A Shift from Hardware to Software in the AI Industry Cycle - These AI Software Stocks Deserve Attention!

TradingKey – The rapid development of artificial intelligence (AI) technology has shifted the spotlight from proprietary models like ChatGPT to open-source alternatives like DeepSeek in just a few years. Capital markets are now pricing in a new AI cycle: the transition from the AI hardware era to the AI software era.

Whether it’s Goldman Sachs’ Four Stages of AI Trading, Bank of America’s Five Trends in AI Software, or Morgan Stanley’s alpha in AI’s rate of change, Wall Street broadly agrees that AI remains the dominant theme in technology. However, a growing consensus suggests that opportunities are shifting from hardware infrastructure to software applications.

In early 2025, Goldman Sachs noted that global capital allocation is gradually pivoting from "hard tech" to "soft tech," a trend amplified by the launch of China’s large-scale model, DeepSeek.

Overview of the AI Industry Chain

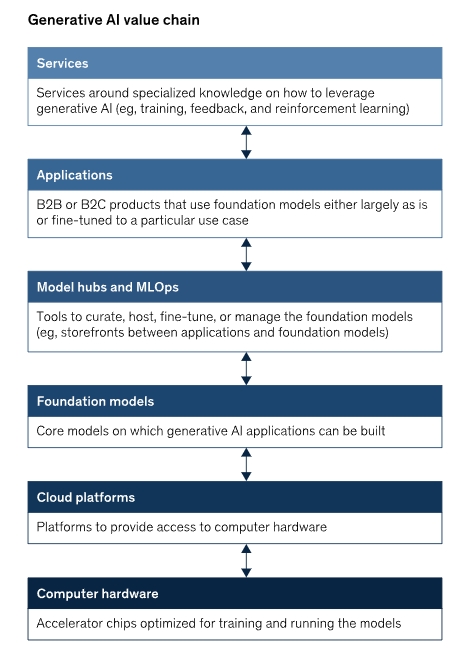

According to McKinsey, the generative AI value chain consists of six segments: computer hardware, cloud platforms, foundational models, model hubs and machine learning, applications, and services. Compared to traditional AI value chains, foundational models represent a new addition.

[Generative AI Value Chain, Source: McKinsey]

McKinsey predicts that market opportunities across these segments will expand gradually over the next three to five years. The AI applications market is expected to experience the fastest growth, presenting significant value-creation opportunities for both established tech giants and new entrants.

