Tempus AI: Architecting the Next Era of Intelligent Diagnostics

- Tempus AI generated $693.4M in 2024 revenue (+30.4% YoY) and projects 2025 revenue of $1.24B (+79% growth).

- Genomics segment brought in $451.7M in 2024, supported by $4,500 Medicare reimbursement for its FDA-approved xT CDx test.

- Data & Services revenue surged 43.2% to $241.6M with 80.3% gross margins and 140% net revenue retention in 2024.

- Valued at $7.5B, Tempus trades at ~6.05x 2025E revenue, with a near-term price target of $45–$48 based on growth metrics.

TradingKey - Tempus AI (TEM) is leading a tectonic transformation of how the healthcare system utilizes diagnostics, not simply ordering tests, but correlating them with patient-level data and incorporating AI to make all insight tailored to each individual. With this ambitious vision, Tempus is constructing the building blocks of a new paradigm for diagnostics, what it refers to as “Intelligent Diagnostics.” It is not a buzz term. It is a deeply strategic reworking of clinical testing, where each diagnosis is as unique not only to the disease, but to the entire clinical journey of a patient.

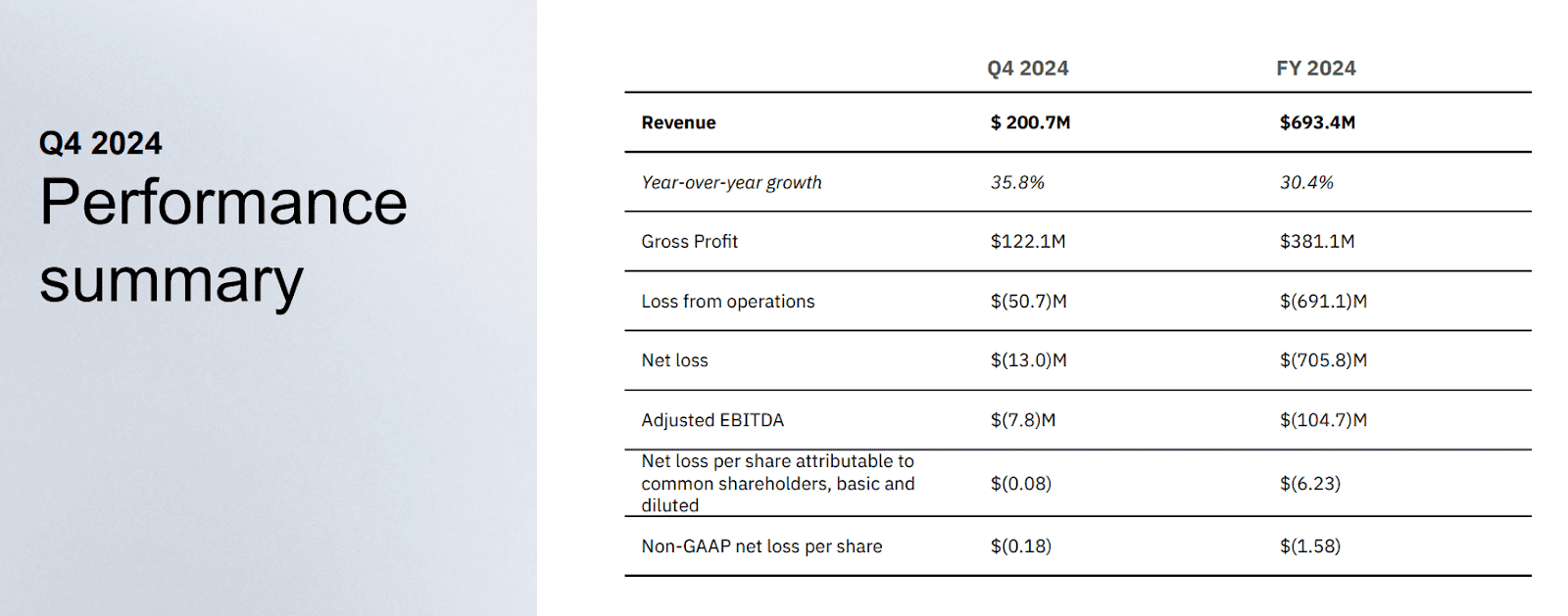

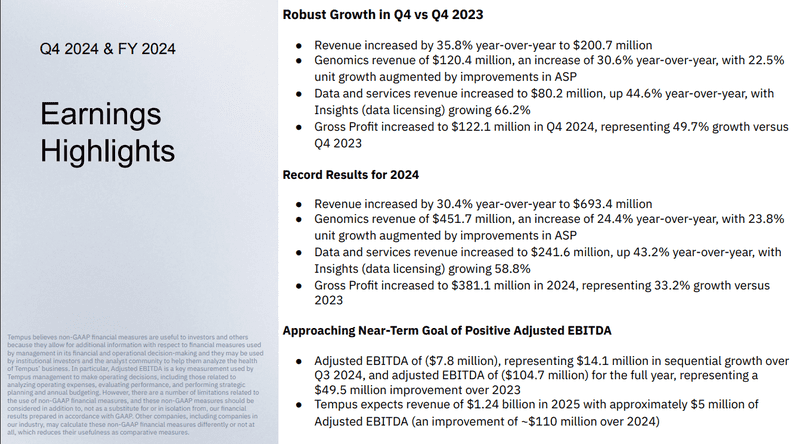

After a year of strong expansion and margin growth, Tempus is now at meaningful scale. Full-year 2024 revenue totaled $693.4 million (+30.4% YoY), with Q4 expansion at 35.8%. With help from timely acquisition of Ambry Genetics, and an expected 79% growth in 2025 revenue to $1.24 billion, Tempus is moving from growth story to operating leverage story. With adjusted EBITDA expected to turn positive by 2025, investors are catching glimpses of the company's long-term vision: a full-stack precision medicine platform with high-margin software, scalable data licensing, and strong payor tailwinds.

Source: Q4 Deck

Business Model Summary: Diagnostics, Data, and AI as Reenforcing Flywheels

Tempus' moat is created at the intersection of three business segments that complement one another over time: Genomics, Data & Services, and AI Applications.

Genomics business is the growth driver, with $451.7 million generated by NGS tests for oncology, liquid biopsies, and inherited disease screening in 2024. Volume expanded 23.8 percent, and price (ASP) was rising as well, as a result of supportive reimbursement, including $4,500 for its FDA-approved xT CDx test under Medicare. While scale separates Tempus, it's integration that differentiates. Each test contributes to an expanding multimodal dataset that bridges molecular, imaging, and phenotypic data, gathered through more than 3,000 healthcare partners. The payoff: diagnostics that learn and adapt with each case.

The company's Data & Services business thus takes that de-identified dataset and creates a product, which it licenses to biopharma firms for R&D, clinical trial design, and drug discovery. In 2024, this business line grew 43.2% to $241.6 million. Its 66.2% growth in Q4 reflects its momentum and margin excellence, with 80.3% non-GAAP gross margins and 140% net revenue retention. Tempus now has a total contract value of well over $940 million, a underappreciated indication of long-term demand for its data assets.

