Lululemon (LULU): Great Brand Value at Huge Discount

Source: TradingView

Investment Thesis

Lululemon is a well-run company, avoiding the strategic mistakes of peers like Adidas and Nike. The company is in its early stages of brand expansion and we expect to see more growth from overseas and from men’s wear. According to our estimates, the margins will take a significant hit in the coming months but even with this into account, the valuation seems quite attractive as the PE ratio is way below the historical average.

Company Business Model

Lululemon is a clothing company that designs, markets and sells high-end athletic apparel, footwear and accessories mostly used for yoga, running and training. The brand’s most recognizable products are their yoga pants and leggings which are extremely popular among women living in the large metropolitan areas all over the world.

How does Lululemon market itself as a brand?

The Lululemon approach differs quite a lot from sports apparel giants like Nike and Adidas.

Lululemon started as a yoga brand and yoga lifestyle still remains a centerpiece of its image. Unlike other sports brands that aim to collaborate with famous athletes, Lululemon marketed itself as a lifestyle brand with a focus on yoga and wellness. The company often collaborates with yoga and wellness practitioners and organizes such events in its stores.

Lululemon sticks to its core specialties. Unlike the larger peers that aim to produce different kinds of items and cater to as big a customer base as possible, Lululemon does not sell a huge variety of items and the customer base is mostly a rather small (compared to what Nike has) community of urban professionals. This helps them 1) keep a certain level of brand exclusivity, allowing for premium pricing; and 2) establish a stronger bond with customers, creating customer stickiness.

Lululemon puts a strong emphasis on product design. Instead of producing many items, they focus on fewer items. Their flagship product, leggings, is undoubtedly the best on the market with high quality fabrics, simple/neutral colors and design that enhance the body’s natural shape.

How does the supply chain look like?

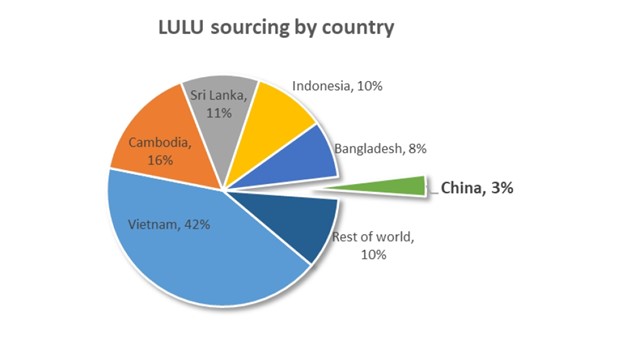

Lululemon does not have its own production facilities, but they rely on a small number of 52 vendors that are responsible for the manufacturing, five of them being responsible for half of it. Nearly eighty percent of the production comes from Vietnam, Cambodia, Sri Lanka and Indonesia, while China represents just 3%.

Source: Needham & Co

The sourcing of materials comes predominantly from Taiwan (35%), Mainland China (28%) and South Korea (11%), according to the latest annual report.

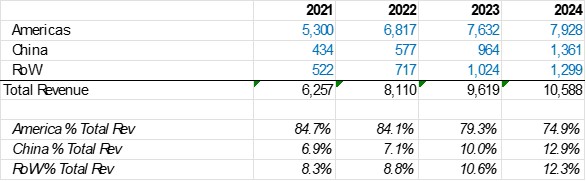

Revenue is divided into three segments based on geography – Americas (US, Canada and Mexico); China (Hong Kong and Mainland China) and Rest of the world (APAC and EMEA). Currently three quarters of the revenue comes from North America, but the China’s portion of the revenue nearly doubled in the last four years.

Source: SEC Filings, TradingKey

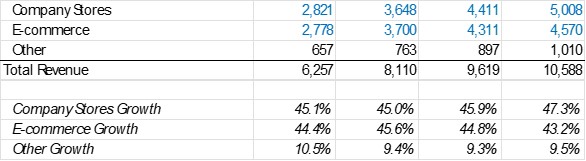

In terms of sales channels, Lululemon approach is predominantly DTC with 90% of the sales coming from either their own company stores or e-commerce website. Many may draw parallels with Nike’s DTC strategy, but we would say Lululemon has been doing significantly better. Firstly, Lululemon prioritizes the selling of an experience along with the product instead of penetrating the market (what Nike did). This allows Lulu not to be dependent on third party wholesalers like Nike does.

Source: SEC Filings, TradingKey

Secondly, Lulu also has a strong e-commerce channel (over 40% of the sales) but the e-commerce strategy complements the store sales rather than cannibalizing it. We can see from the store growth in the recent years that the company still emphasizes on physical presence.

Source: SEC Filings, TradingKey

Overall, with a small amount of manufacturers and own stores, Lululemon has a much tighter supply chain network, allowing them to have a strong grip on their product quality.

Financial Analysis and Outlook

Source: SEC Filings, TradingKey

The most recent quarterly results exceeded the expectations in terms of both revenue and EPS. We also saw improvement in the gross profit margin with 1 percentage point and inventory grew at a slower pace than revenue does. (9% increase in inventory vs 12% increase in revenue). However, the management guidance for 2025 appeared to be quite soft with EPS growth to be just 2-3% vs 14% last year – this is mostly due to decelerating top-line growth and margin headwinds from weak macro and tariffs. (The guidance is before the April tariff announcement.)

A point worth mentioning is their gross margins of around 60% - much higher than Nike’s at 40%. This makes Lulu’s gross margin closer to the luxury goods’ margins. Also, the company was able to maintain them, unlike the downtrend that we see in other sports goods.