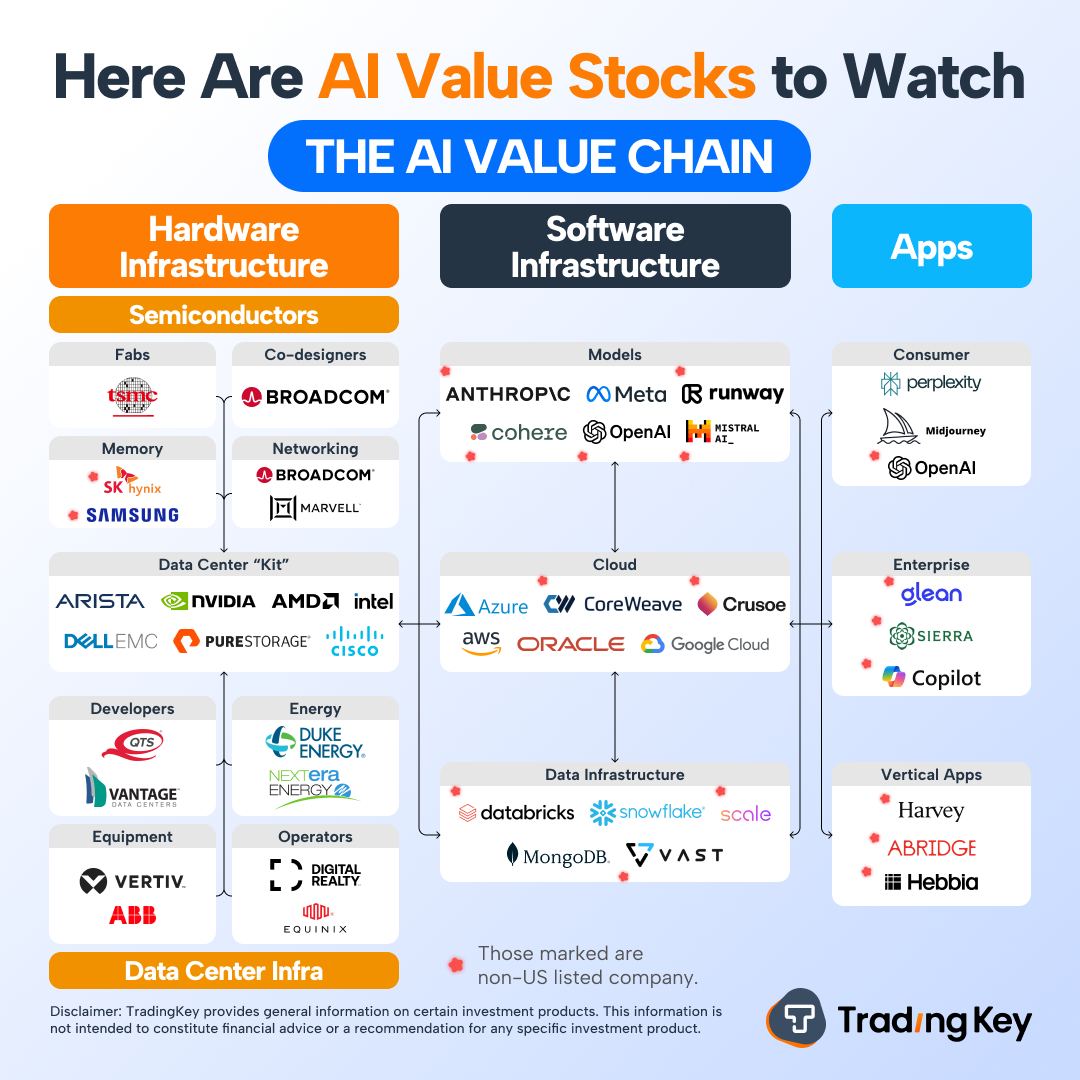

Simplified, the AI industry chain can be divided into:

- Hardware Infrastructure (e.g., NVIDIA, Broadcom, TSMC)

- Software Infrastructure (e.g., Microsoft, Google, Amazon, Meta)

- Application Services (e.g., OpenAI)

[AI Value Chain, Source: TradingKey]

Challenges for AI Hardware Stocks

According to Lu Qi, founder of MiraclePlus (formerly Y Combinator China), the launch of OpenAI’s ChatGPT marked a "paradigm shift" in AI development—from information perception systems (acquiring data from environments) to model knowledge systems (expressing information through models).

ChatGPT ignited a race for large AI models, with NVIDIA emerging as the biggest winner by supplying critical chips for model training. Its market cap once topped the U.S. stock market and remains firmly in the top three.

According to Deloitte, the semiconductor industry experienced robust growth in 2024, with sales surpassing expectations, achieving double-digit growth (of approximately 19%) and reaching $627 billion. Deloitte projects continued expansion, forecasting a record high of $697 billion in 2025, with target valuations of $1 trillion by 2030 and $2 trillion by 2040.

However, AI hardware stocks like NVIDIA face challenges due to cyclicality, slowing growth, and policy risks:

