Where Will Celsius Holdings Stock Be in 3 Years?

Celsius Holdings (NASDAQ: CELH) is one of the best-performing stocks of the last 10 years. Shares of the sugar-free energy drink brand that focuses on selling to women and health-conscious consumers were up 18,000% in the last decade, driven by huge market share gains in the United States.

However, in 2024, the momentum around the brand took a turn for the worse. Revenue growth has slowed this year, and Celsius stock has fallen along with it. As of this writing, the shares are down 66% from all-time highs, with most of the losses coming in the past three months. Investors are undeniably nervous as sales growth went from 100%-plus to just 23% last quarter.

The company is at a crossroads. The next few years will be crucial for Celsius as it tries to gain more market share in the United States and aggressively expand internationally. Where will the stock be in three years' time? Let's dig into the numbers and try to make some estimates.

An energy drink slowdown, and volatility with PepsiCo

Celsius took off like a rocket in the United States by positioning itself counter to the legacy energy drink brands. It is the opposite of many people's perception of energy drinks: sugar-free and focused on fitness enthusiasts. This allowed it to expand the energy-drink category in the United States, with an estimated 10% to 12% of sales today going to the brand.

Double-digit market share from basically zero a decade ago is a phenomenal achievement. But investors are not very nostalgic. It is about what Celsius is doing today and can do in the future. This year has been rough for the brand so far, hitting a double whammy of headwinds that knocked down its revenue growth from 100% in 2023 to 23% last quarter.

First, the entire energy-drink category is slowing down. Lower consumer demand is hitting every brand, including competitor Monster Beverage. Second, Celsius is receiving fewer orders from PepsiCo this year, its main distribution partner in the United States. Pepsi is destocking its inventory of Celsius to help its cash flow, which has affected revenue for the last few quarters.

While these are two concerns to watch out for, I don't think they will affect Celsius over the long term. Macroeconomic headwinds will eventually abate, and Pepsi will eventually normalize its purchases with consumer spending across different retail outlets. What is important is that Celsius continues to grow its market share year over year in the energy drink category. That is happening in 2024.

International expansion and market share gains

Celsius is a huge growth story, but that has mainly come in North America. International revenue was a measly $19.6 million last quarter, albeit growing 30% year over year.

Management did not focus much outside the huge North American market in the last 10 years, but that will change over the next few years. Celsius has partnered with distributors to enter Australia, New Zealand, the United Kingdom, and France to make a big push with the brand in 2025. Investors should be tracking this line item closely to see whether its success can be replicated in new countries.

The second thing investors should be focusing on is market share gains in the United States. Celsius has approximately 12% of energy drink retail sales when including online channels, with Monster Beverage and Red Bull at close to 30% and 40% share, respectively.

There is still lots of room to push for consumers to switch energy drink brands. If it can hit 15% or even 20% market share within the next three years, that would be a lot of revenue growth for the company.

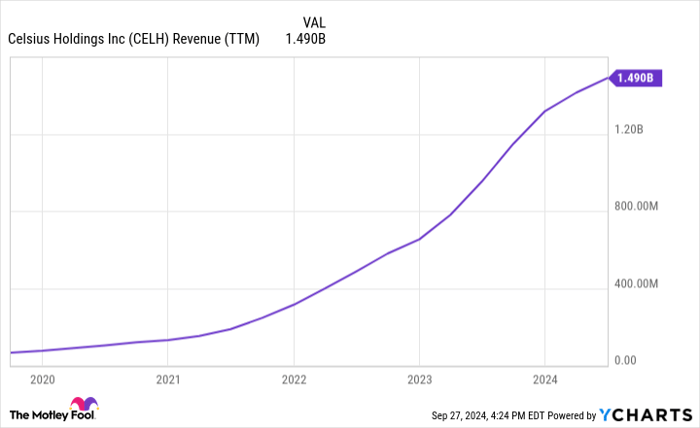

CELH revenue (TTM); data by YCharts. TTM = trailing 12 months.

Where will Celsius stock be in 3 years?

If we combine the market share gains and the potential for international growth, I think Celsius can keep growing its sales by 20%-plus annually for the next three years. That would bring revenue from $1.49 billion in the last 12 months to $2.57 billion in three years.

The company currently has an operating margin of 22.5%, which would equal $580 million in operating earnings within three years based on the above revenue estimates. Again, these are just estimates, but a good illustration of the potential paths forward for Celsius if it can keep gaining market share and grow internationally.

At a current market capitalization of $7.6 billion, these three-year earnings estimates would equal a forward price-to-earnings ratio of 13. This is much cheaper than the market average and what the stock has traded at historically.

Taking all this into consideration, I think Celsius stock will be higher -- perhaps even doubling from today's levels -- in three years.

Should you invest $1,000 in Celsius right now?

Before you buy stock in Celsius, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Celsius wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $744,197!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 30, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Celsius and Monster Beverage. The Motley Fool has a disclosure policy.

Recommended Articles