SFL: Monetizing Assets with Strategic Capital

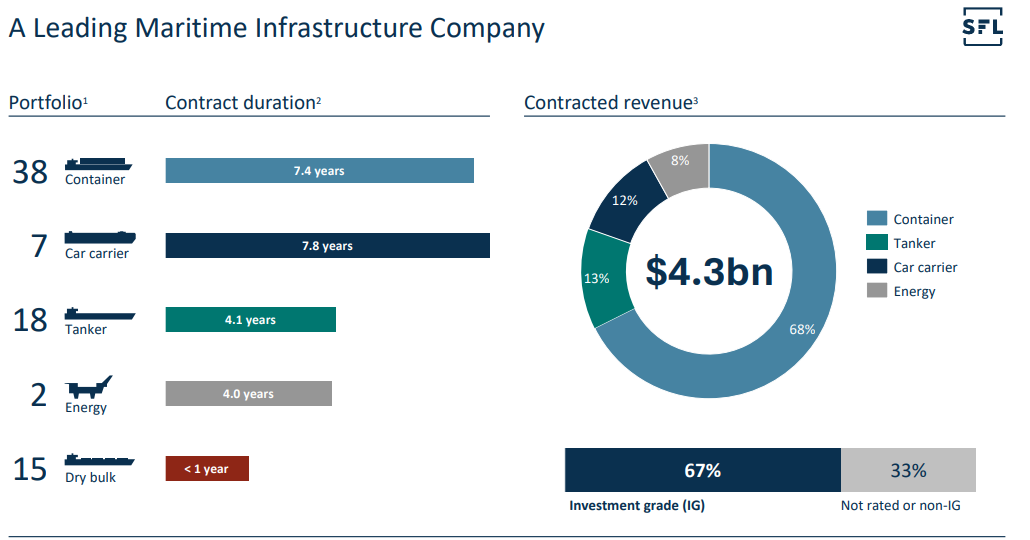

- SFL has secured $4.3 billion in fixed-rate charter backlog, adding $2 billion of new commitments in 2024 alone, primarily with investment-grade counterparties.

- 2024 adjusted EBITDA hit $507 million on $904 million revenue, a 56% margin, fueled by disciplined capital deployment and nearly 100% vessel utilization.

