Here’s What to Watch With February 2025’s CPI Inflation Report

- Bitcoin Drops to $70,000. U.S. Government Refuses to Bail Out Market, End of Bull Market or Golden Pit?

- Gold rallies further beyond $5,050 amid flight to safety, dovish Fed expectations

- Bitcoin Bottom Debate: $70,000 or $50,000?

- A Crash After a Surge: Why Silver Lost 40% in a Week?

- Bitcoin Slips Below 75,000 Mark. Will Strategy Change Its Mind and Sell?

- Bitcoin Rout. Bridgewater Founder Dalio Publicly Backs Gold.

TradingKey - It’s been a rough few weeks for stock markets at technology stocks, in particular, have been hard hit by the uncertainty surrounding the impact of tariffs on the US economy.

Of course, the flurry of tariffs that were announced by President Trump have raised fears of inflation rearing its ugly head again in the US.

Last week, the S&P 500 Index dropped 3.1% while the tech-heavy Nasdaq Composite Index declined by 3.5%. While the Friday non-farm payrolls report was relatively solid – with 151,000 jobs added in the month of February – the sentiment among investors remains downbeat.

That’s leading to questions being raised about whether the US Federal Reserve (Fed) will be able to cut interest rates as much as it wants to this year, given the prospect of potentially higher inflation being sparked by all these tariff announcements.

One of the highlights this week, which should give investors some idea of what the overall inflation picture is like, is the February Consumer Price Index (CPI) inflation report for the US economy.

Set to be released on Wednesday (12 March) before the market opens in the US, it could set the short-term direction for investors in the back half of the week. With that in mind, here’s what investors should know heading into the latest CPI report.

CPI expectations: Where are they?

The Consumer Price Index (CPI) has accelerated in recent months and that has added fuel to the uncertainty fire that is burning. The CPI measures the cost of a broad basket of goods and services across the US economy.

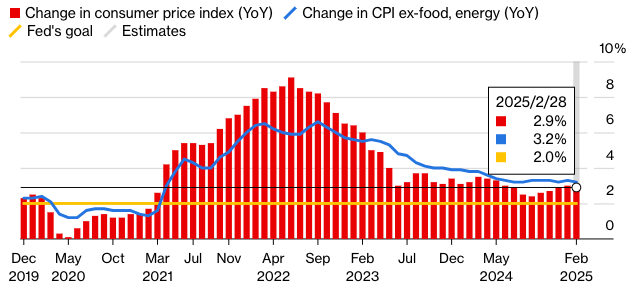

In terms of context, the latest CPI report for January 2025 saw prices rise at a seasonally-adjusted 0.5% month-on-month. That translated into a 3% year-on-year rise in prices and came in ahead of estimates for the reading.

Excluding volatile food and energy prices, the so-called “core CPI” rose 0.4% on the month and put the 12-month/year-on-year inflation rate at 3.3%. Heading into this CPI print, all eyes will be on whether prices appear like they’re on an upward trend or whether it could be the start of a reversal.

Expectations for February’s CPI reading are relatively similar to what was expected for January; headline CPI is expected to rise 2.9% on an annualised basis while core CPI is expected to see a 3.2% annual increase. Of course, these two figures are much higher than the Fed’s ideal inflation target of 2%.

US inflation staying stubbornly around 3%

Sources: Bureau of Labor Statistics, Bloomberg

The good news? The Personal Consumption Expenditures (PCE) Price Index, one of the key inflation readings that the Fed looks at, came in with a 0.3% month-on-month increase for January 2025 while it increased by 2.5% on an annualised basis.

This was slightly down from the 2.6% annualised pace in PCE inflation for December 2024. However, this CPI report on Wednesday will be a leading indicator for many investors for the traditional month-end PCE Index release.

How should investors be thinking about positioning?

Heading into this data release, investors should be aware of the Fed’s Federal Open Market Committee (FOMC) meeting on 18-19 March. It’s nearly certain that the Fed will keep rates where they are but the CPI report on Wednesday will be the last big data point before they gather just over a week later.

It will certainly give the Fed’s board members food for thought as they process the data to determine when they might be able to cut rates. Expect them to factor in the CPI data into any comments they will have in the press conference immediately after the FOMC.

For investors, it looks like the trading momentum right now is to the downside and the S&P 500 Index and Nasdaq Composite Index could easily fall further if the CPI reading on Wednesday comes in “hot” or above expectations. The market is looking for anything even slightly negative as a reason to sell off and that market “mentality” right now is something investors should all be aware of.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.