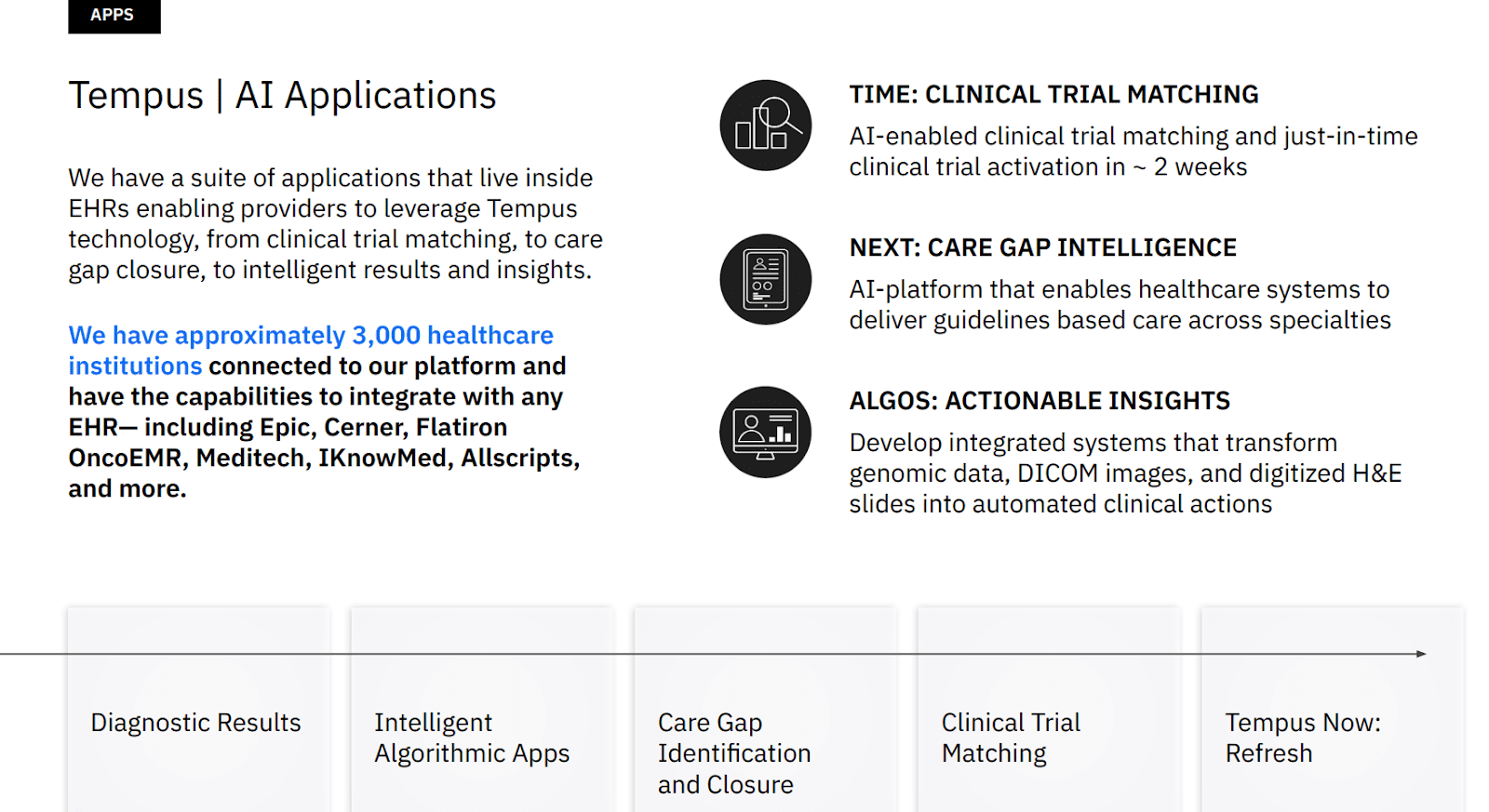

Last, AI Applications, although still embryonic for monetization, strategically matter. Examples such as the Next platform and ECG-AF algorithm, which are already reimbursable by Medicare, represent Tempus’ larger vision: incorporate real-time clinical intelligence into healthcare workflows. These assets not only facilitate sooner intervention opportunities, but also enrichen provider and payor relationships, potentially providing recurring SaaS-like revenues.

Source: Q4 Deck

Competitive Landscape: A Moat Built with Depth of Data and Platform Integration

Tempus occupies a place at the intersection of diagnostics, AI, and healthcare IT, areas typically addressed by separate parties. Diagnostic competitors such as Guardant Health and Invitae concentrate on test development and clinical validation, whereas others like Flatiron and Truveta are centered on aggregation of real-world data. There aren't many, if at all, that occupy both camps with embedded analytics and private data.

Tempus' advantage lies with vertical integration. With control of both inputs (lab-based diagnostics) and outputs (worldly insights, algorithmic applications), the company can provide unparalleled clinical context. It also creates data network effects: increased tests grow the data graph, which enhances AI algorithms and test accuracy, boosting demand. It's a reinforcing feedback loop that competitors without lab infrastructure or clinical access could find difficult to copy.

Ambry not only brings $315 million of high-margin revenue but, with it, takes Tempus into hereditary cancer and rare disease diagnostic categories, categories where genetic counselors are at the center. Significantly, Ambry brings with it earlier points of entry for the patient, enhancing longitudinal datasets and allowing AI tool utilization at an earlier stage. In effect, Ambry is both a horizontal and vertical expansion of Tempus’ data moat.