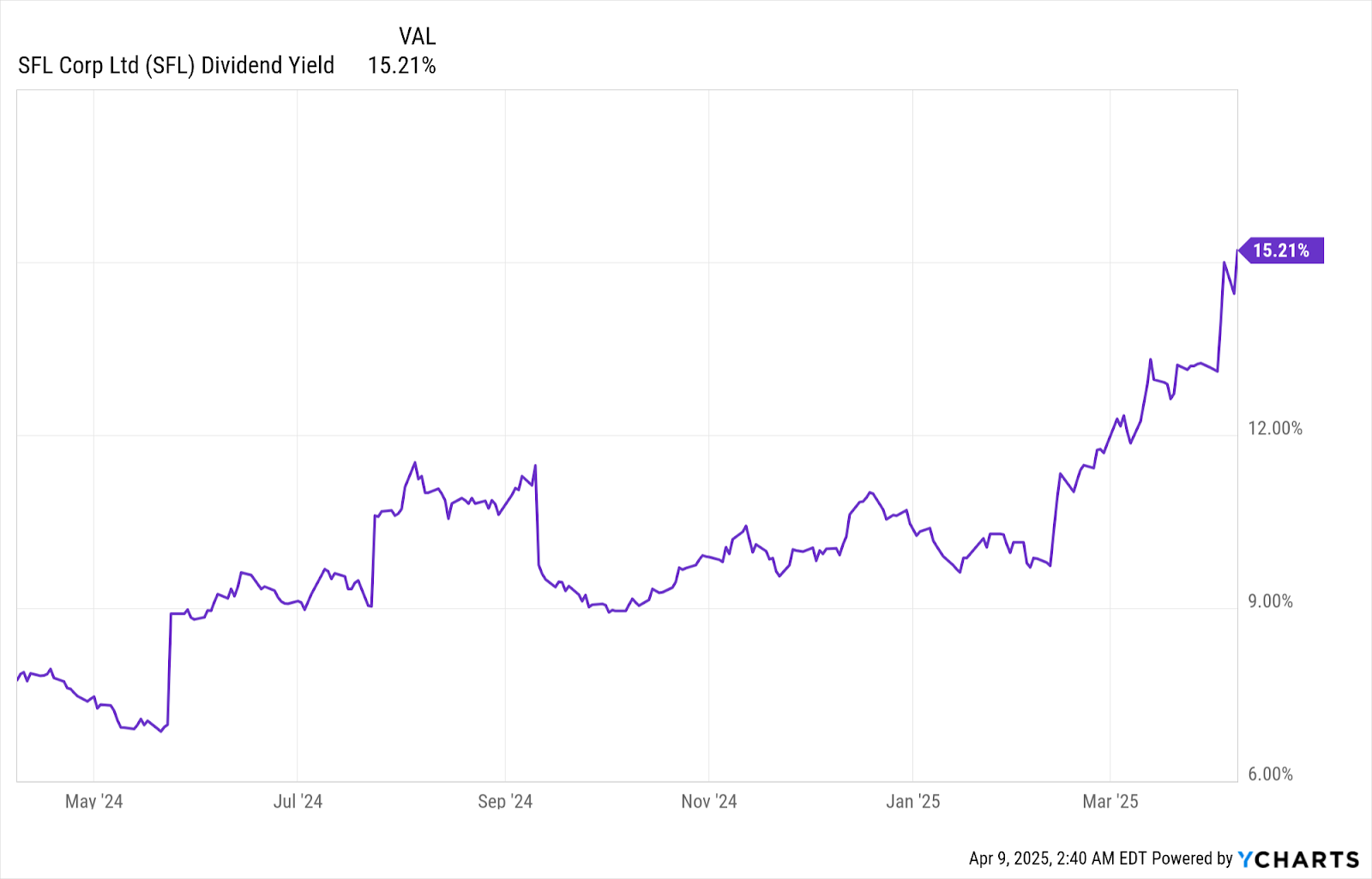

- Quarterly dividend of $0.27 equates to a 10.2% forward yield, supported by 84 consecutive payouts and consistent operating income.

- Fleet growth includes seven new vessels in 2024, each tied to long-term charters, showcasing a yield-plus-duration strategy with low residual risk.

SFL Corporation: A Defensive Yield Play Backed by Charter-Backed Cash Flows and Asset Flexibility

TradingKey - In a time when platform monetization and the AI revolution overshadow market narratives, SFL Corporation (SFL) advances a contrarian thesis founded in real assets, defensive yield, and long-dated charter agreements with investment-grade counterparties. In contrast to asset-light software companies or shipping names with a seasonal nature subject to spot-rate fluctuations, SFL derives stable, recurring cash flows from a diverse pool of shipping assets. With 84 successive quarterly dividends and a forward yield of around 10%, the return profile of its capital is best in class among shipping peers. The true potential lies, though, in its power of growing adjusted EBITDA while sustaining risk-adjusted returns by selective deployment of capital into long-dated charters, a strategic leverage most investors ignore.

On the surface, SFL looks like a yield trap in a commoditized business. Closer scrutiny, though, serves up a maritime platform infrastructure business that has evolved from a finance lease aggregator into a blue-chip operator in step with peers such as Maersk, Hapag Lloyd, and Volkswagen. Despite the industry's tailwinds, such as rate normalization, lower rig utilization, SFL has consistently expanded its $4.3 billion fixed-rate backlog, adding a further $2 billion in new commitments during 2024 alone. This rewards management's disciplined approach to allocating capital, as well as demonstrating the power of originating charters structurally superior to spot markets. The union of high-fixed revenue visibility, efficient leverage, and low residual asset risk serves up a cash flow compounder whose value institutional capital has yet to realize.

The wider implication: while software and AI platforms sprint toward trillion-dollar valuations, investors looking for downside protection with equity-like upside in a world of reflation can find asymmetric opportunity in SFL. With shipping capacity concentrating and rig supply contracting, the firm's reinvestment flywheel, backed by locked-in EBITDA, has the potential to unlock additional capital appreciation in addition to its already-plentiful dividends.

Source: Ycharts

Maritime Infrastructure as a Platform: A Differentiated Model Built on Charter-Backed Stability

SFL Corporation is in the business of real asset ownership coupled with financial engineering. It has a diversified fleet of more than 80 vessels and rigs, comprising container vessels, tankers, car carriers, dry bulk vessels, and offshore drilling units. Its business model revolves around entering into long-term, fixed rate charters with creditworthy counterparties, thus ensuring cash flows free of spot market volatility. Around 68% of its backlog is invested with investment-grade customers, thus ensuring downside protection against defaults or cyclical downturns.

The structure of the company is geared toward reinvesting. Instead of pursuing speculative charter rates or high-velocity asset flips, SFL reinvests in accretive vessel acquisitions tied with firm employment. In 2024, it acquired a total of seven vessels, comprising LR2 product carriers, car carriers, and chemical carriers, together with new long-term charters, demonstrating a disciplined model through a focus on yield plus duration. With a more than seven-year average charter tenure in its container fleet and its tankers, the business is more akin to a REIT-like income engine rather than a speculative shipping trader.

