3 Reasons to Buy DraftKings Stock Like There's No Tomorrow

This is a tricky time to be an investor. Stock valuations are uncomfortably high, yet the Federal Reserve's recent 0.5 percentage point interest rate cut suggests the U.S. economy needs help. It certainly doesn't seem as though this would be the right time to dig in deep with new positions.

There may be some exceptions to this line of thinking though. Online sports betting company DraftKings (NASDAQ: DKNG) is one of them. Here are the top three reasons -- from least to most important -- that you might want to plow into this ticker right now despite the wobbly macro backdrop.

1. Its shares are discounted

In contrast to many other tickers, DraftKings stock is still down 46% from its 2021 peak. And thanks to a more recent pullback, it's also 16% below the 52-week high it set in March. That suggests this is a tremendous entry opportunity for the particular time frames in question.

Further, despite the stock's recent stumble, the analyst community still believes in it. The majority of the analysts covering DraftKings stock rate it a strong buy, and its average 12-month target price of $49.62 is nearly 25% above its present price.

2. DraftKings isn't just sports gambling anymore

You likely know DraftKings as a fantasy sports platform that entered the sports-wagering industry after the Supreme Court in 2018 stuck down the federal law that had banned sports betting in most states. Sports wagering remains the company's bread-and-butter business. While it now offers online casino games like roulette or blackjack to players in five U.S. states plus the Canadian province of Ontario, its sportsbook is available in 25 states and Ontario.

The non-sports business gives DraftKings a second distinct profit center to work with though, and neither of those businesses necessarily cannibalizes the other. That is to say, sports fans wagering on sporting events aren't necessarily not playing casino games online as a result, and vice versa.

Whatever the current revenue mix is, there's a clear opportunity ahead in the online casino gambling business. The American Gaming Association reports that in July, revenue from that sliver of the U.S. gambling market grew 32.5% year over year, extending a growth trend that has been in place since 2021 when the COVID-19 pandemic was still in full effect.

Indeed, although only seven states currently permit online casino game wagering, it's chipping away at brick-and-mortar casinos' share of the overall business. In July, the online share of U.S. gambling revenue rolled in at 25.9%, versus 19.7% in the same month a year earlier.

3. DraftKings' growth prospects look solid

Finally, DraftKings is growing, and should continue to do so well into the foreseeable future. Last quarter's results paint part of this picture. Revenue was up 26% year over year, prompting the company to raise its full-year revenue guidance. For 2024, DraftKings believes its top line will improve by between 38% and 43%.

Although it has yet to offer revenue guidance for 2025, the company anticipates this year's EBITDA (earnings before interest, taxes, depreciation, and amortization) will roll in between $340 million and $420 million, en route to somewhere between $900 million and $1 billion next year.

No doubt, that sounds like a lofty target. While few would argue that DraftKings isn't moving in the right direction, the online gambling market isn't exactly new, nor is it free of viable competition. That's a lot of sales and earnings growth to be predicting at this stage of the game, so to speak, particularly when DraftKings is already operating in most of the states where it's going to set up shop.

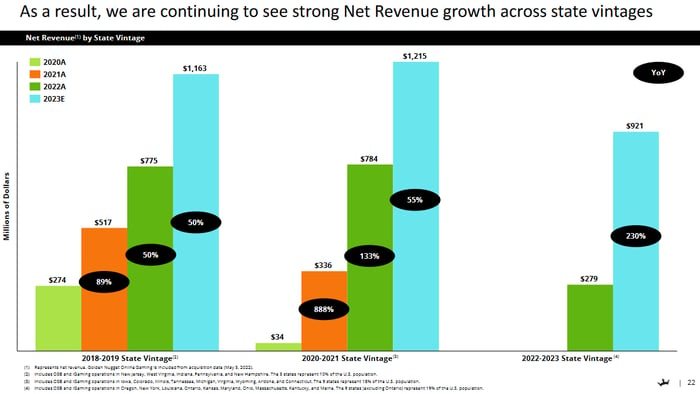

There's an important detail to understand here, however. The longer DraftKings operates within a state, the more revenue that state drives.

Image source: DraftKings November-2023 Investor Day presentation.

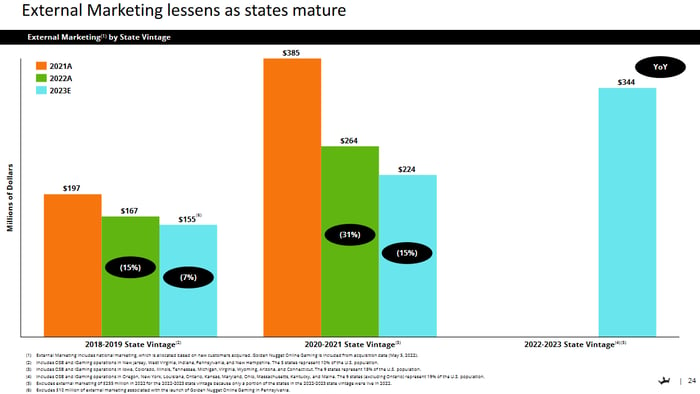

It also gets cheaper to do business in that state, as the company can afford to spend less and less on marketing as more of that state's potential bettors sign up and become loyal customers.

Image source: DraftKings November-2023 Investor Day presentation.

The end result is that its operations in any given state tend to turn profitable in their second or third year. Profit margins continue to widen thereafter, though. Given that DraftKings has only been up and running in several states for two or three years now, a profit explosion beginning next year could be in the cards.

It's not just what's coming in the next year, however, that makes this a prime time to scoop up beaten-down DraftKings shares. Goldman Sachs suggests that online sports betting could grow the overall U.S. sports betting industry from $10 billion now to $45 billion at its peak.

In addition, market research outfit Vixio predicts the online casino gaming industry in the U.S. will grow by 22% to $10.8 billion this year, en route to $13.7 billion by 2027. That puts it on track to surpass the U.K. as the world's single-biggest online casino market.

Not the best first-and-only investment, but still a great growth pick

DraftKings looks like a promising growth prospect, to be sure. Just keep it in perspective. Online sports betting is still relatively new to DraftKings because it's a relatively new business to the United States. This is also a relatively new stock -- the company only went public in April 2020.

Some echoes of the pandemic-driven volatility that prevailed during its early days on the market can still be seen in its chart. As such, owning DraftKings stock isn't for the faint of heart, and it probably shouldn't be one of your core investment holdings.

If the foundational pieces of your portfolio are already in place, though, DraftKings stock brings more upside than risk to the table.

Should you invest $1,000 in DraftKings right now?

Before you buy stock in DraftKings, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DraftKings wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $760,130!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 23, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group. The Motley Fool has a disclosure policy.

Recommended Articles