[IN-DEPTH ANALYSIS] PayPal's Stagnant Stock: Is $97 the Breakout Price for 2025?

Source: TradingView

Key Takeaways

Overview: PayPal leads digital payments, connecting 400M+ users across 200+ markets with secure e-commerce and P2P solutions.

Positioning: Trusted brand with 434M users, 90M on Venmo, driving $1.68T TPV with strong cross-border reach.

Competition: Faces threats from Apple Pay, Google Pay, Stripe, Alipay, Visa, MasterCard, and emerging BNPL/crypto players.

Future Growth: Boosted by e-commerce, mobile payments, emerging markets, and innovations like Fastlane.

Financials: Rising TPV Per Active, Transactions Per Active, Margin at 47%, Take Rate at 1.91%, with strong cash flow and ROE.

2025 Target: $87-$97, recommended $92, fueled by 20% EPS growth and high-margin business.

1. Company Overview

TradingKey - PayPal is a leading digital payment platform that acts as an intermediary in the payment process, connecting merchants and consumers. It allows consumers and merchants to conduct online transactions and provides secure and convenient payment solutions to ensure safe and efficient transactions. PayPal serves over 400 million users across more than 200 markets, focusing on e-commerce and P2P businesses.

The workflow of PayPal can be simply viewed as PayPal acting as a payment gateway and processor, directly managing user accounts and transactions. It deducts funds from the user's account (bank account, credit card, or PayPal balance) and transfers them to the merchant.

2. Industry Positioning

Key Advantages

- Brand Recognition and Trust

PayPal enjoys high brand recognition in Western markets, particularly in the United States, the United Kingdom, and Germany. According to Statista’s in-depth report on Fintech, PayPal’s usage rate ranges from 75% to 90%, with 60% of consumers trusting PayPal more than banks to store payment information. This trust stems from PayPal's long-standing reliability and its buyer protection policies, which give it a significant advantage in the security-sensitive payments market.

Source: Statista

- User Base and Network Effects

PayPal has 434 million active users, including 90 million Venmo users, creating a strong network effect. In 2024, the average number of transactions per account was 61.3, representing a 4.4% year-over-year growth, highlighting strong user engagement. This bilateral network effect (where more users attract more merchants) further solidifies PayPal's market position.

- Global Coverage and Cross-Border Payments

PayPal operates in over 200 markets and supports 25 major currencies. In 2024, its total payment volume (TPV) reached $1.68 trillion, marking a 10% year-over-year growth. PayPal’s cross-border payment capabilities provide a unique advantage in the global e-commerce space, enabling seamless transactions across borders.

Competitive Landscape

As the leader in the global digital payments market, PayPal faces intense competition from various players across different sectors.

1. Digital Wallets

- Competitors: Apple Pay, Google Pay, Stripe, Block

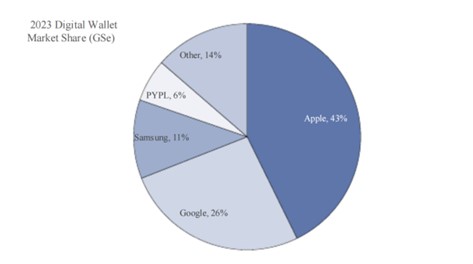

On the consumer side, Apple Pay and Google Pay leverage deep integration with smartphones and their device ecosystems (e.g., iPhone and Android) to lock in users and offer a seamless payment experience. In comparison, PayPal requires an additional login step, which adds friction to the process. As a result, Apple Pay and Google Pay have experienced rapid growth in mobile payments in recent years. According to Goldman Sachs' 2025 Payments Industry Outlook, Apple Pay and Google Pay will collectively hold nearly 70% of the mobile wallet payment market share, directly threatening PayPal's Branded Checkout business, especially in terms of mobile user experience, and this could reduce PayPal’s mobile transaction volume.

Source: Company data, Goldman Sachs Global Investment Research, eMarketer

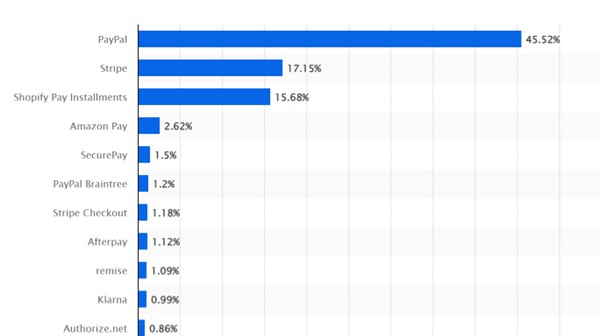

On the merchant side, Stripe and Block focus on providing low-cost, easy-to-integrate payment solutions for small and medium-sized businesses, capturing PayPal’s merchant base. Stripe attracts tech companies with its API and developer-friendly tools, while Block expands its offline market with hardware solutions such as POS terminals. In comparison, PayPal’s innovations, like FastLane, are still in the early stages of rollout and have limited coverage. According to the data on the most used payment processing technology by the end of January 2025, Stripe's market share reached 17.15%, second only to PayPal’s 45.5%. Stripe and Block may divert PayPal’s small business clients, potentially shrinking its merchant revenue and slowing FastLane adoption.

Source: Statista

2. Regional Competitors

- Competitor: Alipay

According to Statista, PayPal is the most popular online payment brand in markets such as Germany, the UK, and the US, with usage rates ranging from 75% to 90%. However, the situation is entirely different in Mainland China, where Alipay, WeChat Pay, and UnionPay dominate with usage rates of 92%, 84%, and 42%, respectively. Alipay holds a dominant position in China and Asia, serving over 1.3 billion users. Its localized strategies, such as integration with WeChat Pay, have made it difficult for PayPal to penetrate the Asian market. Additionally, the Chinese government's support for local payment platforms (e.g., regulatory restrictions on foreign companies) has weakened PayPal's competitiveness. Alipay’s global user base far exceeds PayPal’s 434 million, particularly in cross-border e-commerce. Alipay’s dominance limits PayPal’s growth in Asia, reducing its share of the lucrative cross-border e-commerce market and overall global TPV.