SFL also gains through optionality through its hybrid lease structures, such as its sale-type, or sale, and its finance, or finance lease arrangements, generating interest income, as well as accretive depreciation gain. This strategy achieves a mixture of operational and financial return, while keeping residual value risk in check. Unlike more traditional shipping operators subject to volatile rate swings, the operational platform of SFL revolves around prudent stewardship of cash, with administrative costs in excess of $20 million on some $1 billion of revenue, an incredibly lean profile.

Effectively, SFL acts more as a platform of infrastructure rather than a shipping business. It takes depreciating assets and turns them into income-producing instruments by inserting risk-mitigating, long-term agreements into its capital structure. This positions the firm in a position to raise capital at favorable terms, as shown by more than $1 billion in asset financings and unsecured bond issuances during 2024.

Source: Q4-Deck

A Fragmented Battlefield: Why SFL’s Discipline Sets It Apart in a Volatile Maritime Arena

The world's maritime industry is one of the most capital-intensive sectors, being highly fragmented, with more capacity risks, dynamic charter rates, and aging fleets putting profitability in danger. Though no dominant player exists, large groups of conglomerates include Seaspan, Danaos, Frontline, and Scorpio competing fiercely in segments from container shipping through dry bulk to tankers. These companies tend to achieve scale through asset acquisition cycles, setting themselves up for overbuilding in upswings and underutilization in troughs.

By way of contrast, SFL eschews scale for scale's sake. In contrast to chasing fleet size or headline TEU levels, it prefers contractual quality. Charter tenor, counterparty credit, as well as revenue clarity, take precedence over asset numbers. For example, while SFL has a handful of car carriers, they are time-chartered for top automotive clients, producing a substantial proportion of total operating earnings. Similarly, container exposure is in long-term arrangements with worldwide liners, showing strategic counterparty risk rather than reliance on volatile markets.

