[IN-DEPTH ANALYSIS] Japan: Why Will Stocks and Currency Rise Despite "Reciprocal Tariffs"?

Executive Summary

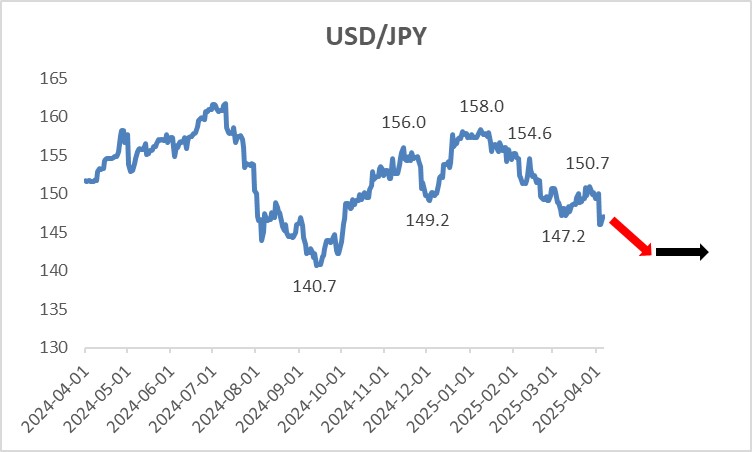

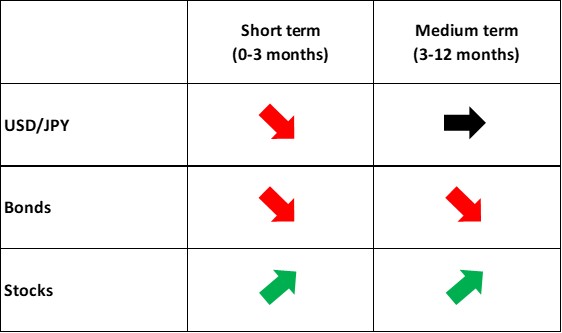

Foreign Exchange Perspective: On the yen side, in the short term (0-3 months), the Bank of Japan’s (BoJ) rate-hiking cycle is expected to drive up Japanese government bond (JGB) yields, thereby boosting the yen’s exchange rate. Additionally, the narrowing policy rate differential between the U.S. and Japan further supports the yen. However, over the medium term (3-12 months), as the U.S. and global economies are projected to slow but not slip into recession, a sustained yen appreciation appears unlikely. On the dollar side, we anticipate the USD Index will decline initially before rebounding. Consequently, we expect the yen to strengthen against the dollar in the short term and stabilize in the medium term.

Stock Market Perspective: For Japanese equities, the current U.S. "Reciprocal Tariffs" concerns may have already been fully priced in. Even if future tariffs exceed expectations, their impact on Japanese stocks is likely to remain limited. These, together with Japan’s ongoing economic recovery, underpin our optimistic outlook for Japanese equities. Notably, while Japanese stocks and the yen historically exhibited an inverse relationship, recent shifts in Japan’s monetary policy, stock valuations and the yen’s characteristics suggest this dynamic may flip in the short term, potentially turning the stock-yen correlation positive.

Source: Refinitiv, Tradingkey.com

Source: Refinitiv, Tradingkey.com

* Investors can directly or indirectly invest in the foreign exchange market, bond market and stock market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. U.S. "Reciprocal Tariffs" on Japan

On 2 April 2025, the U.S. government announced an executive order imposing "reciprocal tariffs" on several trading partners, including Japan. Specifically, the United States has set a tariff rate of 24% on Japanese goods. The U.S. claims this rate mirrors the combined impact of tariffs and non-tariff barriers imposed by Japan on American products. Japan has responded strongly to this measure. Japanese Prime Minister Shigeru Ishiba described it as a "national crisis" and vowed that the government would do its utmost to mitigate the effects. Chief Cabinet Secretary Yoshimasa Hayashi expressed regret over the decision and emphasized that Japan would continue engaging with the U.S. to seek tariff exemptions or adjustments.