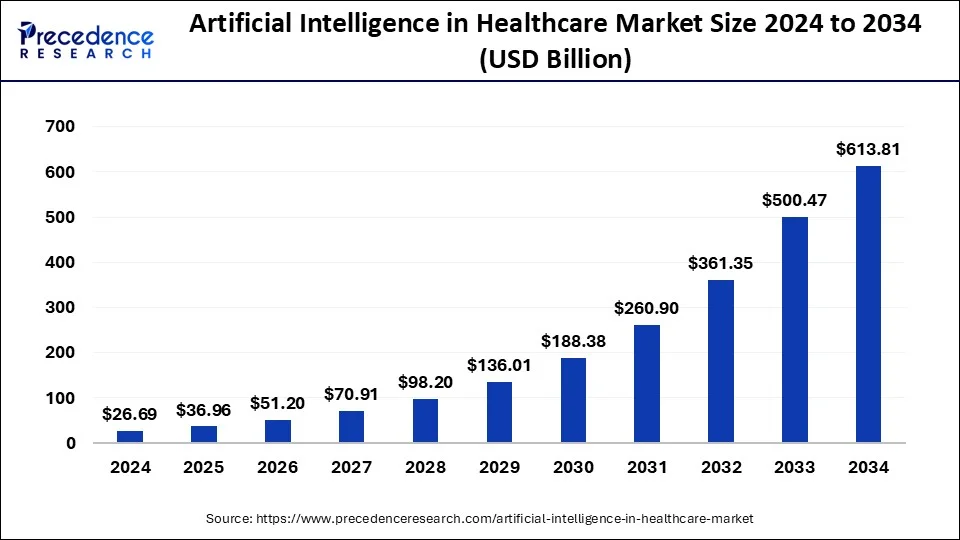

While AI and healthcare data competitiveness is intensifying, Tempus' presence with structured, longitudinal, and multimodal data, combined with regulatory-approved products, provides a defensible advantage. If scaled effectively, this moat can grow as the company expands into disease categories.

Source: precedenceresearch.com

Valuation: In the Platform, But Not On the Optionality

Tempus is valued at an estimated $7.5 billion market cap. Using 2025 revenue guidance of $1.24 billion, the stock sits at around 6.05 forward EV/revenue. On first look, that valuation might look fair versus comps like Guardant Health (7.1 times). With Tempus' persistent GAAP net losses, these comps might appreciate the strategic worth of Tempus.

While its contemporaries are mere test labs, Tempus is a multi-product company with strongly diversified revenue streams and visibility to operating leverage. Its gross margin is rising steadily (55% to almost 62% by 2024), and adjusted EBITDA enhanced by more than $49 million YOY. As soon as management achieves modest profitability by 2025, Tempus will be operating within a valuation regime with revenue multiples starting to shrink and earnings multiples becoming meaningful.

AI-native healthcare software peers, such as Veracyte or even Palantir, but with different models, command 5x–60x revenue multiples, typically, once they demonstrate sustainable, recurring software or licensing revenue. Tempus is not there yet, but its Data & Services and AI Applications segments are pointing there. When those blend shifts happen, Tempus’ revenue will get improved, which will justify expansion multiples.

Optionality is an under-priced asset. If Tempus is successful with productizing additional AI algorithms with Medicare pay (as with ECG-AF), or deploys cloud software for diagnostic interpretation, the company could sustain SaaS-like unit economics. Such a turn toward that direction would significantly change its valuation framework, diagnostics to healthcare tech.