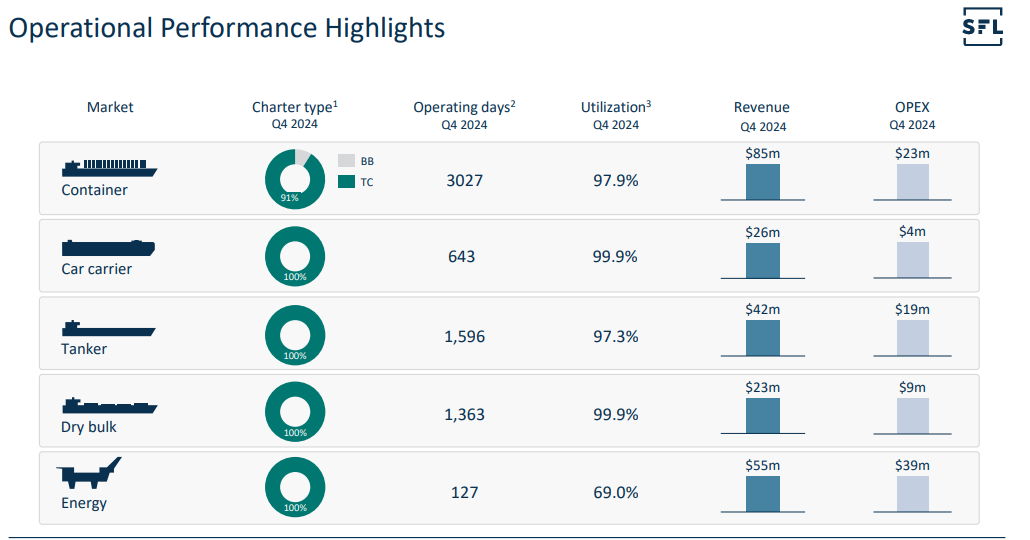

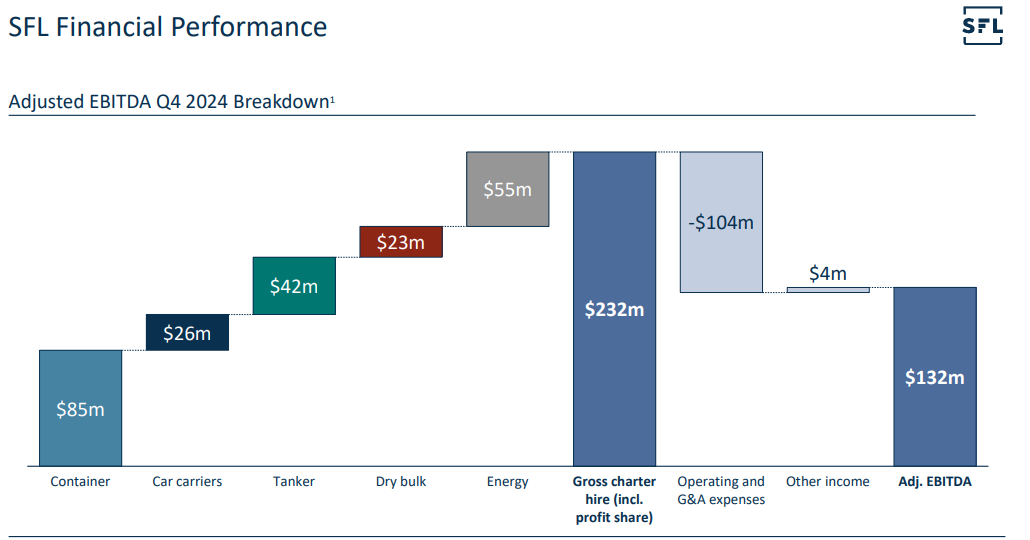

Moreover, SFL's asset diversification in terms of containers, tankers, dry bulk, and offshore rigs is a natural hedge. During fourth-quarter 2024, its business in the containers was leading in terms of EBITDA, followed by the tanker business as well as car carriers. Such diversification acts as a hedge against single-market exposure. Interestingly enough, fourth-quarter revenue was adversely impacted by redelivery of a drilling rig after contract expiration. However, the company replaced this with fresh charters while maintaining over $130 million of adjusted EBITDA in the period.

SFL's emphasis on long-duration contract structures and steady revenue growth is the polar opposite of the cycle peers, who are more likely to suffer from steep earnings declines during economic recessions. The strategy has also won the lenders' trust, as the company has been able to issue new unsecured debt at good terms.

Source: Q4-Deck

Engines of Growth: Monetizing Charter Backlog, Rising EBITDA, and Disciplined CapEx

SFL's growth does not depend on volume throughput but rather origination of smart contracts and financial efficiency. With a backlog of $4.3 billion and a history of uninterrupted dividends, the business is more akin to a cash-generating machine than a typical operator. The annual revenue in 2024 was $904 million, with adjusted EBITDA of $507 million, representing a more than a 55% EBITDA margin, a phenomenal performance for a business with requirements for a large amount of cap. Effective use of ships, in the range of 100% in car carriers, tankers, and bulk trade, underpinned profitability. Control of costs helped as well. Depreciation remains the largest cost at $239 million annually, but admin costs are reduced. Interest charges of $183 million are up but comfortably offset by operating profit of $307 million. There is over $130 million in cash, plus a conservative equity margin. The firm has prudent financial room.

The capital has been invested strategically. Five new large containerships were financed through pre- and post-delivery loan facilities, with the second 5% payment made by SFL. Substantially, the vessels are backed by long-term charters, hedging asset residual risk. The success of the firm in winning $48 million in legal damages in a rig redelivery dispute is a further indication of management discipline in operations as well as contract enforcement.

Monetization of scrubber savings under contingent charter arrangements contributed more than $10 million in revenue in 2024, a testament that the company maximizes incremental cash flow opportunities in addition to base charter rates. Coupled with periodical asset sale-and-leaseback arrangements, all these levers drive consistent free cash flow, recycled into dividends or new vessel deployment.

Source: Q4-Deck

Valuation and Risk: Asymmetric Yield in a Repricing Macro Environment

SFL is valued at a reasonable price given its strong income stream. With a net income of $130 million in 2024, a per-share earnings of $1.01, and a share price of around $10.55, the firm has a price-earning ratio of slightly more than 10. Its EV/EBITDA metric fluctuates around 7x, lower than infrastructure peers, lower than even capex-heavy leasing peers with the same long-term cash flows.

What lends this multiple appeal is the embedded yield. With a $0.27 quarterly payout, the forward yield of SFL is in excess of 10%. The payout is comfortably covered by earnings and supported by multi-year charter agreements. The firm's fixed-rate backlog also supplies forward visibility, with billions in new commitments having been booked in 2024 alone.

There are still risks. A protracted decline in oil prices might cut the demand for offshore rigs, especially as unbooked rigs seek redeployment. The firm is also subject to counterparty risk, albeit reduced due to investment-grade clients, and residual ship value deterioration as more new, greenfleet ships are introduced into the market. Technological obsolescence is a underestimated risk, especially in segments such as tankers and drillships where new platforms can surpass traditional assets.

Furthermore, leverage costs could be impacted by interest rate volatility as well as refinancing risks. Though SFL raised more than $1 billion of 2024 financing, future funding could be obtained at wider spreads if macro conditions are tightened. Finally, ESG focus in shipping, regulatory restrictions, as well as cyber exposures, might raise compliance costs or limit access to capital.

Source: eia.gov

Conclusion:

SFL Corporation embodies a distinct combination of yield, stability, and reinvestment discipline in a volatile sector. Its consistent ability to monetize assets through long term charters, achieve near-full utilization, and produce structurally elevated EBITDA margins positions it as an under-recognized infrastructure-like vehicle for income investors. In a rising rate environment with a fragmented macro backdrop, SFL exposes investors to asymmetric return with well-managed risks, providing both capital preservation and long term potential.

Recommended Articles