2. Macroeconomics

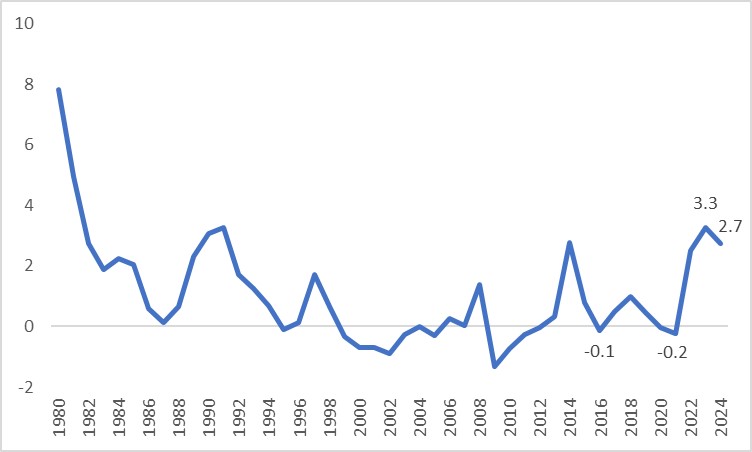

Japan’s economy endured decades of deflation until recent years ushered in a long-awaited period of “benign inflation” (Figure 2.1). This shift stems from four factors:

- Abenomics’ Three Arrows—loose monetary policy, flexible fiscal policy and structural reforms—have sustained demand-side inflationary pressure.

- Fundamental changes in household consumption and corporate investment behaviour have enabled firms to pass rising costs onto consumers.

- A saturated non-regular employment market has prompted regular employees to demand wage hikes, fostering a virtuous wage-inflation cycle.

- The yen’s depreciation over recent years, combined with post-pandemic global oil price surges, has fuelled imported inflation.

Figure 2.1: Japan's long-term CPI (%)

