SoFi Technologies: Rewiring Financial Infrastructure from the Ground Up

- Financial Services and Tech now comprise 47% of adjusted net revenue in 2024, up from 38% in 2023, accelerating the shift away from lending.

- $23.2B in loans originated in 2024, with $67M revenue from LPB off-balance-sheet deals like Blue Owl’s $5B forward pipeline.

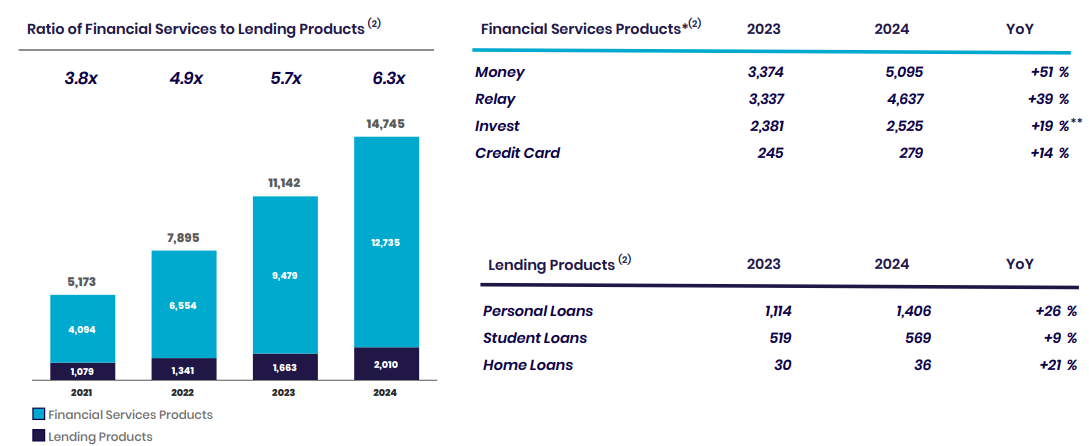

- Financial Services revenue hit $257M (+84% YoY) with 45% contribution margin; revenue per product rose 37% YoY to $81.

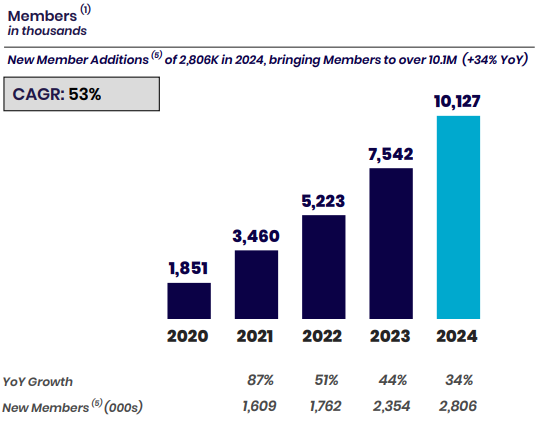

- 168M accounts (+15% YoY); partnerships like U.S. Treasury’s Direct Express drive recurring B2B revenue across public and private sectors.

TradingKey - Amongst a sea of incumbent banks and fintech aspirants, SoFi Technologies (SOFI) is working stealthily towards a scale-enabled, structurally advantaged financial operating system. Under the surface turbulence of its stock price is a three-dimensional business, GAAP-profitable, diversely revenue-streamed away from high-capital lending, and deeply rooted in consumer finance as well as B2B infrastructure. It's not merely a neobank. It's a digital, end-to-end financial services platform powered by a Shopify-like technology stack with a monetization engine in the process of becoming capital-light by design.

Although market sentiment continues to keep SoFi grounded in its financing roots, the more recent evolution tells a different tale. SoFi's top line has come a long way in shifting towards fee-based revenue, with its financial services and tech platform segments today representing 47% of total adjusted net revenue in 2024, up from 38% in 2023. This transformation is not cosmetic. It effectively restrikes the business's value profile, cost base, and credit cycle sustainability. The question, no longer, is if SoFi's a profitable business, but rather if the marketplace has yet to realize the sustainability and scaling of its model in a post-hike world.

