US Dollar softens as Powell signals no urgency to change rates

- The US Dollar Index trades with losses for the second consecutive session on Tuesday, hovering above 108.00 without clear direction.

- Federal Reserve Chair Jerome Powell signals no urgency to adjust monetary policy, keeping markets in a cautious stance.

- The CME FedWatch Tool shows that markets are pricing in a hold at March’s meeting.

The US Dollar Index (DXY), which measures the value of the US Dollar against a basket of currencies, remains down for the second day after hearing from the head of the US central bank. Federal Reserve (Fed) Chair Jerome Powell's testimony to Congress emphasized a data-dependent approach, indicating that rates will stay steady unless inflation or labor conditions shift. This notion reduced the chance of a rate cut at the March meeting.

Daily digest market movers: US Dollar loses traction after Powell’s cautious testimony

- The main market mover on Tuesday was Powell’s testimony before Congress, which wasn’t as hawkish as expected and might have weakened the USD.

- The Fed Chair confirms no immediate changes to policy, keeping the 2% core inflation target intact.

- Powell acknowledges inflation is still somewhat elevated but emphasizes patience in adjusting monetary policy.

- He also highlighted concerns over long-term rates, stating they are driven by fiscal deficit and inflation expectations.

- Equities remain mostly flat with investors digesting Powell’s neutral stance on interest rates and trade.

- The CME FedWatch Tool indicates a 90% probability that the Fed will maintain rates at 4.25%-4.50% in March.

- Elsewhere, the US 10-year yield climbs toward 4.55%, extending its rebound from a year-to-date low of 4.40% reached last week.

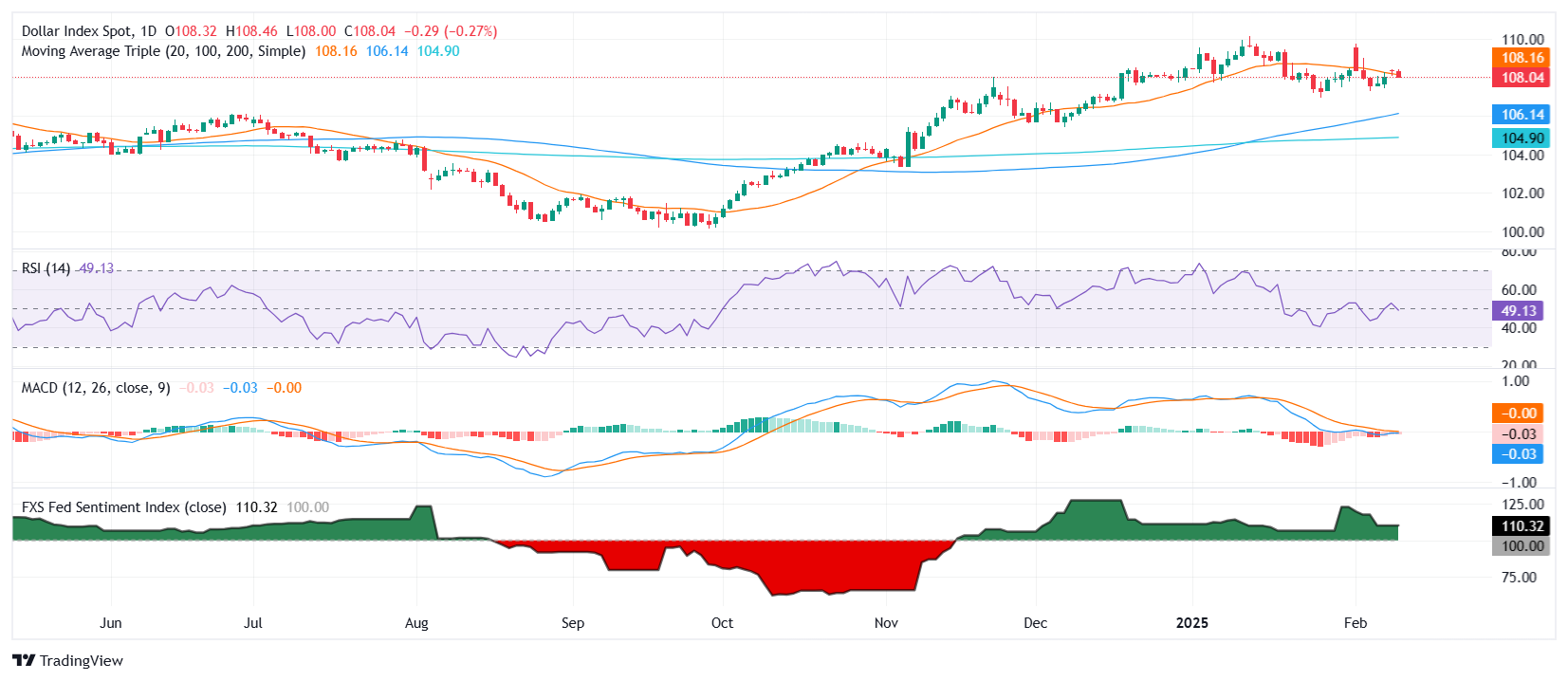

- In fact the Fed's sentiment index on the daily chart signlas that the bank's hawkish tone has eased somewhat.

DXY technical outlook: Dollar weakens as key support levels come into play

The US Dollar Index struggles to maintain momentum, slipping below the 20-day Simple Moving Average (SMA) around 108.50. The Relative Strength Index (RSI) is drifting lower, approaching bearish territory below 50, signaling declining momentum. The Moving Average Convergence Divergence (MACD) histogram is turning negative, indicating growing bearish traction.

If selling pressure intensifies, immediate support lies at 108.00, followed by the psychological level of 107.50. On the upside, resistance is seen at 108.80 and the 109.20 zone, which could cap short-term rebounds.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Recommended Articles