Altria’s Smoke-Free Future: Transformation or Trouble?

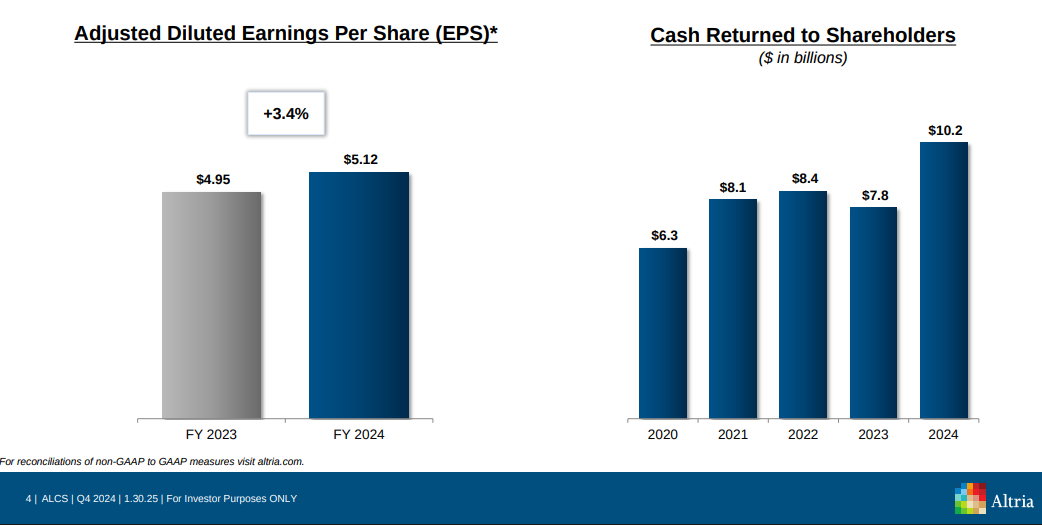

- Altria posted 2024 adjusted EPS of $5.12 (+3.4% YoY), but revenue excluding excise taxes remained flat at $20.4B, reflecting mature category limits.

- Smoke-free revenue hit $2.8B, up YoY; on! pouches saw 44.4% volume growth, while NJOY’s share rose to 6.4% but faces litigation risks.

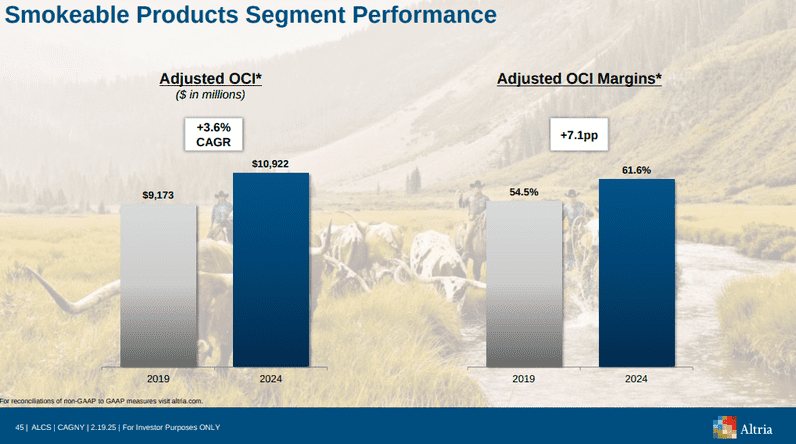

- 2024 adjusted operating margin was 60.3%, and smokeables saw a 2% OCI gain despite a 10.2% volume drop—pricing power remains intact.