Source: Q4-Deck

A Fintech stack with integrated optionality

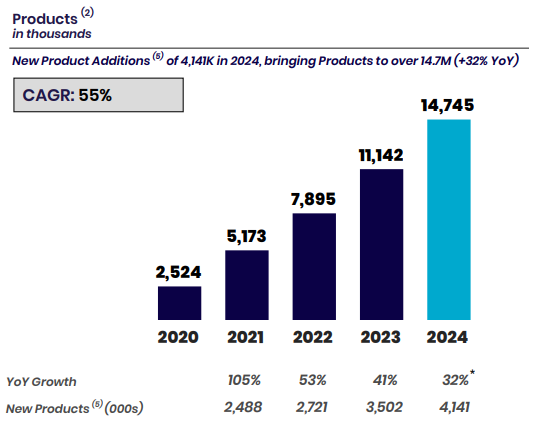

SoFi's business structure functions in three interconnected segments: Lending, Financial Services, and the Technology Platform. The central advantage of the firm is its vertically integrated model, one in which it has full-stack control from origination through servicing but with growing monetization from third-party infrastructure as well as client relations. SoFi originated a record-high $23.2 billion worth of loans in 2024, but its most interesting achievement was not the top-line volume, but rather the Loan Platform Business (LPB), a game-changer in its lending engine.

Under LPB, SoFi originates credit on behalf of institutional investors such as Fortress and Blue Owl, generating fee income while taking no balance sheet risk. In 2024, LPB powered $67 million in revenue in lending business and services, and a new deal with Blue Owl is set to drive up to $5 billion in originations by 2026. The key is that SoFi keeps the servicing rights, keeping member relationships and data within its system, reinforcing management's so-called "Financial Services Productivity Loop." This is a monetization flywheel within its ecosystem, in which a member acquired through LPB might become a direct banking, investment, or credit customer later.

The Financial Services business has evolved into a high-margin, growth engine. Net revenue grew by 84% in 2024 to a total of $257 million, with contribution margin growing from 18% to 45%. Products such as SoFi Money (+51% YoY), Relay, and Invest are not merely growing, they are better monetizing. Financial Services revenue per product grew 37% year-over-year to $81. There is further margin upside, management believes, as cohort behavior has shown cross-product adoption is gaining momentum. During Q4, 40% of new members acquired a second product within 30 days, up from previous cohorts.

In the meantime, the Technology Platform, anchored by Technisys and Galileo, is maturing from a developer toolset to a full enterprise solution. With 168 million (+15% YoY) accounts, the platform drives embedded finance for fintechs, banks, and, most recently, government partners. The arrangement with the U.S. Treasury's Direct Express program, the largest federal benefit card program, not only adds credibility but unlocks recurring B2B revenue based on real-scale deployments. Recent signings, such as a top 10 revenue client in 2026, predict both wallet growth and verticals-specific market share gains.

Source: Q4-Deck

Breaking Away from the Pack

The fintech landscape is famously cut-throat, but no one else approaches SoFi in terms of breadth and vertical integration. Chime, for example, has banking-like services but no lending or back-end tech stack. Block's Cash App has payment rails as well as minimal investing, but it is aligned with transaction-based swings as well as no funding through deposits. And traditional banks are saddled with compliance overhead, siloed tech, and infrastructure decades in the making, which can no longer iterate rapidly.

Where SoFi has an advantage is through its ownership of both the consumer pipeline as well as the infrastructure layer. The technology-driven nature of the company enables it to deliver new features, such as robo-advising with BlackRock, alternative investing through SpaceX-related funds, and subscription-based SoFi Plus, with speed. The competitors, in contrast, usually outsource the core stack or are single-product platforms open to commoditization.

AI, unglitzy though it is, is quietly woven throughout SoFi's underwriting, fraud prevention, and member servicing. Its more lasting distinction, however, is in behavioral data. All activity in lending, investing, and payments feeds into a single data graph, one that drives personalization, retention, and risk segmentation. The foundation for predictive product suggestions and ultimately AI-native financial advisors driving wallet share with no incremental headcount.

The customer acquisition cost (CAC) is also structurally decreasing. SoFi's flywheel of marketing, fueled by brand partnerships such as TGL Golf and naming rights, generates awareness, while product cross-selling increases lifetime value (LTV). In 2024, close to 30% of additional new product additions were from current members. This is no linear DTC pipeline, it's a looped system with inbuilt retention levers, a feat in the financial industry.

