Executive Summary

TradingKey - At the front end of the NZD/USD currency pair, the New Zealand Dollar (NZD) is expected to weaken against non-USD currencies due to the Reserve Bank of New Zealand’s (RBNZ) ongoing rate cuts, the central bank’s recent dovish remarks and the impact of Trump’s tariff policies. At the back end, the USD index is projected to decline in the short term (0-3 months) due to a slowing US economy and the Federal Reserve’s resumption of rate cuts. Over the medium term (3-12 months), however, the USD’s safe-haven appeal may strengthen as US economic weakness spreads globally and Europe’s recovery falters. Consequently, with both ends of the pair weakening in the short term, we anticipate NZD/USD will trade in a range without a clear trend. In the medium term, a rising USD index is likely to push the pair lower.

Source: Refinitiv, Tradingkey.com

Source: Tradingkey.com

* Investors can directly or indirectly invest in the foreign exchange market, bond market and stock market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Macroeconomics

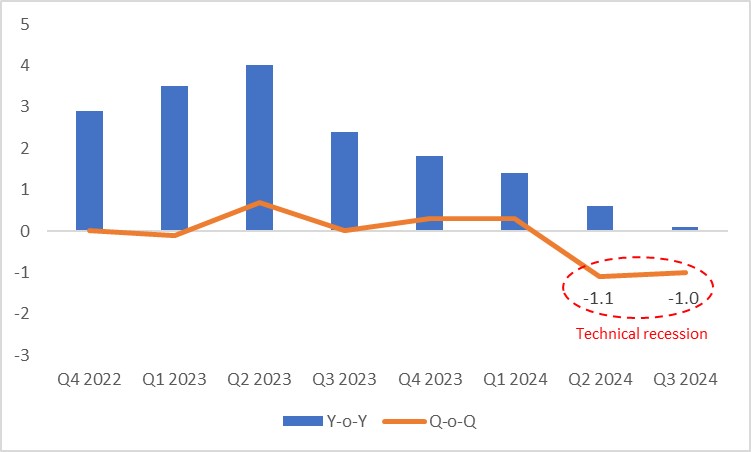

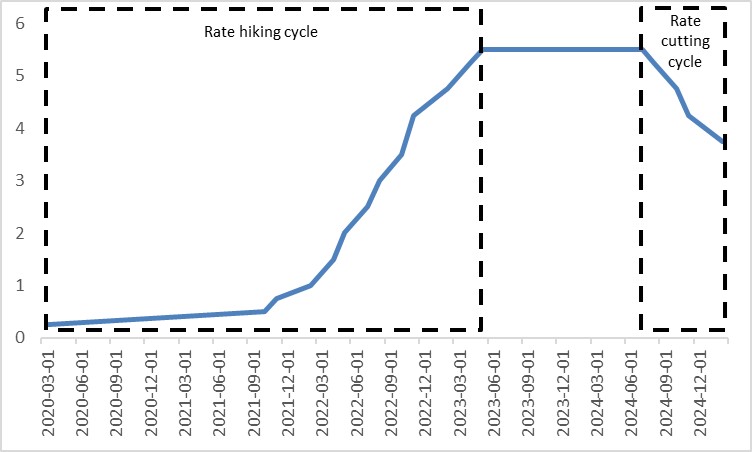

In recent years, the RBNZ has played a textbook role. The pandemic triggered high inflation, prompting the RBNZ to aggressively hike its policy rate from late 2021 to mid-2023. While inflation was tamed, the economy slipped into a recession in 2024 (Figure 1.1). Against this backdrop, the RBNZ initiated a rate-cutting cycle in August 2024 (Figure 1.2).

Figure 1.1: New Zealand real GDP growth (%)

Source: Refinitiv, Tradingkey.com

Figure 1.2: RBNZ policy rate (%)