Source: Refinitiv, Tradingkey.com

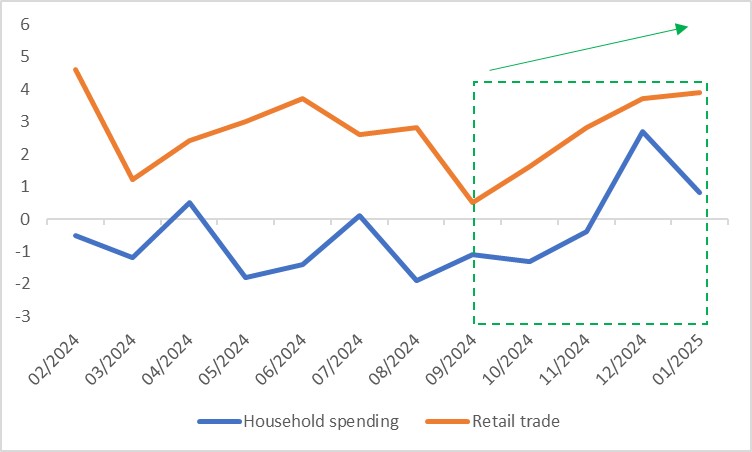

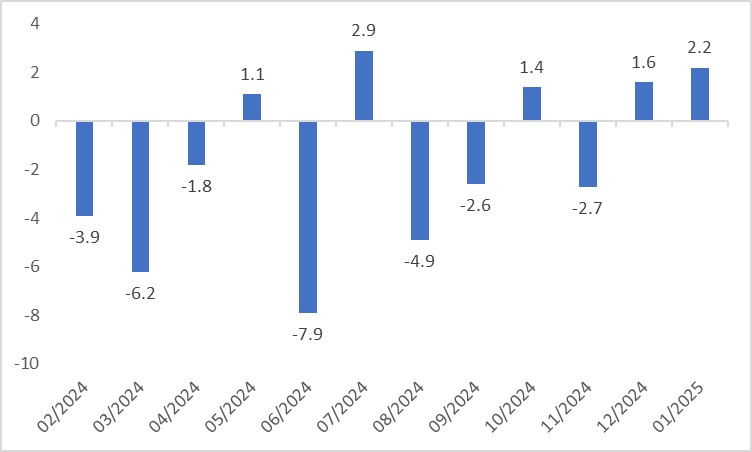

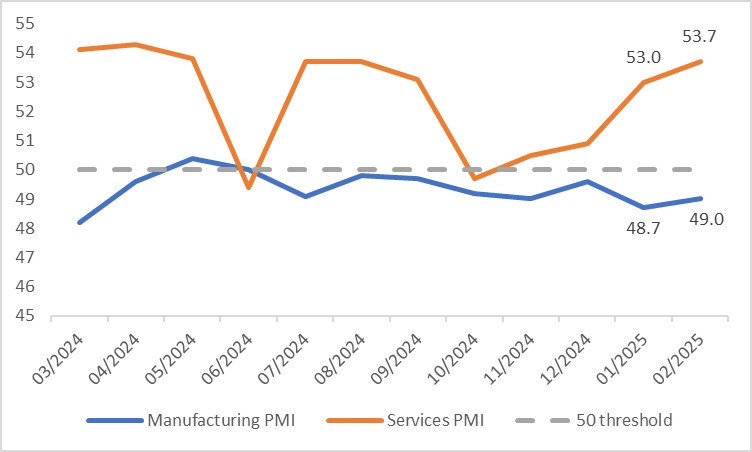

As the economic adage goes, “High inflation isn’t ideal, but deflation is worse.” Prolonged deflation dimmed Japan’s economic prospects for years, but as reflation takes hold, signs of recovery are emerging. Despite negative GDP growth in the first half of last year, Japan’s ultra-low interest rates—far below those of other developed economies—have supported a rebound since mid-2024. Real GDP has turned positive (Figure 2.2) and high-frequency data reflect warming trends. On the consumption side, household spending, after four consecutive months of decline, returned to growth in December 2024. Retail trade growth has risen for four straight months since bottoming in September 2024 (Figure 2.3). Additionally, the “Shunto” indicates slightly stronger wage growth, fuelling a positive wage-consumption spiral that supports economic expansion. On the production side, industrial production is recovering (Figure 2.4). Although the Manufacturing PMI remains below the 50 threshold, February’s reading improved from January. Meanwhile, the services sector, accounting for roughly 70% of the economy, shows robust growth (Figure 2.5).

Figure 2.2: Japan's real GDP growth (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Figure 2.3: Japan household spending and retail trade (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Figure 2.4: Japan industrial production (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Figure 2.5: Japan PMI

Source: Refinitiv, Tradingkey.com

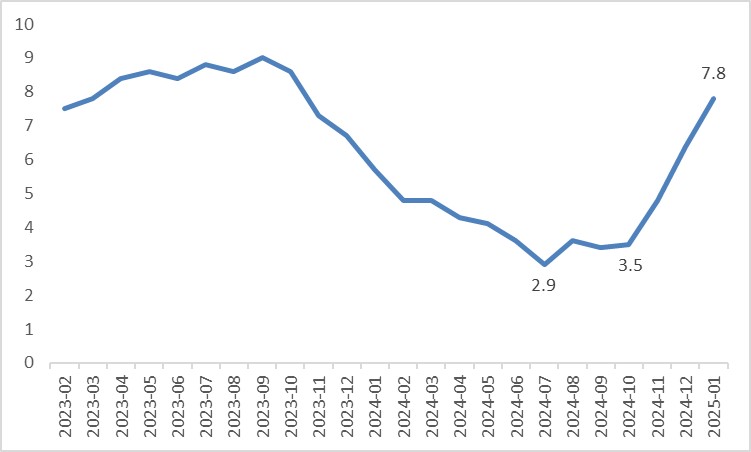

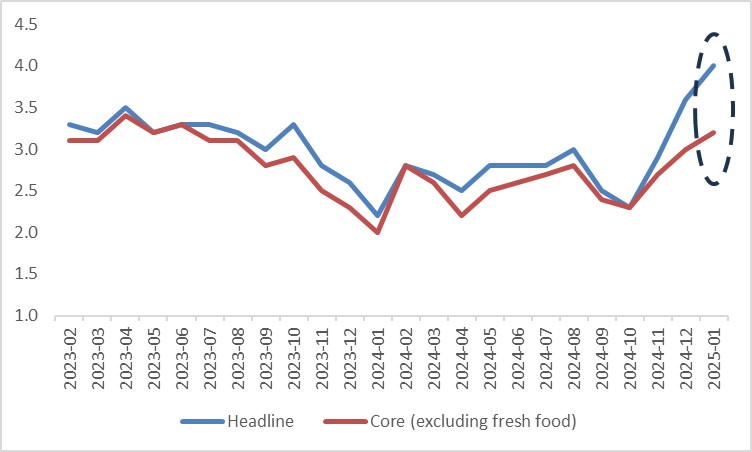

Inflation Dynamics: Rising food prices (Figure 2.6)—particularly rice—and persistent labour market tightness have driven both headline CPI and core CPI (excluding fresh food) to rebound from lows (Figure 2.7). A warming economy, climbing inflation and the wage-inflation spiral from “Shunto” reinforce the BoJ’s rate-hiking trajectory. However, external factors will cap the BoJ’s ability to raise rates aggressively. Following the U.S. tariff policy implementation on 2 April, any tariffs imposed on Japan will directly hinder its growth. Even if direct tariff impacts are limited, a broader trade war’s dampening effect on global growth will indirectly weigh on Japan’s export-driven economy. Retaliatory measures from trading partners are also expected to slow U.S. growth further, prompting the Federal Reserve to restart its rate-cutting cycle—potentially exceeding current market expectations. This, in turn, will temper the BoJ’s monetary policy normalization. Overall, we forecast one BoJ rate hike of 25 basis points by year-end—below market expectations of two hikes.

Figure 2.6: Japan food CPI (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Figure 2.7: Japan CPI (y-o-y, %)

Source: Refinitiv, Tradingkey.com

3. Exchange Rate (USD/JPY)

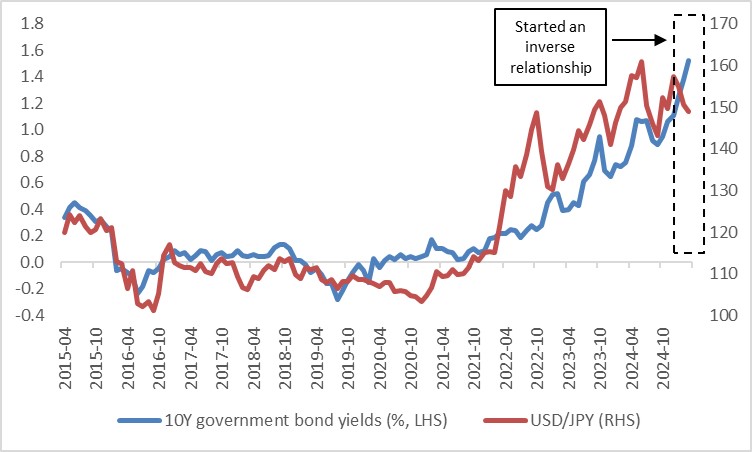

Despite our projection of a milder BoJ rate-hiking pace than markets anticipate, the broader trend of monetary policy normalization should keep JGB yields rising. Theoretically, higher yields attract foreign capital, boost inflows, improve economic expectations and shift risk appetites, all supporting yen appreciation. Yet, over the past decade, JGB yields and the yen’s exchange rate have shown little correlation—sometimes even moving counter to theory—due to the BoJ’s prolonged negative interest rate policy, which left the yen more sensitive to Fed policy and global economic conditions.