Source: Q4-Deck

Durable Growth, Capital Discipline, and Monetization Leverage

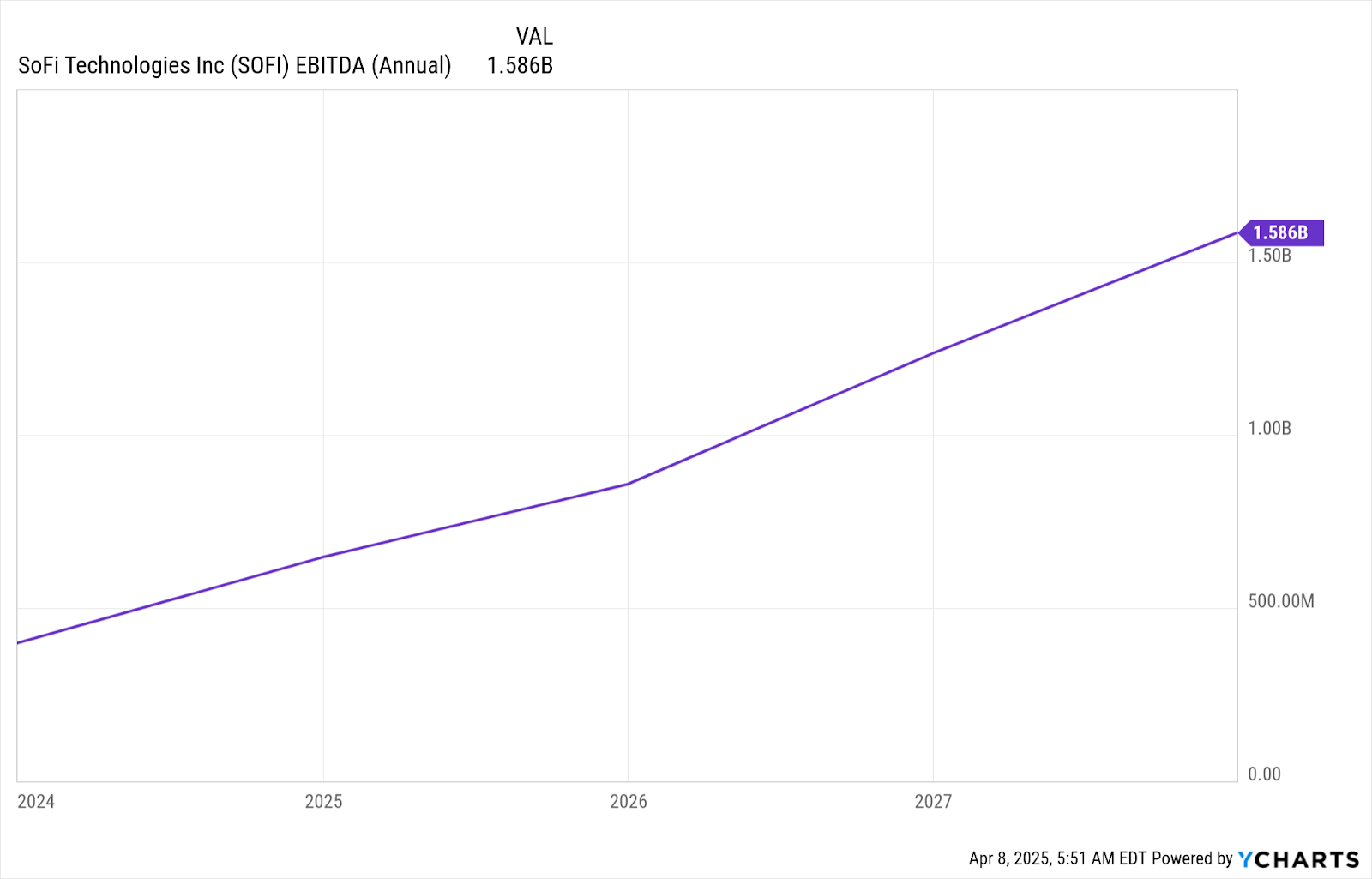

SoFi's results uphold the platform leverage thesis. Adjusted net revenue in FY2024 was $2.6 billion (+26% year-over-year) with a corresponding adjusted EBITDA of $666 million, as well as GAAP net income of $499 million. Without considering extraordinary tax credits, this was the firm's first full year of GAAP profitability, a benchmark many fintechs are yet to come close to. Non-lending segments, consisting of Financial Services and Tech Platform, generated close to half of the revenue and expanded at a 54% YoY, driving the business mix towards more capital-light, recurring revenue. Lending, though strong, is now a high-yield funnel instead of a single revenue pillar.

