TSMC's Q1 2025 Earning: Technological leadership and AI demand drive continued growth in performance

As the world's leading wafer foundry, TSMC's Q1 2025 financial report showed strong performance, highlighting its core position in the fields of AI chips and HPC. The market regards TSMC's financial report as a weathervane for the AI industry, and this better-than-expected financial report has encouraged confidence in the fragile market.

Financial performance: strong growth and high profitability

1. Revenue and net profit

TSMC's revenue in Q1 2025 reached NT$839.25 billion, a year-on-year increase of 41.6%, and a quarter-on-quarter decrease of about 5.1% from the fourth quarter of 2024. Although there was a slight decline from the previous quarter, mainly due to seasonal fluctuations in the smartphone market, the annual growth rate set the fastest record since 2022, reflecting the strong drive of AI server chips and smartphones.

In terms of net profit, TSMC achieved NT$361.6 billion, a year-on-year increase of 60.3%, significantly exceeding the market expectation of NT$346.76 billion. EPS was NT$13.94, up 60.4% year-on-year, showing a significant improvement in the company's profitability.

2. Gross profit margin and operating efficiency

The gross profit margin in the first quarter was 58.8%, slightly lower than 59% in the fourth quarter of 2024, but still higher than the market expectation of 58.1%. The operating profit margin was 48.5%, reflecting TSMC's cost control ability and technology premium in high-end process technology. The slight decline in gross profit margin was mainly due to the initial yield optimization costs of the new 2nm process and the increase in overseas factory operating expenses, but the overall level remained industry-leading.

3. Capital expenditure and future layout

TSMC's capital expenditure in the first quarter of 2025 was approximately US$10 billion, and the full-year plan was to maintain it at US$38 billion to US$42 billion, an increase of approximately 19%-40% year-on-year. These funds are mainly used to expand production of 3nm and 2nm advanced process nodes, as well as to increase the capacity of CoWoS. This shows TSMC's long-term confidence in the demand for AI and HPC, and its strategic determination to consolidate its technological leadership.

Technology and product structure: the driving force of AI and advanced processes

1. Revenue contribution of advanced processes

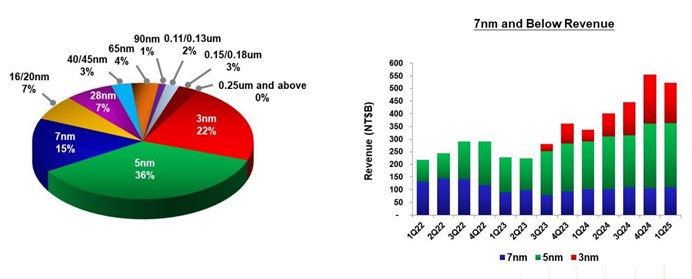

TSMC's technological barriers in the field of advanced processes are the core driving force of its performance growth. In the first quarter of 2025, 3nm process accounted for 22% of wafer sales revenue, 5nm accounted for 36%, and 7nm accounted for 15%. The three together contributed 73% of wafer sales, which was a further increase from 67% in the fourth quarter of 2024. This structural revenue growth highlights TSMC's competitive advantage in the high-end chip market, especially in the fields of AI accelerators and HPC chips.

Source: TSMC

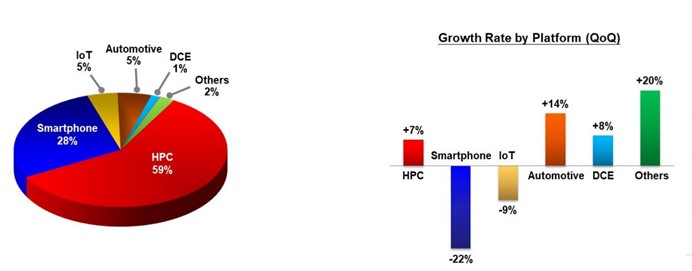

2. Explosion of demand for AI chips

The demand for AI chips is the biggest highlight of TSMC's performance in 2025. HPC-related revenue increased by more than 70% year-on-year, accounting for nearly 60% of total revenue, mainly due to AI accelerator orders from customers such as NVIDIA and AMD, and the expansion needs of cloud computing vendors such as Microsoft and Amazon. TSMC expects AI accelerator chip sales to grow 100% year-on-year in 2025, with a compound annual growth rate (CAGR) of 45% from 2024 to 2029, becoming the pillar of long-term growth.

However, the capacity bottleneck of CoWoS packaging technology limits some of the shipment potential. To meet this challenge, TSMC is accelerating the expansion of CoWoS capacity, and it is expected that the capacity will double by the end of 2025 to meet the explosive demand for AI chips.

Source: TSMC

Macro environment and potential risks

1. Tariff policy

TSMC is highly dependent on local manufacturing in Taiwan, and the tensions in the Taiwan Strait and the US restrictions on semiconductor exports to China have brought uncertainty to its operations. In early 2025, the United States briefly imposed a 32% tariff on Taiwan's semiconductor products, causing customers to stock up in advance, pushing up first-quarter revenue. However, if the United States implements more extensive semiconductor import restrictions in the future, it may have an impact on TSMC's global supply chain.

The Arizona plant plans to mass-produce 4-nanometer chips in 2025, and plans to build 3-nanometer and 2-nanometer plants. Despite this, the monthly wafer output of the Arizona plant is far from enough to meet market demand, and the operating costs are high. Affected by the US tariff policy and the imbalance between supply and demand, TSMC plans to implement a 30% price increase for the production of 4-nanometer chips in its US plant. This strategy is both a response to rising costs and a reflection of the tight demand for AI chips. However, the price increase may weaken the order willingness of some

2. Industry cycle and inventory adjustment

Despite the strong demand for AI chips, the traditional consumer electronics market is still affected by seasonal fluctuations, resulting in a quarter-on-quarter revenue decline of about 5.5% in the first quarter. In addition, customers' advance stocking to avoid tariffs may trigger subsequent inventory adjustment risks, and demand may slow down in the second quarter of 2025.

Future trends and performance sustainability judgment

1. Sustainability of growth momentum

The explosive growth in demand for AI chips provides long-term momentum for TSMC. The market expects that global AI hardware spending will account for 80% of total generative AI spending in 2025. As a major foundry, TSMC's revenue growth is expected to remain at 24%-26%, far exceeding the industry average (about 10%). The 2nm process has entered mass production, leading its competitors Intel and Samsung by about a year, and the technology premium will continue to support high gross profit margins. By investing in factories in the United States, Japan and Europe, TSMC effectively disperses geopolitical risks while meeting customers' localized production needs.

2. Geopolitical risks and response strategies

In the short term, TSMC may face pressure from seasonal demand declines and inventory adjustments, and revenue growth may slow in the second quarter, and gross profit margins may be under pressure in the 57%-59% range. The uncertainty of US tariff policies has exacerbated market risks, and customers' advance stocking may lead to subsequent demand fluctuations. To this end, TSMC needs to smooth the impact of inventory cycles through flexible capacity allocation and customer communication. The explosive growth in demand for AI chips has provided long-term momentum for TSMC. As a major foundry, TSMC's revenue growth is expected to remain stable and far exceed the industry average.

Geopolitical risks remain the biggest challenge facing TSMC. The tensions in the Taiwan Strait and US restrictions on semiconductor exports to China may disrupt the supply chain. TSMC needs to continue to promote its global layout and reduce its dependence on Taiwan.

3. Market Outlook

TSMC's financial performance not only reflects its own growth potential, but also drives the valuation repair of the semiconductor supply chain. The continued expansion demand of customers such as NVIDIA and AMD, as well as the investment of cloud computing vendors in AI infrastructure, provide TSMC with a stable order flow. The current stock price is considered to underestimate its long-term potential in the field of AI. Investors' confidence in TSMC stems from its technological leadership and the explosive growth of the AI market. TSMC expects revenue growth of about 20% in 2025. Although tariff uncertainties may lead to minor adjustments, the overall market sentiment remains optimistic.

Conclusion

TSMC's first quarter 2025 financial report shows its irreplaceable position in the field of AI and high-performance computing. Strong revenue and net profit growth, technologically advanced processes, and a diversified customer base jointly support the sustainability of its performance. In the short term, seasonal fluctuations, inventory adjustments and geopolitical risks may bring uncertainty, but TSMC actively responds through global layout and large-scale capital expenditures, and its long-term growth momentum remains strong.

For investors, TSMC's current valuation has not yet fully reflected its growth potential in the AI chip market. It is recommended to pay attention to its progress in 2nm process mass production and CoWoS capacity expansion. At the same time, it is necessary to closely monitor changes in US tariff policies and the situation in the Taiwan Strait. As a weathervane of the AI industry, TSMC's future performance will continue to lead the market's confidence in the semiconductor and AI industries.

Recommended Articles