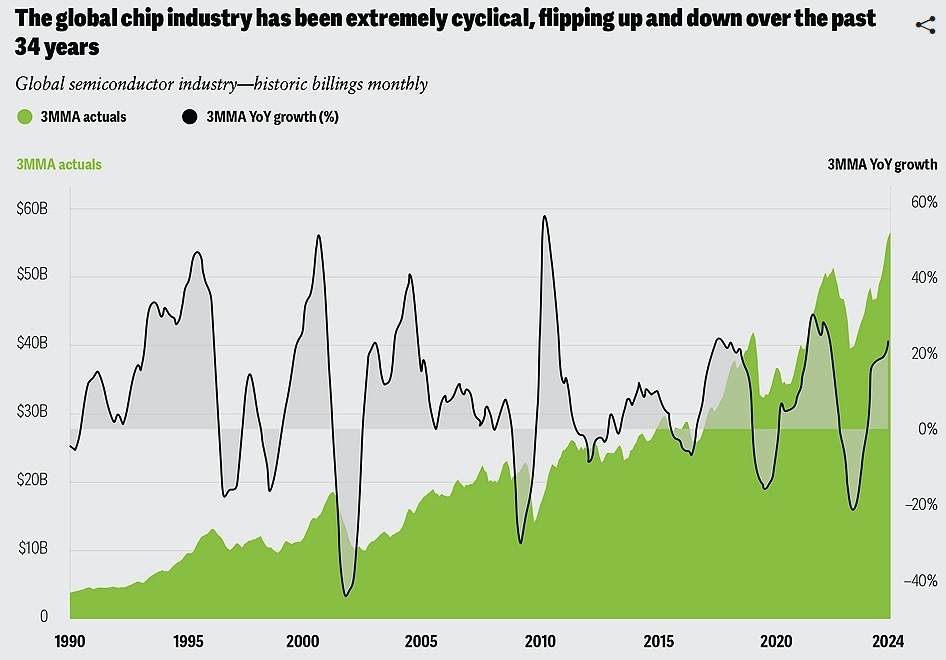

- Cyclical Volatility

Semiconductor and memory sectors exhibit strong cyclicality, driven by supply-demand dynamics. A typical semiconductor cycle spans four years (, with 2–3 years of growth followed by a 1–1.5-year downturn). Deloitte notes that the industry has undergone nine growth-to-contraction cycles over the past three decades. While the outlook for 2025 remains optimistic, uncertainties persist for 2026.

[Semiconductor Cycle, Source: Deloitte]

- NVIDIA’s Slowing Growth

NVIDIA, which controls 90% of the AI chip market, saw its revenue growth slow from triple-digit rates in 2024 to 78% by Q4 2025. Morgan Stanley notes that semiconductor growth is typically either high or negative, rarely moderate. - DeepSeek’s Shock

China’s DeepSeek model is challenging existinghardware and software "moats" with its open-source, low-cost, low-hardware-requirement, high-performance approach. Analysts argue, "We don’t need more NVIDIA chips; we need applications." - Export Restrictions and Tariffs

Meanwhile, U.S. export controls on advanced chips to China, Russia, and Israel— along with the potential for stricter measures under a Trump 2.0 administration—pose risks toNVIDIA ( which derives 50% of its revenue from overseas, with 20% from China) and Broadcom.

Opportunities for AI Software Stocks

As NVIDIA’s hardware boom cools, Wall Street is turning bullish on software in 2025. Wedbush notes, "The AI software era has arrived."

Bank of America identifies five trends driving software growth:

- Enterprise AI adoption for productivity

- Enhanced AI monetization by software firms

- AI spending displacing lower-priority IT projects

- Rise of autonomous AI and small language models

- Low/no-code application proliferation

Goldman Sachs outlines four phases of AI trading:

- Chip leaders (e.g., NVIDIA)

- AI Infrastructure

- AI-enabled revenue

- AI-productivity gains

By 2025, Goldman sees Stages 1–2 under pressure, while Stage 3 (24 software firms among its 40 picks, including Palantir and Cloudflare) offers growth.

Key Drivers for Software Stocks

- Dual Cycles: Overlapping software spending and generative AI innovation cycles.

- AI Applications as the Endgame: Capital naturally flows to software, where AI use cases materialize.

- DeepSeek Democratizes AI: Open-source models lower adoption barriers, benefiting application and platform layers.

- AI Agents: Autonomous AI models (e.g., for customer service, biotech, and education) could revolutionize labor-intensive sectors. Gartner predicts that 33% of enterprise software will integrate AI agents by 2028.

Top U.S. AI Software Stocks to Watch

- Cloud Services:

- Microsoft (MSFT): Azure’s dominance in AI model development.

- Amazon (AMZN): AWS’s infrastructure and diverse AI use cases.

- Google (GOOG): Google Cloud’s expanding AI ecosystem.

- Salesforce (CRM): CRM leader with strong AI integration.

- Data Companies:

- Palantir (PLTR): Shifting from government to commercial AI.

- Snowflake (SNOW): Steady growth in data solutions.

- AI Applications:

- Home Depot (HD) and Spotify (SPOT): High pricing power in AI adoption.

- Financial Firms:

- Evercore (EVR), MSCI (MSCI), Fiserv (FI), Toast (TOST): Leveraging AI for efficiency and risk management.

Recommended Articles