Source: Refinitiv, Tradingkey.com

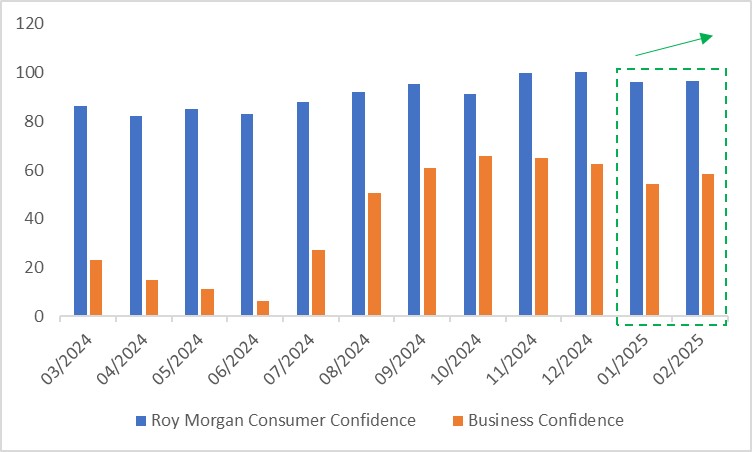

Under this looser monetary policy, signs of economic recovery have emerged. High-frequency data shows February’s Roy Morgan Consumer Confidence rising to 96.6, slightly up from January’s 96. Business Confidence in New Zealand surged to 58.4 in February, well above January’s 54.4 (Figure 1.3).

Figure 1.3: New Zealand consumer and business confidence

Source: Refinitiv, Tradingkey.com

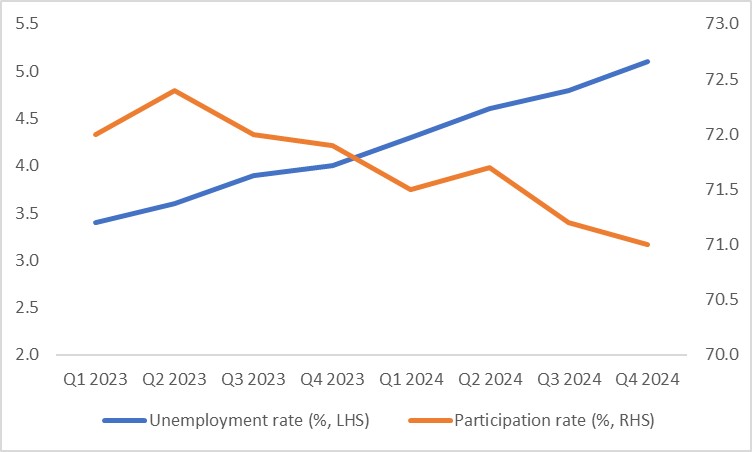

However, the labour market remains weak, signalling persistent economic downside risks. Fourth-quarter 2024 data, released in February, revealed an unemployment rate of 5.1%—up 1.9 percentage points from its cycle low and just 0.1 points shy of the COVID-19 peak. This has driven the labour force participation rate lower for several consecutive quarters (Figure 1.4).

Figure 1.4: New Zealand labour market

Source: Refinitiv, Tradingkey.com

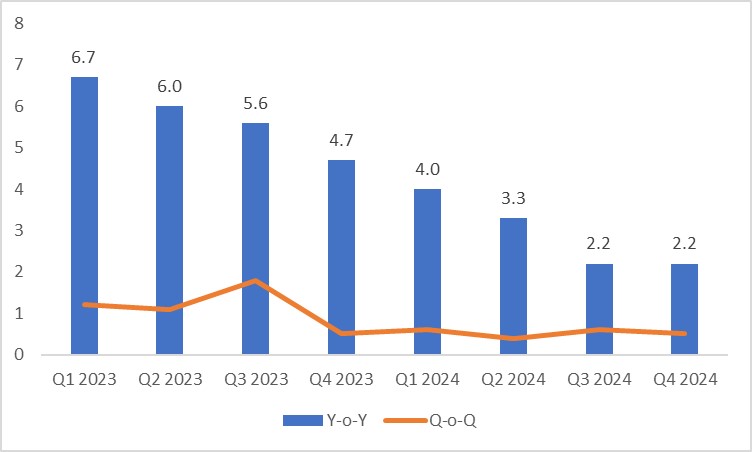

On inflation, New Zealand’s CPI has gradually declined amid the 2024 recession and labour market softness, falling within the RBNZ’s 1%-3% target range since Q3 2024 (Figure 1.5). With inflation easing and economic risks lingering, the RBNZ cut rates by 50 basis points on 19 February 2025, bringing the policy rate to 3.75%—a cumulative 175-basis-point reduction since August 2024. Looking ahead, while recovery signs may temper the pace of cuts, further easing remains ongoing.