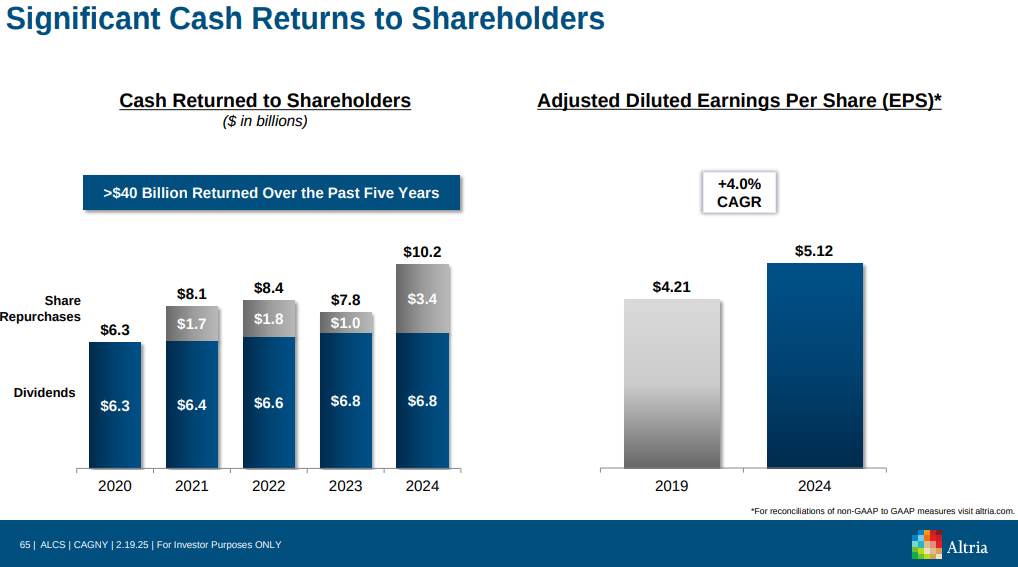

- $10.2B returned in 2024, with $6.8B in dividends and $3.4B in buybacks; new $1B repurchase plan set for 2025.

TradingKey - Altria Group (MO) has long been a pillar of the US tobacco industry, centered around its powerhouse brand, Marlboro, and a business model yielding consistent dividends. Today, however, the firm is at a crossroads. With declining rates of smoking and rising regulatory pressure, Altria is driving full-steam toward a smoke-free future. The transformation isn’t skin-deep, it’s systemic, backed by billions in investment in e-vapor, nicotine pouches, and heat-not-burn tobacco. Still, investors are skeptical. Will this transformation generate a growth story for the long term or get derailed by regulatory turmoil and black market competition?

Altria's results in 2024 are a reflection of this tension. It delivered strong adjusted EPS of $5.12 (+3.4% YoY), but revenue was unchanged, and key smoke-free goals were diminished by unregulated e-vapor proliferation. Altria does, though, have a good story of transformation, margin stability, and return of capital. It's also, though, a tale marred by litigation and a shifting marketplace more quickly than can be regulated.

