Is Meta Platforms Stock A Buy?

Meta Platforms (NASDAQ: META) has been a dream stock for investors, returning 90% over the past year and an even more spectacular 548% since its low in 2022, when shares briefly traded under $90.

Compared to a disappointing slowdown after the worst of the pandemic, the social media giant reclaimed its operating and financial success by focusing on core strengths. An all-in approach toward artificial intelligence (AI) as a new growth driver has given shareholders plenty to cheer about.

The headlines are positive, but do they make the stock a buy today? Let's discuss whether the rally in Meta Platforms can keep going.

MetaAI driving strong growth in 2024

Meta Platforms is globally recognized through its family of apps and platforms, including Facebook, Instagram, and WhatsApp, that help people around the world stay connected. Its vast user base and significant reach (3.3 billion daily active people) have proven highly attractive to advertisers.

The trends from Meta this year have been very impressive. In the fiscal second quarter (for the period ended June 30), total revenue climbed by 22% year over year, propelled by a 10% increase in ad impressions delivered across the family of apps while the average price per ad was also 10% higher.

A big part of the momentum is the impact of new AI features on advertisement performance. Improved ad targeting based on AI recommendations led to higher conversions for marketers, which in turn supports higher demand for advertising campaigns. Meta also rolled out AI tools like its MetaAI virtual assistant with text and image generation to keep users engaged.

These dynamics, with cost-controlling measures, translated into strong profitability. Q2 earnings per share (EPS) were up 73% from last year to $5.16 while free cash flow reached $11 billion.

According to consensus estimates, Meta should grow revenue by 20% this year and maintain a double-digit pace into 2025 and beyond. Earnings should also climb even higher with margins benefiting from the improved AI scale.

Image source: Getty Images.

Exercise caution before buying Meta

There's a lot to like about Meta Platforms proving it can continue to innovate through artificial intelligence. The initiation of a $0.50-per-share quarterly dividend earlier this year solidifies it as a blue-chip stock. That said, it's also worth considering potential weak points in the company's profile that could represent risks down the line.

One area of concern is that the company hasn't been able to materially diversify beyond advertising. Meta does have the Oculus virtual reality headset line along with its recently prototyped Orion augmented reality smart glasses, but these products are not expected to be major growth drivers for the overall business any time soon.

This is in contrast to other "Magnificent Seven" tech stocks that have multiple different operating segments. For example, Alphabet is also a major internet advertising player through search but it has the YouTube video-sharing platform as well, along with the Chrome and Android operating systems.

The question mark is how exposed Meta Platforms would be during an economic downturn in which advertising pulls back. Other tech giants like Microsoft and Amazon could prove to be more resilient.

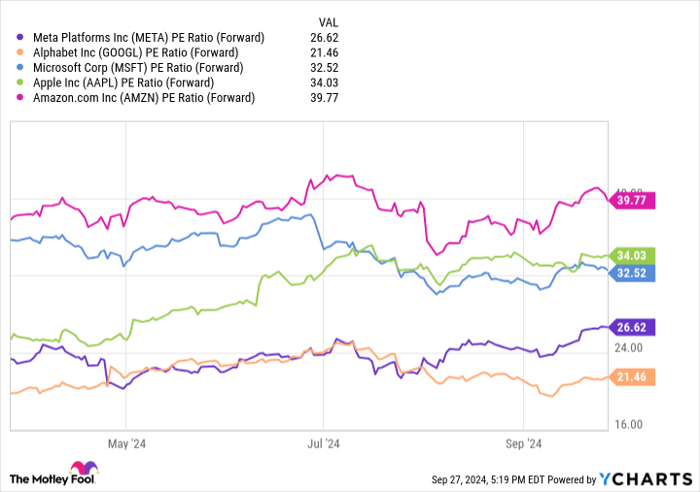

In terms of valuation, shares of Meta Platform are trading at 27 times its full-year consensus EPS as a forward price-to-earnings (P/E) ratio. This level represents a discount compared to Microsoft and Apple, which are above 32, but still a large premium compared to Alphabet, which is closer to 21. It's not clear that Meta is significantly over- or undervalued.

META PE Ratio (Forward) data by YCharts

Decision time for Meta Platforms stock

Meta has everything in place to keep rewarding shareholders over the long run. Still, I believe a hold rating is prudent for now, balancing high expectations following what has already been a breathtaking rally this year. Patient investors may manage to scoop up shares of Meta Platforms at a lower price during the next round of volatility or find more compelling opportunities elsewhere in the market.

Should you invest $1,000 in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $743,952!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 30, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Dan Victor has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles