of the fintech company surged 34.5% in the quarter, marking its best quarterly performance since 2020. The company's strong performance comes amid signs that the turnaround plan CEO Alex Chriss enacted is starting to take hold.

Can the stock's momentum continue?

Turnaround taking hold

When Chriss took over PayPal, it was seeing solid revenue growth but gross margin pressures. During the past decade, its gross margin had shrunk from 52.6% in 2014 to 39.6% in 2023 as much of the company's growth had started coming from lower-margin sources. This caused gross profits to shrink from 2021 to 2023 despite the company growing revenue by more than 8% both in 2022 and 2023.

In Q3, the company showed progress fixing this issue that has been plaguing it the past few years. In the quarter, its transaction margin dollars, which is similar to gross profits, rose 8% to $3.6 billion. It was PayPal's highest transaction margin dollar growth since 2021 and the first time in over two years that its BrainTree business contributed to transaction margin dollar growth.

BrainTree, PayPal's unbranded payment processing solution, has been a solid revenue driver for the company, but the lower-margin business has also been a part of the problem, as companies have moved more business there.

Since taking over at PayPal last fall, Chriss has set out to innovate, and the company has introduced a number of attractive value-added solutions to help drive sales for merchants.

One of PayPal's most exciting innovations under Chriss is an AI solution called Fastlane that lets consumers check out with a single tap without having to set up an account or provide credit card information to retailers. Having to create accounts and add credit card information often leads to customer frustration and unfinished purchases, leaving a lot of money on the table. In tests with early adopters, PayPal said returning Fastlane users are converting at a nearly 80% average versus an industry average of about 50%.

Image source: Getty Images.

This type of innovation helps PayPal customers make more money, so it's highly desirable. The product became widely available to U.S. merchants only in August, and so is yet to show up in its results.

The company has also introduced a number of marketing products, including smart receipts and advanced offer platforms, that will give retailers the ability to customize offers and make product recommendations based on what types of items customers have bought across both their own and other merchants' websites.

With this innovation, PayPal has also been looking to improve pricing for both its branded and unbranded products based on commercial outcomes. It credited this price to value approach as the main reason BrainTree was able to positively contribute to transaction margin dollar growth.

Chriss said that while this process will take time, the company is already having conversations with its top customers about pricing and focusing on commercial outcomes. He said the company is still in the early days, but that he is encouraged by the initial actions related to price value.

Is there more upside in the stock?

With Fastlane just being made generally available in the U.S. in August and its price to value strategy in its early days, it appears there is a lot more potential growth in PayPal's future. The company has introduced some great marketing and fraud protection solutions that should propel growth and help margins.

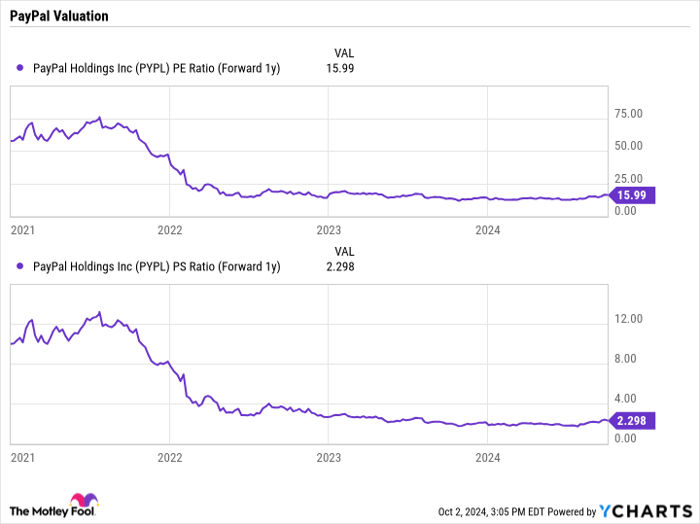

At the same time, despite the stock's outperformance in Q3, it is still attractively priced at current levels. PayPal stock trades at a forward price-to-earnings (P/E) ratio of 16 times and a forward price-to-sales (P/S) ratio over 2 times based on 2025 estimates. Both of those metrics are well below where the stock traded just a few years ago.

PYPL PE Ratio (Forward 1y) data by YCharts.

With Chriss at the helm, PayPal's turnaround is going smoothly and its future looks bright. The best part is the stock is still cheap and the turnaround still looks to be in its early stages.

As such, I'd be a buyer of the stock at current levels.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 768% — a market-crushing outperformance compared to 167% for the S&P 500.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and PayPal made the list -- but there are 9 other stocks you may be overlooking.

See the 10 stocks »

*Stock Advisor returns as of September 30, 2024

Geoffrey Seiler has positions in PayPal. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends the following options: short December 2024 $70 calls on PayPal. The Motley Fool has a disclosure policy.

Recommended Articles