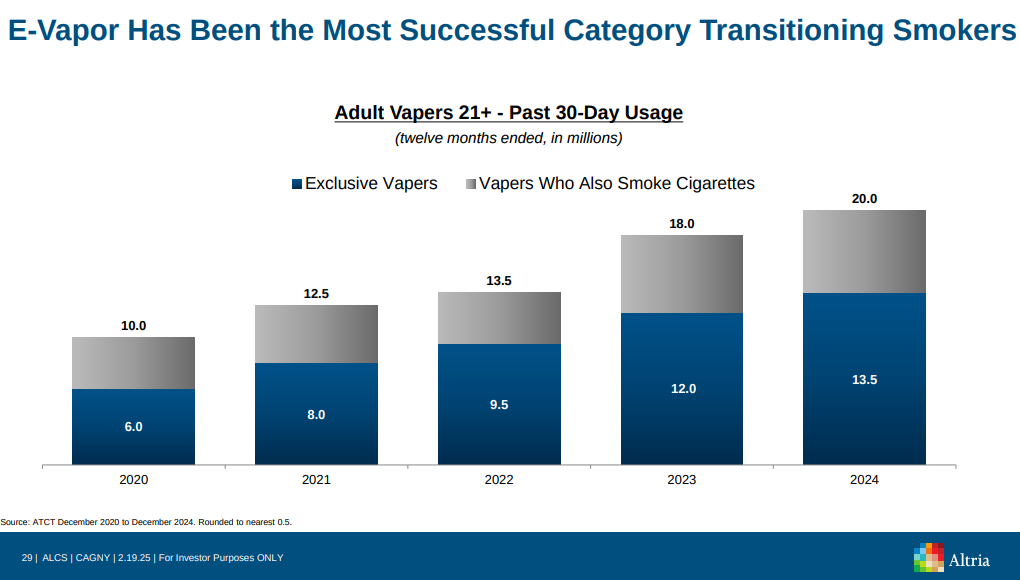

Source: Altria Presents at the Consumer Analyst Group

The Smoke-Free Initiative: A Well-Intended Shift with Unequal Momentum

Altria's model is divided: a maturing but declining smokeable segment, together with a promising, rapidly growing smoke-free segment. On the smokeable side, Marlboro carries a retail share of 41.7% while facing a shipment decline of 10.2% in 2024. The segment's adjusted operating company income (OCI) actually grew by 2%, with the margin increasing to 61.6%, again showing the pricing power and cost discipline responsible for this core brand being a cash engine.

The company's real growth bets are in its smoke-free business, for example, Helix's on! nicotine pouches and NJOY's FDA-regulated e-vapor. In 2024, net smoke-free revenues incrementally rose to $2.8 billion, while shipment volume in on! was up 44.4% YoY, with repeat shopping exceeding 800K shoppers. Helix even turned a profit a year early.

The NJOY, acquired during the second half of 2023, is Altria's weak link and also its transformational jewel. Shipments by volume of consumables during fourth-quarter 2024 were up by 15.3%, while the brand's share in the U.S. retail value was up by 2.8 share points at 6.4%.

JUUL's successful patent litigation, though, has the power to ban NJOY ACE imports as early as March 31, 2025, a reversal potentially harming Altria's 2028 smoke-free volume and revenue goals. The company is countering, but timing is uncertain.

In addition, while Altria's hot tobacco product, Ploom, is promising in testing, wherein 74% of smokers reduced cigarette consumption, the bigger U.S. hot tobacco opportunity lies in its infancy. Without broad FDA approvals and consumer demand, expanding this segment will be challenging.

Engaging Illicit Rivals as well as Institutional Giants The nicotine competition environment is more fragmented, and maybe more dangerous, than ever. Altria continues to dominate in combustibles, but its smoke-free aspirations are confronted with a significant challenge from three camps: regulated established players, outlaw illicit actors, and well-funded global giants.

First, there are JUUL and Reynolds (with Vuse), who fight for share in the FDA-regulated e-vapor category. NJOY's proprietary advantage is its full portfolio of FDA marketing authorized orders, the sole approved menthol e-vapor offerings. However, this advantage is undercut by the meteoric rise in unauthorized disposable e-vapes. Illicit items control more than 60% of e-vapor volumes today and contribute to underage consumption, a problem the FDA has not yet truly curtailed.

There are also global players such as Philip Morris International (PMI), who globalized IQOS and today lead the heating tobacco category outside the U.S. Altria's deal in 2024 to transfer U.S. IQOS rights to PMI earned a $2.7 billion payday but exposed it to losing share in a category it once set out to dominate.

At the same time, new entrant brands such as Sweden's Match, acquired by PMI, are gaining share in pouches. Altria's on! brand expanded share in U.S. oral tobacco by 2.0 points, reaching 8.9% in Q4 2024, but it is a challenger brand in a highly competitive category. All this has caused Altria to take a more conservative investment posture, particularly in e-vapor. CEO Billy Gifford explained that “until we make real progress addressing the illicit marketplace.we will adopt a disciplined posture in terms of investing in NJOY and beyond.” This could defend margins, but also limit innovation.