Figure 1.5: New Zealand CPI (%)

Source: Refinitiv, Tradingkey.com

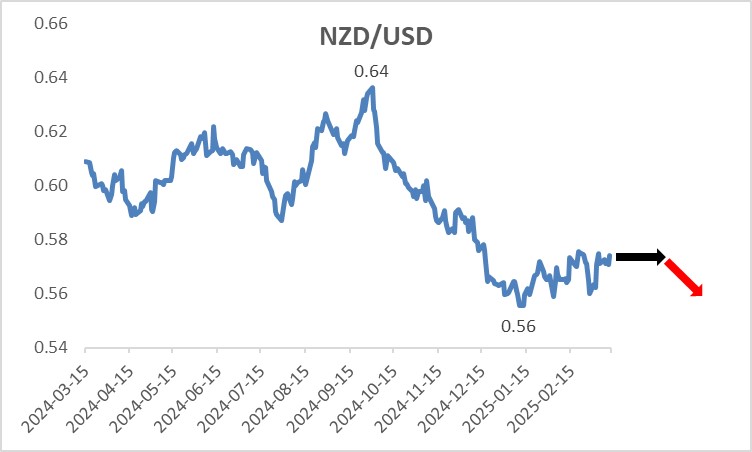

2. Exchange Rate (NZD/USD)

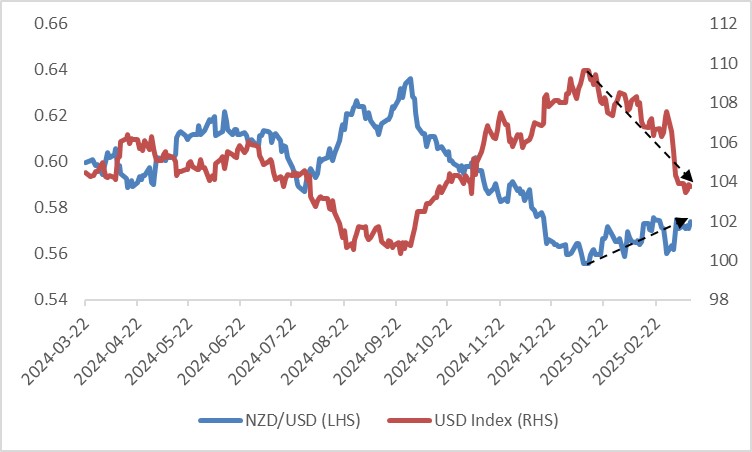

Risk-off sentiment tied to tariff-related news triggered a late-February drop in the NZD. Since early March, however, NZD/USD has strengthened as early signs of US economic weakness weighed on the USD index.

Looking forward, the NZD faces multiple headwinds:

· RBNZ Policy: The RBNZ has signalled a continued easing path. Ongoing rate cuts will widen the policy rate differential with the Fed, pressuring the NZD downward.

· Dovish Rhetoric: The central bank described the NZD’s decline as a “welcome boost”, suggesting the RBNZ may tolerate a weaker currency to support exports and curb trade deficits.

· Trade War Impact: Trump’s tariffs and a US-led trade war pose challenges for New Zealand, given its export reliance and current account deficit. Even without direct tariffs, regional economic ties and indirect spillovers will weigh heavily on the NZD.

On the USD side, a slowing US economy and Fed rate cuts will likely keep the USD index soft in the short term (0-3 months). Over the medium term (3-12 months), however, global contagion from US weakness and Europe’s stalled recovery could bolster the USD’s safe-haven status. (See our report on [In-Depth Analysis] Trump Policies: Market Overreacted, Remain Bullish on Stocks, published on 17 March 2025).

With both NZD and USD weakening short-term, NZD/USD is poised for range-bound trading without a clear direction. In the medium term, a stronger USD index will likely drive the pair lower (Figure 2).

