- US President Donald Trump says Iran talks to begin Monday after canceling attack

- Gold Price Forecast: Can Gold Still Rise Above $4,300 Ahead of July Non-Farm Payrolls?

- Gold rallies to two-week high as USD softens on Iran deal hopes, receding Fed hike bets

- Australian Dollar remains calm following Trade Balance data

- WTI holds firm near $77.50 as escalating Middle East tensions threaten oil supply routes

- WTI trades with positive bias below mid-$79.00s on Iran uncertainty, supply concerns

By Jason Tang, Petar Petrov, Viga Liu

In 2025, with Trump returning to office, the US dollar is likely to remain strong?

USD Index

Similar to US Treasury yields, we expect the USD Index to rise in the short term, driven by the dominance of Trump Trade in the market. This upward trend is likely to persist through the first quarter of 2025. In the medium term, however, the focus will shift to the Fed’s interest rate cut cycle, leading to a gradual decline in the USD Index. However, could the dollar remain stronger than expected in 2025?

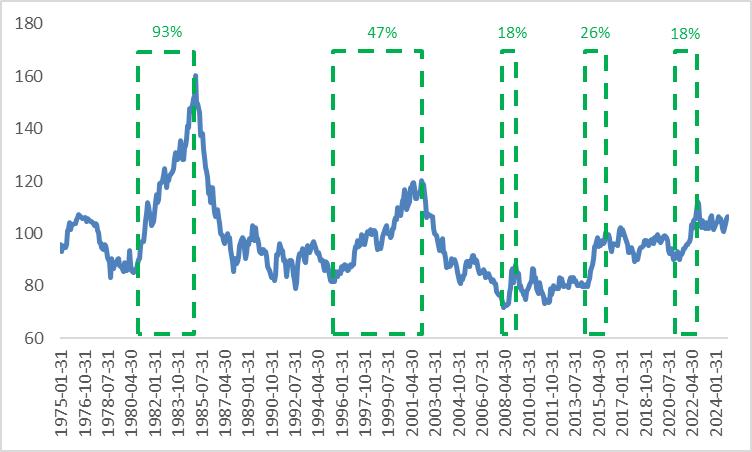

To evaluate whether the USD Index could stay elevated throughout the year, we examine the historical patterns of dollar appreciation. Since the collapse of the Bretton Woods system and the creation of the USD Index, the dollar has experienced five major appreciation cycles—two long and three short (Figure 5.1).

By analysing these cycles, we identify five key conditions for the US dollar to sustain a medium- to long-term upward trend: 1) Rising inflation levels; 2) A Fed interest rate hike cycle; 3) Divergence in the US and European monetary policies; 4) Exceptional strength in the US economy; 5) A global economic crisis.

At present, none of these conditions are being met. Inflation remains under control, the Fed is in a rate-cutting phase and US monetary policy aligns with other major economies. Additionally, while the US economy shows resilience, it is not experiencing exceptional outperformance. The global economic environment also lacks the kind of crisis that typically drives a prolonged dollar rally.

Given these factors, the likelihood of the USD Index maintaining a sustained upward trend throughout 2025 is low.

Figure 5.1: US dollar upward cycles

Source: Refinitiv, Tradingkey.com

EUR/USD

After the US election, the euro has lagged behind other major currencies. Looking ahead to 2025, the euro’s performance against the US dollar is expected to be influenced by three main factors: 1) Divergence in economic growth between the US and the eurozone; 2) The different pace of inflation declines in the two economies; 3) Trump’s policies.

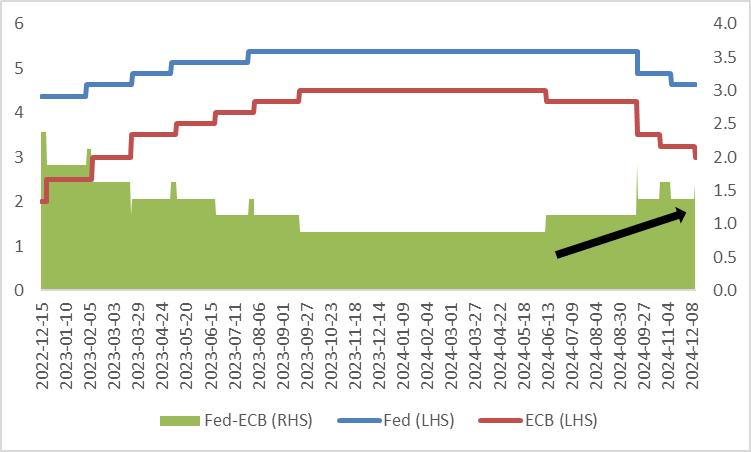

Regarding the first two factors, in 2025, the European Central Bank (ECB) will likely focus on addressing weak economic growth, while the Fed will concentrate on alleviating pressures from reflation. As a result, we expect the ECB to adopt a more aggressive rate-cutting strategy compared to the Fed, which could widen the policy interest rate gap between the US and Europe (Figure 5.2).

In addition to the monetary policy divergence, political unrest in Germany and France could further constrain fiscal spending, adding continued downward pressure on the euro against the dollar, particularly in the first quarter of 2025.

In terms of Trump’s impact on the euro, as discussed in the Macroeconomics section, Trump’s high tariffs and efforts to force the EU to decouple from China could negatively impact eurozone exports, which is generally bearish for the euro.

However, starting in the second quarter of 2025, we expect a decline in the USD Index. This could lead the euro to enter a period of choppy trading against the dollar as market dynamics evolve.

Figure 5.2: Fed vs. ECB policy rates (%)

Source: Refinitiv, Tradingkey.com

USD/JPY

As noted earlier, the Japanese bond market experienced a prolonged bull run from 1990 to 2019, with three notable periods of yield rebounds. Similar to other developed countries, Japanese bond yields and the yen tend to exhibit a degree of correlation. During these three periods of yield recovery, the yen also strengthened (Figure 5.3).

After 2021, however, Japanese bond yields and the yen began to diverge, largely due to the appreciation of the US dollar.

Looking ahead, we expect the dollar to enter a bear market starting in the second quarter of 2025. This, coupled with monetary policy divergence between the Fed and the Bank of Japan (BoJ), as well as the upward trajectory of Japanese bond yields, supports our view that the yen will enter a bull market in 2025.

Figure 5.3: 10Y Japanese government bond yield vs. USD/JPY

Source: Refinitiv, Tradingkey.com

Risks

If geopolitical tensions, escalating trade protectionism and intensifying reflationary pressures exceed expectations in 2025, the global macroeconomic environment and financial markets could face heightened risks. These challenges may lead to declines in global stock markets, rising bond yields and sustained strength in the USD Index.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.