Source: Altria Presents at the Consumer Analyst Group

Financing Structure: Margin Control and Capital Allocation Discipline

Even in a declining industry, Altria has crafted strong financial solidity. For 2024, total adjusted OCI margin was 60.3%, sustaining its ten-year track record of operating efficiency. Adjusted EPS was up at $5.12 (+3.4% YoY), and management reaffirmed 2025 EPS guidance of $5.22 to $5.37, a 2% to 5% increase range.

Altria's share repurchase strategy is also strong. The firm paid $10.2 billion in dividends back to shareholders in 2024, $6.8B of dividends and $3.4B in share repurchasing, displaying both cash-generating strength and belief in intrinsic worth. It repurchased 5.8 million shares in the fourth quarter alone at a cost of $53.04 per share and launched a fresh $1B 2025 share repurchase plan.

Capex is moderate in the range of $175M to $225M for the year 2025, with debt/EBITDA at a reasonable 2.1x. The payout ratio is at around 80%, a number showing commitment but restricting room for disruptive M&A. Even so, Altria's least recognized strength could be its tax planning and non-core monetization. The $2.7B IQOS gain supported 2024 earnings and offset charges from the NJOY transaction as well as the Skoal trademark impairment.

That being said, not everything was fine. Revenues excluding excise taxes were unchanged YoY in 2024 at $20.4B, while the NJOY litigation clouds future contributions to cash flow. Furthermore, youth use of tobacco continues to be controversial, particularly as unregulated e-vapor products spread due to a lack of enforcement.

Source: 2024 Deck

Valuation: Undervalued or Value Trap

Altria is currently trading presently at ~10.5x 2025e EPS, a discount when compared with peers such as PMI (~21.1x). On EV/EBITDA, MO also trades at ~9.25x, a discount. The market seems to reflect a risk of terminal decline or ongoing litigation, even as they have stable cash flows, not to mention a high-60% EBITDA margin business.