Margins are widening with size. Adjusted EBITDA margin reached 26% in 2024, from 21% in 2023. Financial Services’ contribution margin was up at 45%, while Tech Platform was unchanged at 31%. Net interest margin (NIM) in the book is also strong at 5.91%, taking advantage of the firm’s deposit funding strength, up at $26 billion. The spread between cost of funding by deposits vs. warehouse lines (193 basis points) equates to ~$500 million in annualized savings, insulating margins in diverse rate regimes.

Importantly, credit quality remains strong. Weighted average FICO scores for personal loans are 744, with net cumulative losses tracking below 4%, far beneath the 8% underwriting tolerance. Delinquencies and charge-offs declined sequentially in Q4, and SoFi has actively sold late-stage delinquents to manage exposure. This signals prudent risk management amid macro uncertainty.

On the expense side, SoFi has kept costs efficient while growing. OpEx as a portion of revenue declines, while CapEx is disciplined. Monetization per product increases, as does member engagement, such that the business has strong operating leverage. The business looks to achieve a 30% incremental EBITDA margin in 2025, investing selectively in product development as well as client acquisition.

Source: Ycharts

Valuation: Expansion Multiples vs. Skepticism Over

SoFi is still a high-growth fintech stock that's obviously priced for future growth versus existing profitability. Its non-GAAP forward P/E was 36, almost 278% above the industry median of 9.49, while the GAAP forward P/E is also bloated at 37.46. These multiples are indicative of optimism surrounding SoFi's evolution from a lending-focused model to a platform-based, fee-driven fintech environment. With Q4 revenue growing 24% year-over-year and membership gains of over 8.1 million, the market is seemingly willing to pay premium for the long-term potential. But without any form of historical five-year P/E average and earnings still playing catch-up, we've got a sentiment-driven gamble versus a value proposition here.

Analyzing sales-based multiples, SoFi's FWD price-to-sales of 3.29 is 38% ahead of the industry median, and 1.61 price-to-book is approximately 47% higher. Note how that P/B multiple is approximately 95% lower than the five-year average of 29.62, which shows how far the stock has compressed off of its original SPAC-driven highs. Although that implies a more reasonable valuation relative to past multiples, it still trades well ahead of usual financial peers. What we are waiting for is whether SoFi will increase margins and bring in revenue on those users quickly enough to grow into these lofty multiples. If the management gets it done, especially by growing that tech platform and cross-selling financial products, the premium can be justified. But for now, it assumes near-flawless execution, something we'll be watching closely.

Navigating Uncertainty: Regulatory, Credit, and Competitive Risk

Even with strong performance, SoFi is not risk-free. There are regulatory risks lurking in fintech banking, notably around fee disclosure and data protection. In 2024, it was hit with a fine of $1.1 million for brokerage infractions, a sizable but manageable fine but a testament to the compliance burden attached to its diversified business.

In addition, while LPB and securitizations expose the firm's balance sheet, its borrowing carries interest rate sensitivity. A later-than-expected Fed pivot or a period of new credit stress would weigh on origination volumes and funding spreads. Nonetheless, the firm's balance sheet, with a 16.2% capital ratio and tangible book value of $4.9 billion, presents a strong degree of resiliency.

Competition is also growing fierce. Apple, Google, and PayPal are further accelerating their charge into financial ecosystems, but few are as integrated as SoFi. Embedded finance upstart competitors such as Synapse, or Unit don’t bring consumer scale. SoFi's task is maintaining a lead in pace of innovation rather than diluting product sophistication.

Source: Market Data Forecast

Conclusion

SoFi's evolution from student loan originator to a thriving, diversified financial platform is perhaps the least credited story in fintech. Having passed the profitability Rubicon, achieved multi-segmented monetization, and created a brand that speaks to digitally native generations, the firm has a brand, business, and economics that are likely poised for a seismic shift. Though the marketplace is preoccupied with interest rate cycles, the true signal is in SoFi's shifting business mix, improving margin profile, and widening data moat. Expanding fee-based revenue, along with anchored B2B wins in scale in 2026, may not merely keep SoFi afloat during fintech's growing pains, but instead set the next template for a digital financial operating system.

Recommended Articles