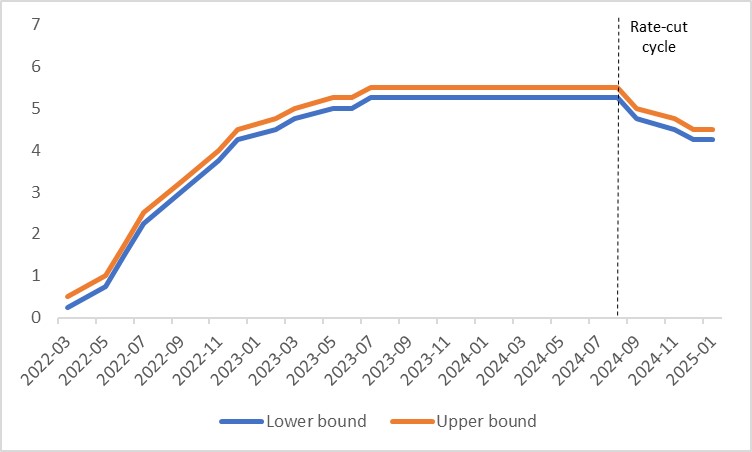

On 20 March 2025, the Federal Reserve (Fed) will announce its interest rate decision for March. The market widely anticipates that the central bank will keep its policy rate unchanged, maintaining it within the range of 4.25%–4.5% (Figure 1). We align with this consensus outlook. This article analyses the Fed’s monetary policy through three lenses: high-frequency economic data, the labour market and inflation.

Figure 1: Fed policy rate (%)

Source: Refinitiv, Tradingkey.com

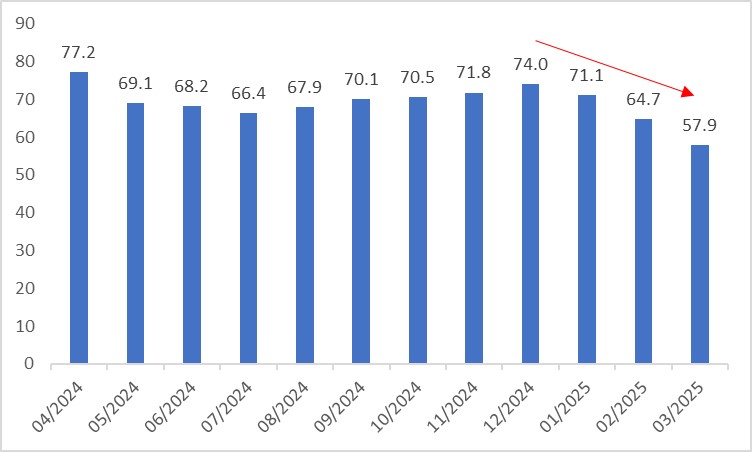

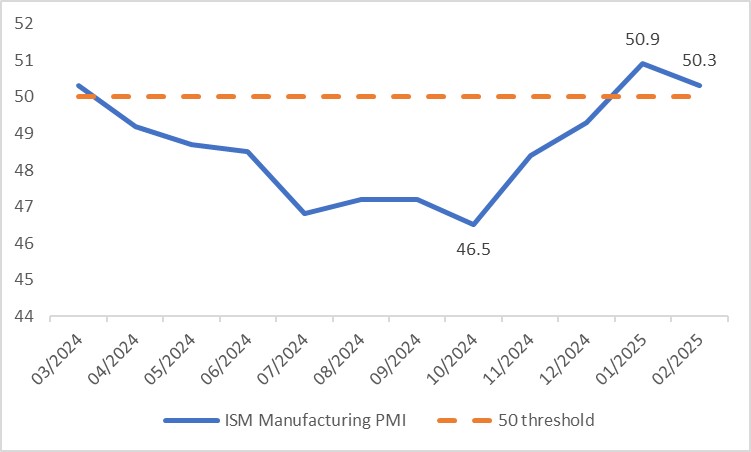

High-frequency data reveals that U.S. economic resilience is gradually fading, with clear signs of a slowdown. On the spending side, the Michigan Consumer Sentiment Index has declined steadily from a peak of 74 in December last year to 57.9 in March (Figure 2). Waning consumer confidence has dampened spending intentions, with the latest figures showing retail sales growth slowing from 4.2% year-over-year in January to 3.1% in February. On the production side, while the ISM Manufacturing PMI rebounded from a low in October last year and crossed the 50 threshold in January, it edged lower again in February (Figure 3).