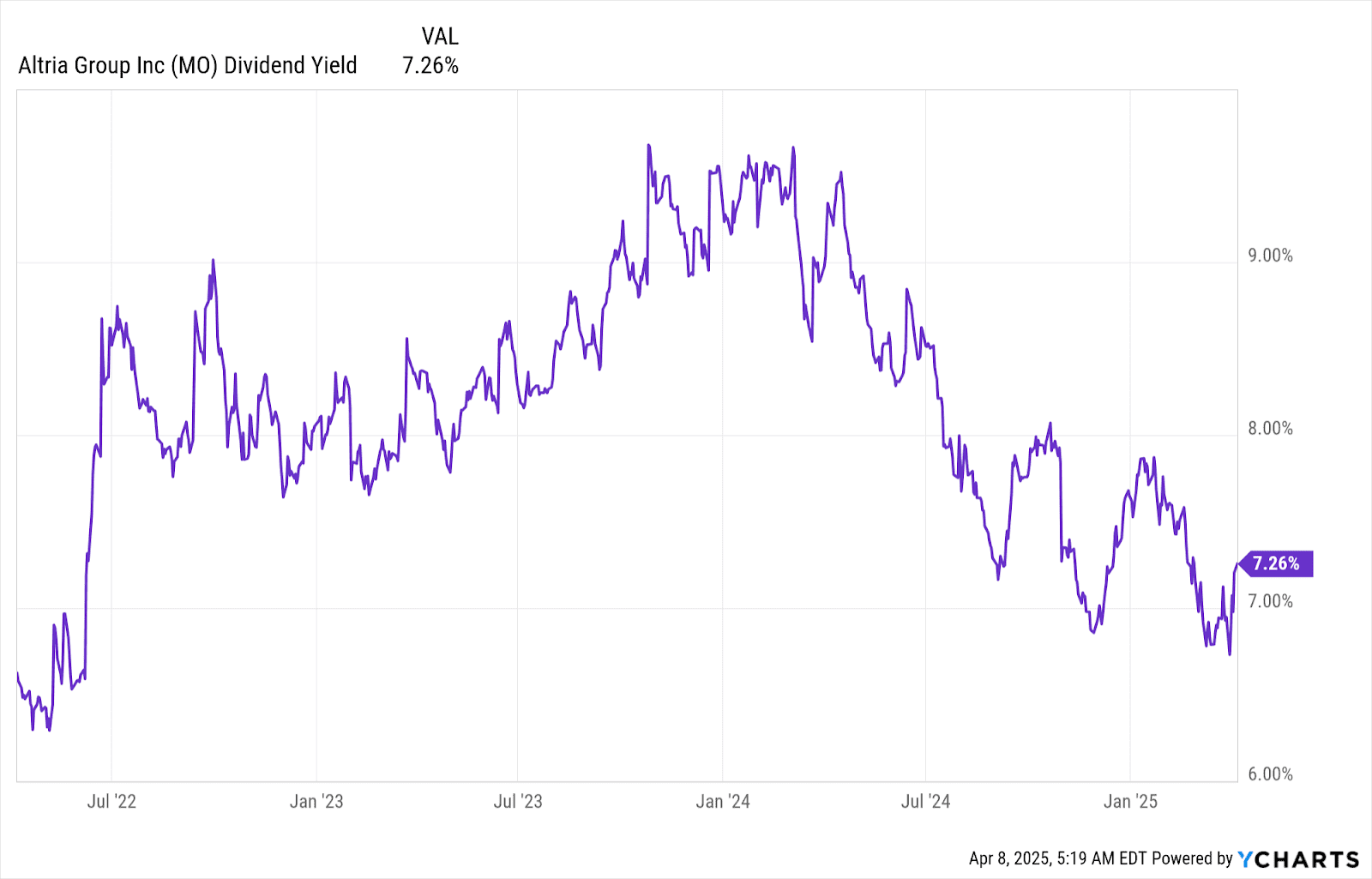

A conservative DCF model, with flat revenues, moderate margin decline, and a 3% growth rate at the finish, results in a fair value of between $58 and $64 per share, creating upside of 15% to 25% from today's levels (~$51). If NJOY litigation settles in a positive manner and FDA compliance strengthens, upside may be higher, considering Altria's +7% dividend yield.

Yet, if regulatory inaction continues or NJOY is disrupted materially, investor sentiment may deteriorate further. Smoke-free ambitions of Altria depend upon a legitimate marketplace functioning, a reality as yet untimely.

Source: Ycharts

RISK: Litigation, Regulation, and Market Fragmentation

There are a mosaic of risks confronting Altria that can alter its path. Most prominent is regulatory uncertainty. The FDA's sluggish approval process and lax enforcement empower unlawful players, undercut NJOY, while distorting category economics. Moreover, JUUL's litigation success against NJOY has the potential to upend a central revenue source.

Aside from regulation, macroeconomic factors such as inflation and income compression are driving shoppers towards discount cigarettes as well as black market e-vapor substitutes. Altria's use of pricing to make up for declining volumes could ultimately reach a limit. Lastly, the future of the firm's transformation rests in its capability to innovate and expand new items, an unsure proposition in light of previous failures (e.g., JUUL investment, IQOS pullback).

Source: Altria Presents at the Consumer Analyst Group

Verdict: Smoke-Free Vision Collides with Harsh Marketplace Realities

Altria is a paradox. It is a cash-rich giant with enviable margins and strong brand equity but in a structurally declining, politically exposed industry. Its smoke-free shift, led by NJOY and on!, is progressing but not yet sufficiently to counteract headwinds from black markets and regulatory uncertainty. If Altria can ride out litigation storms and take advantage of tailwinds in terms of enforcement, its value implies substantial upside. Without, though, more clear-cut resolution of the NJOY issue and more firm action by the FDA, Altria can be expected to continue being valued like a melting ice cube, albeit a well-rewarding one. Currently, Altria is a hold with asymmetrical upside potential, but the clock is running for its promise of a smoke-free future.

Recommended Articles