Better Artificial Intelligence (AI) Stock: Nvidia vs. AMD

The semiconductor industry has received a big lift from the growing adoption of artificial intelligence (AI) technology in multiple industries ranging from data centers to smartphones to personal computers, which explains why the PHLX Semiconductor Sector index has clocked healthy gains of 20% so far in 2024.

Nvidia (NASDAQ: NVDA) has been one of the biggest beneficiaries of the fast-growing demand for AI chips. The stock has shot up 135% so far in 2024 as of this writing, and that's justified, as Nvidia is the leading player in the market for AI graphics processing units (GPUs), with an estimated market share of 94% at the end of 2023.

This terrific market share explains why Nvidia's rival Advanced Micro Devices (NASDAQ: AMD) hasn't received enough love on Wall Street. Shares of AMD are up just 6% this year, and that's not surprising, as its revenue and earnings growth have been nowhere near Nvidia's. Does this mean Nvidia will remain a better AI stock than AMD, or will the latter's gradually improving AI credentials spark a rally in its stock price? Let's find out.

The case for Nvidia

The biggest reason to buy Nvidia over AMD is the impressive moat that the former enjoys in AI GPUs. We have already seen that Nvidia is the dominant company in the AI chip market, with a phenomenal market share. This explains why the chipmaker's revenue from the data center business stood at a record $26.3 billion last quarter, up an impressive 154% from the same period last year.

AMD, on the other hand, reported data center revenue of $2.8 billion, up 115% year over year.

The third suitor in the AI chip market, Intel, reported data center and AI (DCAI) revenue of $3 billion last quarter, a decline of 3% from the same period last year. So, the three chipmakers together sold just over $32 billion worth of data center chips last quarter, and Nvidia enjoyed the lion's share of this market with a share of over 80%.

What's more, Nvidia's data center revenue grew at a much faster pace than that of its rivals, which clearly means that the demand for its chips remains stronger compared to competitors. In fact, customers are still lining up to buy Nvidia's Hopper AI GPUs that are set to be replaced by the upcoming Blackwell chips. Meanwhile, Nvidia estimates that the demand for its Blackwell processors will exceed demand going into 2025.

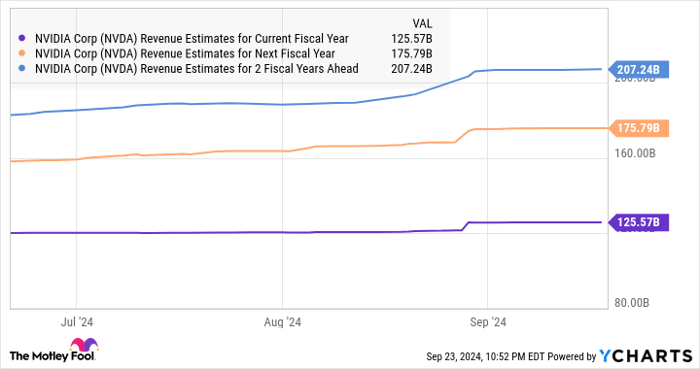

All this indicates that Nvidia's AI chip demand is set to remain solid both in the short and long run. That's the reason why the company's data center business is expected to generate a whopping $200 billion in revenue in 2025, according to KeyBanc analyst John Vinh. That forecast is higher than the $140 billion consensus estimate for Nvidia's data center revenue in 2025 (which will coincide with its fiscal 2026).

Nvidia has generated almost $49 billion in data center sales in the first half of the current fiscal year. That puts the company on track to clock close to $100 billion in data center revenue in fiscal 2025. So, KeyBanc is expecting the company to double its data center sales in the next fiscal year, and that possibility cannot be ruled out, as the arrival of Nvidia's Blackwell chips is expected to supercharge its sales growth.

The company will start the production of the Blackwell processors in the fourth quarter of the current fiscal year, generating "several billion dollars in Blackwell revenue." Analysts expect these new chips to drive serious revenue growth for the company next year thanks to a robust demand environment. Timothy Arcuri of UBS estimates that Nvidia's revenue in calendar 2025 (which will coincide with fiscal 2026) could hit $204 billion. That's well ahead of consensus expectations.

NVDA Revenue Estimates for Current Fiscal Year data by YCharts

As such, Nvidia is likely to remain a top AI stock going forward, delivering eye-popping revenue and earnings growth.

The case for AMD

By now, it is evident that AMD has failed to make a dent in the AI data center GPU market. While we are talking about Nvidia's data center revenue exceeding the $100 billion mark this year, AMD management is expecting its data center GPU revenue to hit at least $4.5 billion in 2024. So, AMD's data center GPU business is miles away from getting to Nvidia's scale.

But at the same time, investors should note that AI could eventually become a key growth driver for AMD, as it is well-placed to benefit from the adoption of this technology in multiple areas beyond data center GPUs. For instance, AMD's client segment revenue increased an impressive 49% year over year in Q2 to $1.5 billion, driven by the healthy demand for the company's Zen 5 Ryzen processors that have been developed to power AI applications on PCs (personal computers).

These new processors have a dedicated AI chip on them to help PCs and notebooks run AI workloads locally. Counterpoint Research estimates that three out of four laptops shipped in 2027 are going to be AI-capable. On the other hand, market research firm Canalys estimates that the AI PC market could clock an annual growth rate of 44% through 2028.

Given that AMD has been gaining ground in the client CPU (central processing unit) market and controls just over a third of this space, it is well-placed to make the most of this fast-growing opportunity on offer. Meanwhile, AMD's data center business can also get a boost thanks to the growing demand for general-purpose server CPUs required in the development of small AI models as well as for inferencing purposes.

AMD's peer Intel estimates that general compute chips such as server CPUs could generate $24 billion in annual revenue in 2027. So, AMD still has a lot of room for growth in the data center business thanks to AI. On the one hand, it could keep gaining more share of the server CPU market from Intel, while on the other hand, it could witness growth in the data center GPU market as well even if it plays second fiddle to Nvidia.

The verdict

The good news for AMD investors is that the company's growth is forecasted to accelerate in the coming years, but Nvidia is expected to grow at a faster pace. Nvidia's earnings are forecast to increase at a compound annual growth rate of 52% for the next five years, higher than the 33% growth rate that AMD is forecast to deliver over the same period. Even better, Nvidia is cheaper than AMD.

NVDA PE Ratio data by YCharts

So, investors looking to buy an AI stock to make the most of the AI chip market's growth can still consider buying Nvidia even after the impressive gains that it has delivered in 2024, as its dominant position in this space could lead to years of robust growth.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $756,882!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 23, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Intel and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.

Recommended Articles