Since this year, however, the BoJ has ended negative rates, lifting its policy rate to 0.5%. This shift has restored theoretical dynamics to Japan’s markets, with elevated JGB yields now driving yen strength (Figure 3.1). Looking ahead, in the short term (0-3 months), rising JGB yields, combined with widespread rate cuts by other global central banks, should further bolster the yen.

Figure 3.1: Japan government bond yields and USD/JPY

Source: Refinitiv, Tradingkey.com

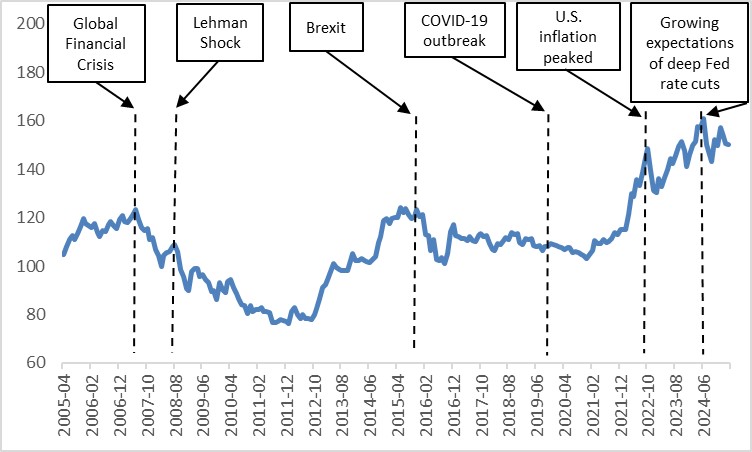

Can the yen sustain significant gains over the medium term (3-12 months)? Historically, sharp yen appreciation against the dollar required: 1) a U.S. recession; or 2) a steep drop in U.S. inflation; or 3) deep Fed rate cuts—each triggering dollar weakness—or 4) a global crisis amplifying the yen’s safe-haven appeal (Figure 3.2). Looking forward, with the U.S. and global economies expected to slow but avoid recession, these conditions are unlikely to materialize. Thus, sustained yen appreciation seems improbable.

Figure 3.2: External factors caused the yen to sharply appreciate

Source: Refinitiv, Tradingkey.com

We also expect the USD Index to dip before rising (see “[IN-DEPTH ANALYSIS] Trump Policies: Market Overreacted, Remain Bullish on Stocks, published March 17, 2025”). In the short term, U.S. economic softness and a Fed rate-cutting cycle will pressure the dollar downward, aiding yen appreciation. Over the medium term, a dimmer U.S. outlook and Europe’s sluggish recovery will weaken global growth, enhancing the safe-haven appeal of both the dollar and yen. Consequently, the yen-dollar rate should stabilize within a range, with little room for further upside.