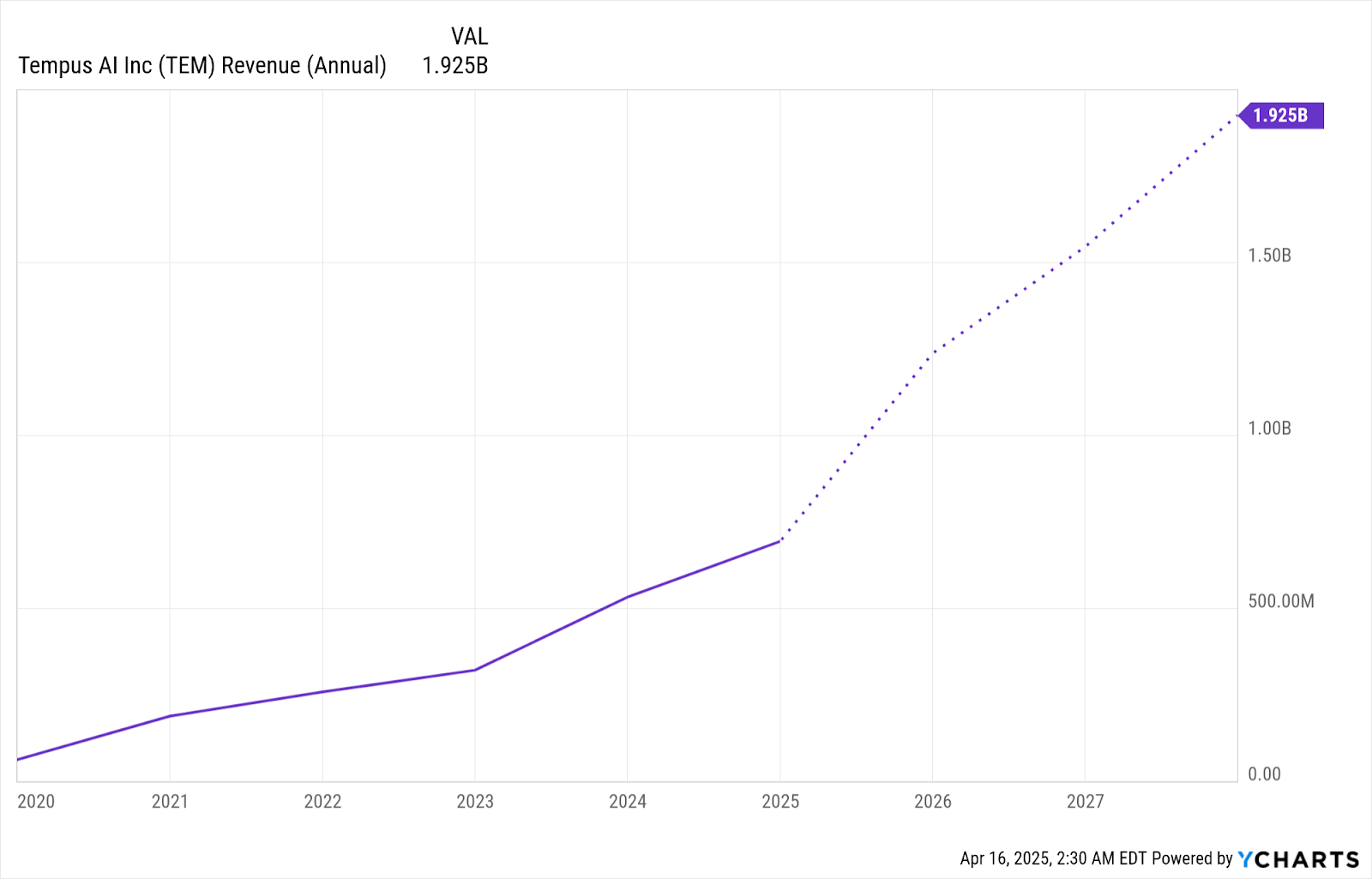

In the short term, a conservative valuation model based on applying a 7 times revenue multiple to 2025E revenues results in a price range of $45–$48 per share. With increasing proof of margin expansion and recurring AI revenues, re-rating to a range of $55–$60 is well within range for 12–18 months.

Source: Ycharts

Risk Evaluation: A Promising Platform Continues to Walk Executive Tightropes

It is not without material risks, both operational and structural, despite its potential. Regulatory complexity introduces chronic uncertainty first and foremost. Whilst ADLT and Medicare reimbursements are tailwinds, a reversal of coverage decisions and scrutiny of algorithmic diagnostics could impede adoption. Secondly, the FDA’s shifting position regarding software-as-a-medical-device (SaMD) may place new compliance barriers upon Tempus’ AI Applications, which will push commercialization back.

Second, execution risk is a major threat. The integration of Ambry will need to be kept under close control to maintain its margin profile and momentum with hereditary testing. Any misstep will weaken operating leverage and push aside Tempus’ AI efforts. Moreover, maintaining 140% net revenue retention will be more challenging as the base matures. Existing biopharma client growth cannot be assumed.

Third, Tempus' cost model still warrants scrutiny. While non-GAAP measures indicate robust progress, GAAP net operating losses are still high based on $547.7 million of 2024 stock-based compensation. Absent normalized stock grants, dilution may exert downward pressure on shareholder returns over the long term, particularly if cash burn persists past 2025.

Finally, there is increasing competition. Niche but deep AI players may pioneer niches in diagnostics or data infrastructure. Big players with greater capital and AI models will likely move into healthcare as well. Tempus's protection relies upon its rate of iteration and capacity for sole-source data pipelines and payer connections. In summary, Tempus is a category-defining business, still, however, operating at a scaling stage. Long-term potential is intriguing, but not without risks.

Source: Q4 Deck

Conclusion

Tempus is constructing the foundation for a future with diagnostics that are no longer static images but dynamic, AI-driven roadmaps for clinical decision-making. With a model for a differentiated platform, driving top-line growth, and viable path to profitability, the company has a unique combination of strategic vision and commercial momentum. For long-term investors, Tempus is potentially one of the decade's most compelling healthcare platform plays.

Recommended Articles