Figure 2: NZD/USD and USD Index

Source: Refinitiv, Tradingkey.com

3. Bonds

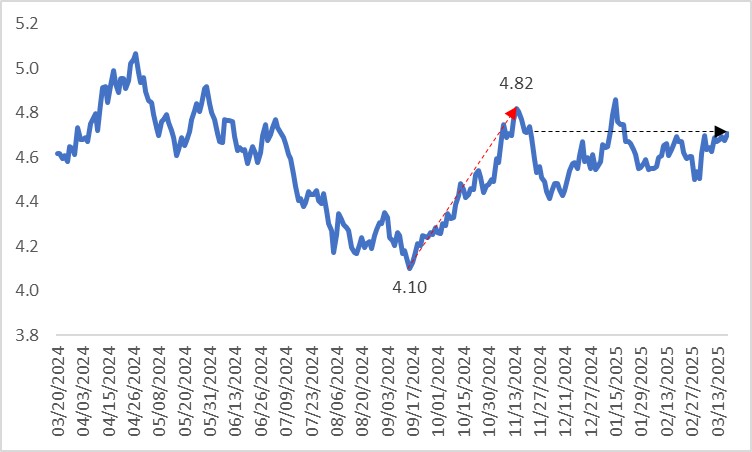

New Zealand government bond yields rose steadily from September 2024, peaking at 4.82% in November, before stabilizing in a range. This was driven by internal and external factors. Domestically, inflation eased from September but remained above expectations, pushing yields higher. Since late 2024, however, the RBNZ’s decisive rate cuts and inflation falling within the target range have capped further increases (Figure 3.1).

Figure 3.1: New Zealand 10Y government bond yields (%)

Source: Refinitiv, Tradingkey.com

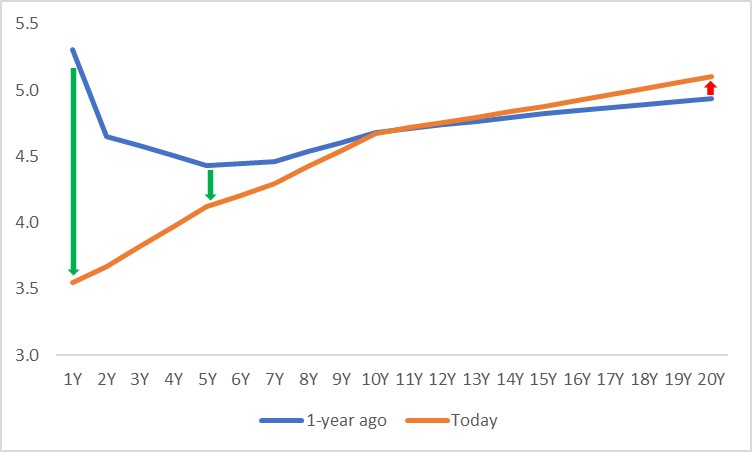

Going forward, continued RBNZ easing is expected to pull the yield curve lower, further pressuring the NZD against non-USD currencies. Short-term yields, more sensitive to policy rates, are likely to decline more sharply than long-term yields (Figure 3.2).

Figure 3.2: New Zealand government bond yield curve (%)

Source: Refinitiv, Tradingkey.com

4. Stocks

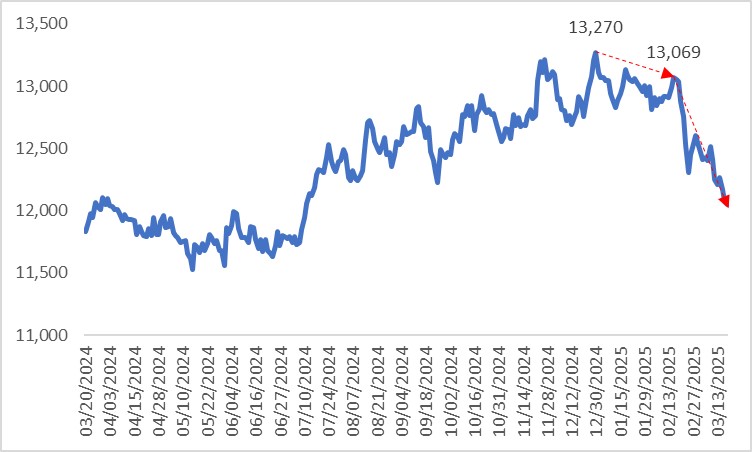

The New Zealand stock market peaked in late December 2024 before trending lower, with a sharp decline starting in mid-February 2025 (Figure 4). This reflects a dim economic outlook and labour market weakness. Looking ahead, as the economy shows tentative recovery signs and the RBNZ continues easing, the stock market is expected to stabilize and trade within a range, halting its downward slide.

Figure 4: NZX 50

Source: Refinitiv, Tradingkey.com

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.