4. Bonds

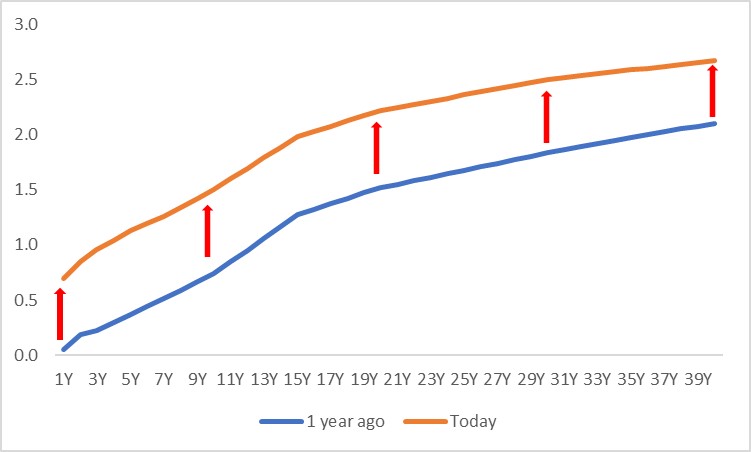

Beyond the BoJ’s rate hikes lifting JGB yields (as noted in the Exchange Rate section), Japan’s economic recovery will also influence bonds. Historically, JGBs enjoyed a decades-long bull market with declining yields. However, from June 2003 to August 2004, economic recovery expectations triggered a stock-bond seesaw, with both equities and JGB yields rising. In this recovery cycle, we expect a similar pattern: risk appetite will drive funds into equities, pushing JGB prices down and yields up.

Regarding duration, policy rate hikes primarily lift short-end yields, while economic recovery boosts long-end yields. With both drivers exerting balanced force, we anticipate a parallel upward shift in the JGB yield curve, unlikely to steepen or flatten significantly (Figure 4).

Figure 4: Japan government bond yield curve (%)

Source: Refinitiv, Tradingkey.com

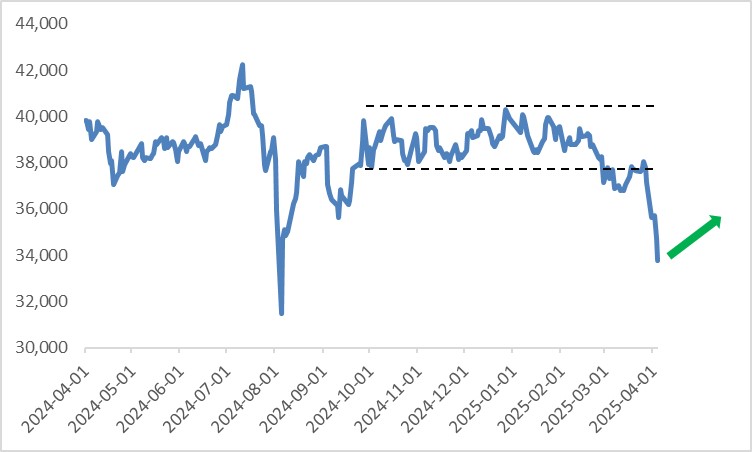

5. Stocks

Since October last year, Japanese equities have traded in a range, but a downward trend emerged in February due to Trump’s foreign policy, U.S. economic slowdown spillovers, declines in Japan’s U.S.-linked tech stocks and the BoJ’s rate hikes. The most significant factor is Trump’s tariff measures. Japanese Foreign Ministry and METI officials recently visited the U.S. to negotiate tariff exemptions, but given America’s hardline stance, Japan is unlikely to avoid tariffs on autos. Economically, auto exports to the U.S. account for 35.5% of Japan’s total exports to the U.S. and 1.2% of GDP. In the stock market, Japanese automakers have underperformed the Nikkei 225 by around 20% over the past year amid tariff fears. While tariffs would dent both the economy and equities, recent stock declines may have already priced in this risk. Once negative news is exhausted, a rebound is likely. Moreover, Japan’s trade surplus with the U.S. is modest and tariff gaps are small. Therefore, compared with stocks in other countries, Trump’s April policy has a limited impact on Japanese stocks.

Looking forward, with tariff headwinds fading and limited downside even if tariffs escalate and Japan’s economic recovery, we remain bullish on Japanese equities (Figure 5). As noted in the Exchange Rate section, we predict short-term yen appreciation. Will this hurt stocks? Our answer is “not in the short term”. This is because recent shifts in Japan’s monetary policy, stock valuations and the yen’s nature suggest the historical negative stock-yen correlation could turn positive (see “Japan: Believe in Long-Term Recovery. Buy!, published January 21, 2025”).

Figure 5: Nikkei 225

Source: Refinitiv, Tradingkey.com

Recommended Articles