Source: SEC Filings, TradingKey

Another positive note is the strong balance sheet with $1.984 billion in cash and zero debt.

Effects of Tariffs

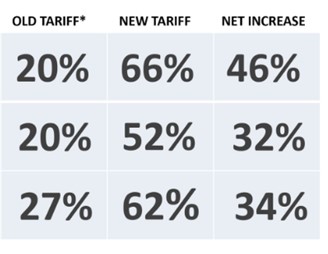

Apparel industry is one of the industries that will be affected the most from the implementation of high tariffs, due to the fact that apparel companies have largely outsourced their production to factories in Vietnam, Indonesia and China.

Source: Solerview.com

Considering the majority of products of Lululemon come from Vietnam, Cambodia, Sri Lanka and Indonesia, the weighted-average tariff increase will be around 40%.

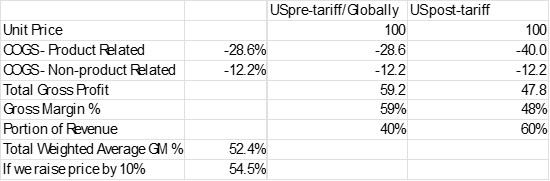

The costs of goods sold for the company in 2024 have been 40.8% of the total revenue. This implies a gross margin of 59.2%. It means the cost of a $100.00 Lululemon item is $40.80 dollars and the gross profit is $59.20. From this $40.80, $28.60 are the costs directly related to the production (raw materials, manufacturing etc.), while the rest $12.20 is related to rent, distribution centers and salaries. In the event of high tariffs, the product-related cost will go up, while the non-product related cost will stay relatively the same.

If Lulu decides not to increase prices and absorbs the full amount of the tariff, we will see a 40% increase in the Product-related portion of the COGS, which will lead to a drop in the gross profit from $59.20 to $47.80. According to last year’s financial results, 60% of the revenue comes from the US (and 40% from overseas), we calculated that the weighted average gross margin will be around 52.4%, a drop of 6.8 percentage points from what we had in 2024 – 59.2%.

Source: TradingKey

There is a possibility that Lululemon decides to raise the prices of their products. However, if this happens, we believe the price increase will not be very significant due to the fact that their items are already on the higher end of the price spectrum. If we see a jump in price of 10%, this will lead to a gross margin of roughly 54.5%, 4.7 percentage points lower than last year’s gross margin.

Also, during the supply-chain crisis of 2021 and 2022, when shipping rates soared after the pandemic, Lululemon grabbed market share as it wasn't as aggressive as its competitors with price hikes, thus we believe they may do something similar this time also.

There are a lot of uncertainties with these estimates, as it is impossible for us to predict how the tariff policies will turn and how the tariffs will be charged.

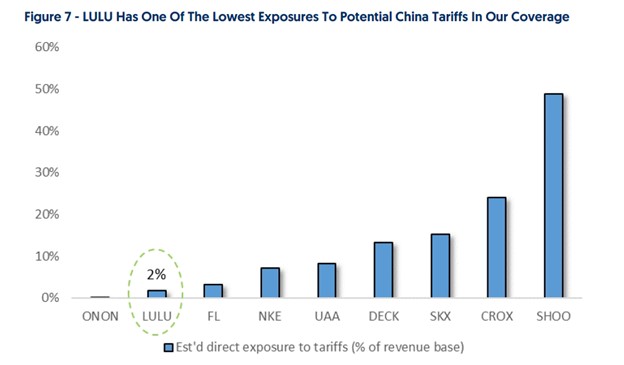

However, one positive aspect for the company is their low exposure towards Chinese manufacturers, unlike other peers. As mentioned above only 3% of the manufacturing is based in China and only 2% of the company revenue will be subjected to tariffs to China. Additionally, when it comes to Vietnam, there is a high chance of tariff negotiation towards more favorable rates.

Source: Needham & Co

Valuation

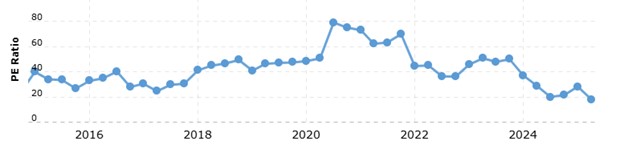

With estimated growth of mid-single digits and margin going towards 52%, we expect an EPS of $11.40 for the full year of 2025, this currently values LULU at 24 times PE, which is lower than the historical PE of the company of around 40 PE, this implies a target price of $450, a 60% upside from the current price.

Source: Macrotrends.net

Despite the slowdown in growth in the recent two years, we see several sources of tailwinds that can unfold in the coming years and make the top line rebound. Firstly, the brand is yet to be more recognized by the consumers, both domestically and internationally. Out of the 40-45 stores about to be opened, only 10-15 will be in the US and the rest globally – implying that the management will be focusing on expanding the brand internationally and improve the same-store sales in the US.

Another source of growth will be the men’s line, as the company derives just 24% of its revenue from men’s items, while the athletic apparel industry is more than 50% men’s items.

Risks to the Investment Thesis

Tariff risk remains the most significant one. Other potential factors that can impact our estimates are more intense competition, exchange rate fluctuations and excessive increase in inventory.

Conclusion

Lululemon is among the most recognizable athletic apparel brands globally. Their business strategy differs from those of Nike and Adidas, helping them achieve an exclusive brand image and strong connection with the customers. The slowdown in growth and the expected drop in margins is rather temporary and not related to the company’s execution. Even with these factors in mind, the company’s PE is below the historical average. We also see growth opportunities in the overseas markets and the men’s categories.

Recommended Articles