Figure 2: U.S. Michigan Consumer Sentiment Index

Source: Refinitiv, Tradingkey.com

Figure 3: U.S. ISM Manufacturing PMI

Source: Refinitiv, Tradingkey.com

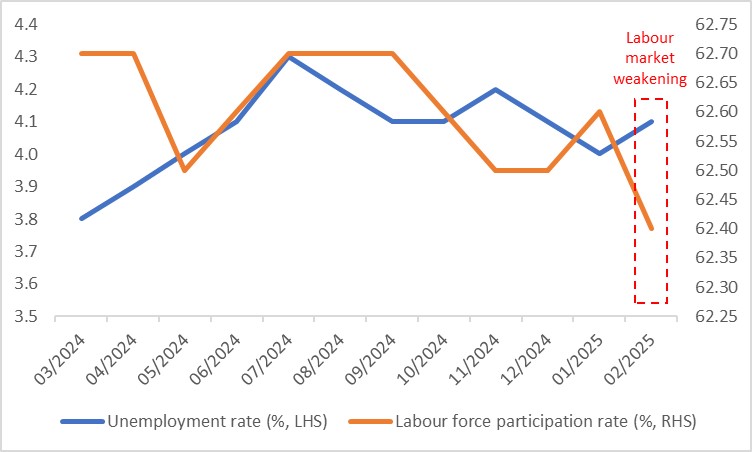

In tandem, the U.S. labour market is showing signs of weakness. After a steady decline in the unemployment rate throughout the second half of last year, the metric began to tick up in February. This contributed to a sharp drop in the labour force participation rate, which fell to 62.4% in February—a 12-month low (Figure 4).

Figure 4: U.S. labour market

Source: Refinitiv, Tradingkey.com

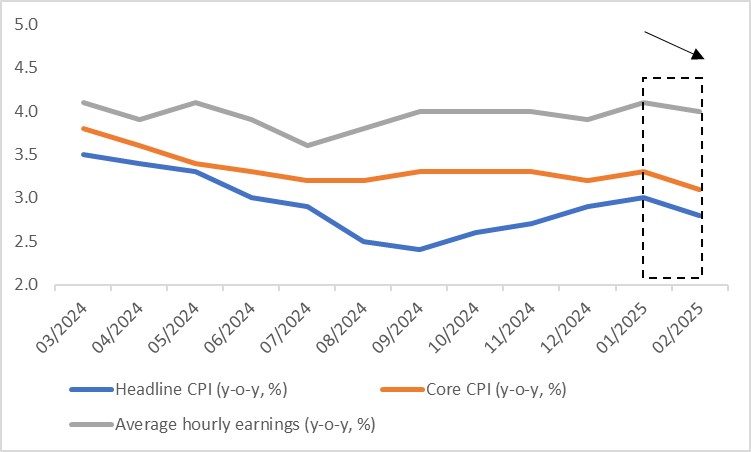

On the inflation front, the latest data suggests that inflation has reached a turning point, breaking from its prior upward trend. Compared to January, February’s Headline CPI and Core CPI each dropped by 0.2 percentage points, reaching 2.8% and 3.1%, respectively. Looking ahead, we expect inflation to gradually ease toward the Fed’s 2% target over the coming quarters. Additionally, a decline in average hourly earnings could further alleviate inflationary pressures (Figure 5).

Figure 5: U.S. inflation and earnings

Source: Refinitiv, Tradingkey.com

Given the economic slowdown, softening labour market and declining inflation, we anticipate the Fed will resume its rate-cutting cycle within the next few months. However, with uncertainties surrounding Trump administration policies and the risk of a U.S. recession remaining low, a rate cut in March appears unlikely.

Since the market has already priced in the Fed’s decision to hold rates steady on 20 March, the announcement itself is unlikely to significantly move financial markets. That said, Fed Chair Powell’s accompanying remarks will be a critical factor to watch. A hawkish tone from Powell could boost the U.S. dollar index and Treasury yields while weighing on equities. Conversely, a dovish stance could have the opposite effect.

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.