Source: Statista

3. Traditional Payment Networks

- Competitors: Visa, MasterCard

Visa and MasterCard are expected to engage in fierce competition with PayPal in the digital payments and real-time transfer space. For example, Visa’s Visa Direct and MasterCard’s MasterCard Send services enable fast point-to-point (P2P) payments and business-to-consumer (B2C) payments, directly challenging PayPal’s Venmo and Branded Checkout offerings, decreasing PayPal’s P2P and B2C transaction volumes and related revenue.

4. Emerging Trends

- Competitors: Klarna, Affirm, Coinbase, Block

According to Thomson Reuters, BNPL services like Klarna and Affirm are rapidly capturing the younger market by offering flexible payment options and low entry barriers, pushing the global BNPL market to an estimated $116 billion by 2025. While PayPal's Pay in 4 service has made progress, its awareness remains low, and further marketing efforts are needed to improve its competitiveness. Meanwhile, Bitcoin payment solutions from platforms like Coinbase and Block challenge traditional payments with innovative approaches. PayPal’s cryptocurrency services, launched in 2020, have yet to be fully monetized, requiring faster innovation to compete with specialized platforms.

Klarna and Affirm may outpace PayPal in BNPL adoption, while Coinbase and Block could hinder its crypto service revenue growth, pressuring PayPal to accelerate innovation and marketing.

3. Why Is PayPal’s Stock Struggling?

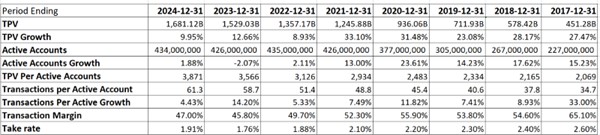

PayPal's stock has been stagnant since 2022, with nearly three years of no significant movement. The primary reason, in my opinion, is that the market began pricing in a slowdown in PayPal’s key metrics starting in 2021. Looking at the trends in PayPal's key data, the market's assessment appears to be accurate.

TPV growth has slowed from nearly 30% to less than 10%, and active accounts growth has significantly decelerated, with almost no growth or even negative growth in some periods. This has led to a sharp slowdown in revenue growth and gross margin over the past few years, while net income growth has stagnated, and in some cases, even turned negative.

Source: TradingKey, Paypal

Source: TradingKey, Paypal

4. Can PayPal Make a Comeback in the Future?

E-commerce Growth

The rapid growth of global e-commerce and digital payments is providing strong momentum for PayPal's Total Payment Volume. According to Statista, global e-commerce sales are expected to reach $8 trillion by 2027, growing at a CAGR of 11%. The expansion of the e-commerce market will directly drive the growth of PayPal's TPV.

Expansion in Emerging Markets

According to the World Bank, around 1.3 billion people globally still do not have access to bank accounts, primarily in Asia, Africa, and Latin America. PayPal has a relatively low penetration in these emerging markets, but the digital transformation in these regions, coupled with the unbanked population, presents a huge growth opportunity for PayPal. Through localized payment solutions and partnerships with regional e-commerce platforms, such as Flipkart in India and Jumia in Africa, PayPal can significantly boost its global user base and TPV.

Innovative Products

PayPal is significantly expanding its revenue streams and enhancing its market competitiveness through innovative products such as Fastlane, Buy Now Pay Later (BNPL), and cryptocurrency services. Fastlane’s rapid checkout feature has already increased conversion rates by 30% (Reportlinker). The BNPL service is expected to account for 10% of Total Payment Volume (TPV) by 2027 (Goldman Sachs 2025 Americas Payments Outlook), while cryptocurrency transactions grew by 15% in 2024 (PayPal Q4 2024 Earnings). These innovations meet consumer demand for convenience and digital assets, driving future growth for PayPal.

Financials May Have Bottomed, Valuation Appears Reasonable

Although PayPal's TPV Growth and Active Accounts Growth have slowed, TPV Per Active Account, Transactions Per Active Account, Transaction Margin, and Take Rate show signs of stabilization and recovery, reflecting PayPal's success in enhancing user value and profitability by focusing on high-value users and high-margin businesses (e.g., driven by Venmo and Fastlane). Consequently, while PayPal's Gross Margin growth has moderated, its Operating Margin and Profit Margin remain stable, demonstrating resilient operational performance.

PayPal's Free Cash Flow Margin has steadily risen to 21.29%, highlighting its strong cash generation capabilities; the Quick Ratio, consistently between 1.17 and 1.40, ensures liquidity and debt repayment capacity; Return on Equity (ROE) has increased from 11.80% to 20.30%, reflecting improved capital efficiency; and Buyback Yield has shifted from -0.25% to a positive 6.14%, signaling the company's belief that its stock is undervalued and its efforts to enhance per-share value through repurchasing shares. The current PE Ratio has dropped from a historical peak of 65.3 to around 17, suggesting a more reasonable valuation.

PayPal's reasonable target price for 2025 is estimated at $87-$97, with a recommended value of $92, based on a 2025 EPS of $4.84 and a PE ratio of 18-20. The upside potential is driven by improved profitability (EPS growth of 20%), a focus on high-margin businesses (Transaction Margin at 47.00%), increased user value, and financial stability, though investors should remain cautious of intensifying competition and market saturation risks.

Recommended Articles