3 Things That Dollar General Bears Just Don't Get About the Company Right Now

There's no denying that Dollar General's (NYSE: DG) second quarter was just plain bad. Not only did its top- and bottom-line results fall short of analysts' expectations, but its same-store sales growth was anemic, and profits fell year over year. The company dialed back its full-year estimastes as well. The stock was duly punished for all of it.

There are, however, a handful of details that Dollar General bears might also want to consider before deciding to stick with their pessimistic conclusions. Indeed, there are three standout reasons for investors to take a shot on Dollar General stock while it's deeply discounted.

1. Last quarter's sales slump was temporary

The discount retailer's top line did rise by 4.2% during the fiscal second quarter ended Aug. 2, but nearly all of that growth stemmed from new store openings. Same-store sales (revenue from stores open for at least one full year) rose only 0.5%. For comparison, Walmart (NYSE: WMT) reported same-store sales growth of 4.2% for the comparable quarter, while Target's (NYSE: TGT) growth was 2%.

According to Dollar General Chief Executive Officer Todd Vasos, "the softer sales trends are partially attributable to a core customer who feels financially constrained." That view echoed recent comments from executives at a range of consumer companies, and it's not an inaccurate explanation either. Inflation was still above 2% in Q2, the impact of a couple of years of much higher inflation is still being felt, and interest rates were higher than they had been in decades. That's likely why, after months of improvements, the Conference Board's consumer confidence measure dipped in June, and then faltered again in July. In September, the biggest dip in economic confidence came from consumers with annual incomes of less than $50,000 -- Dollar General's primary customer demographic, and a group that can't simply "trade down" in the same way that shoppers with higher incomes can.

However, that short period of time was a perfect storm of monetary misery. Interest rates now are dropping, steered lower by the Federal Reserve's 50-basis-point (0.5%) cut to the benchmark federal funds rate in September. Inflation has continued to moderate, too, and personal spending edged higher in step with August's higher incomes. Gross domestic product ended up rising by 3% in the second quarter, despite the challenging backdrop.

There's still plenty of rebuilding work to do. But last quarter's lethargy arguably marks the absolute low point in Dollar General's target consumers' capacity to spend.

2. (Some) rivals are withering

Dollar General isn't the only discount retailer on the ropes, for the record. Big Lots filed for bankruptcy in early September, and Dollar Tree (NASDAQ: DLTR) announced in June it was reviewing "strategic alternatives" for the Family Dollar store chain it acquired back in 2015. The company has struggled to make Family Dollar all it initially hoped to, so much so that a potential sale or spinoff is now on the table.

This doesn't mean the 1,300-plus Big Lots stores or the 7,761 Family Dollar stores in operation today are going to shutter. The whole reason that Big Lots went into Chapter 11 bankruptcy and Dollar Tree began its strategic review of the Family Dollar unit, in fact, was that their management teams were looking for the best ways to keep as many of those stores open as possible.

Both rival store chains are clearly on the defensive, though, suggesting their management teams may be distracted or unwilling to invest in stores with uncertain futures. Those conditions create opportunities for Dollar General to win some market share.

3. Dollar General stock is underpriced

Now down by 30% from its late-August high and 46% below March's peak, Dollar General stock is just too cheap to pass up.

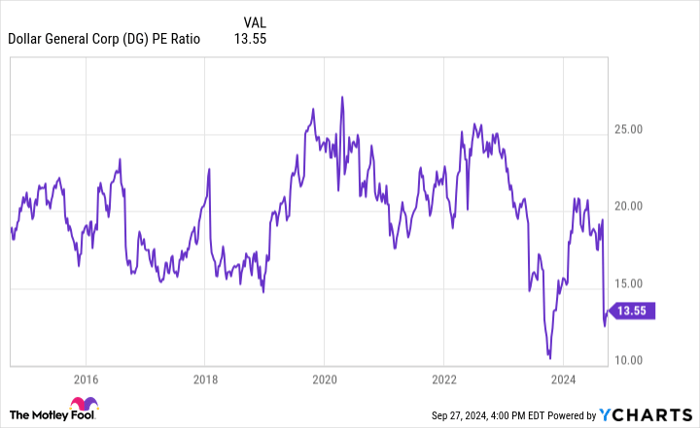

Consider first its simple valuation. Priced at only 13.6 times this year's expected earnings per share of $5.84 and valued at about 15 times next year's projected earnings of $6.32 per share, Dollar General stock is about as cheap as it's been at any point in the past decade, during which the company was growing like crazy.

DG PE Ratio data by YCharts.

Moreover, data compiled by New York University's Stern School of Business indicates the average general merchandise retailer's stock's trailing and forward-looking price/earnings ratios are both currently higher than 20, while food-retailing stocks are priced at just under 17 times their past and projected earnings.

Perhaps even more bullish is the fact that Dollar General shares are underpriced relative to analysts' estimates. Their average 12-month price target stands at $98.92, which is more than 17% higher than the stock's recent price.

True, the analyst community is still generally ho-hum about this company -- most of those who cover it rate the stock a mere hold. There are a handful of buy and even strong buy ratings, though, and there's only one underweight rating. At the very least, this suggests the analyst crowd feels a rebound is possible, even if not guaranteed.

Reward that's worth the risk and the volatility

Obviously, the company still has work to do if it's going to engineer a turnaround, and plenty of risk to be shouldered by shareholders in the meantime. Investors looking for a more reliable, foundational holding for their portfolios should relegate this retailer to their watch lists for now.

If you've got some room in your portfolio for a bit of calculated risk, though, Dollar General's potential reward is now bigger than its plausible downside. Most (if not all) of its potential bad news is already priced into the stock. The biggest worry from here is just the continued volatility that's sure to be in the cards as other investors begin weighing Dollar General's lingering challenges.

Should you invest $1,000 in Dollar General right now?

Before you buy stock in Dollar General, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dollar General wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $743,952!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 30, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Target and Walmart. The Motley Fool has a disclosure policy.

Recommended Articles