Understanding CBOE Volatility Index & How to Trade the VIX

TradingKey - During periods of turbulence in global capital markets, the CBOE VIX Index frequently makes headlines in major media outlets. Commonly viewed as a forward-looking indicator for U.S. equities, the VIX has historically spiked ahead of sharp declines in stock markets—highlighting its role as a gauge of investor fear.

Ahead of the implementation of "reciprocal tariffs" set to take effect on April 2 by the 47th U.S. President, Donald Trump, the VIX surged approximately 30% over four consecutive days, drawing significant attention from investors.

In the early days of Trump's second administration, a sense of "uncertainty" persisted among U.S. government officials—including those at the Federal Reserve—Wall Street analysts, and the broader investment community. Reflecting this unease, gold prices hit record highs at least ten times in the first quarter of 2025. In addition to gold, trading products linked to the VIX index have emerged as a popular tool for investors seeking to hedge against rising market risks.

The VIX (Volatility Index) was created by the Chicago Board Options Exchange (CBOE) in 1993 to measure expectations of the S&P 500's volatility over the next 30 trading days. Its full name is the CBOE Market Volatility Index.

The VIX is calculated using the implied volatility of S&P 500 index options, reflecting investor expectations of future market fluctuations. It is recognized as the world’s first quantitative indicator of market volatility expectations.

Globally, the VIX is regarded as a "barometer of market sentiment" and is known for its forward-looking nature. A higher VIX reading indicates greater investor concern about potential market turbulence. While there is generally an inverse relationship between the VIX and stock market performance—meaning the VIX tends to rise when equities fall and vice versa— this correlation is not always consistent.

Importantly, the VIX measures the expected magnitude of market fluctuations, not the direction of the S&P 500 movement.

The VIX is calculated by collecting option prices on the S&P 500, computing the implied volatility for the nearest and second-nearest monthly expirations, constructing a variance curve, and then adjusting the result on an annualized basis to derive the market's expectation of volatility over the next 30 days.

- Option Selection: Near-term (23 to 37 days until expiration) and second-month call (Call) and put (Put) options, covering all strike prices.

- Implied Volatility Calculation: Reverse-engineering the market's expectations of future volatility based on option prices.

- Weighted Average: Combining option prices, strike prices, and expiration times to calculate variance and annualize it, ultimately deriving the VIX value.

The calculation of the VIX involves a complex formula, but the core idea is straightforward: it uses price data from the options market to infer investors’ expectations of future volatility.

The VIX is quoted in percentage points and assumes a normal distribution. For example, when the VIX is at 20, it indicates that the expected annualized volatility of the S&P 500 over the next 30 days is 20%. This translates to a 30-day volatility of: 20%/√12 = 5.77%. It implies a 68% probability that the S&P 500 will fluctuate within ±5.77% over the next 30 days.

According to S&P Global, the VIX ranges can be interpreted as follows:

- 0–15 (Low): Calm and optimistic market sentiment.

- 15–20 (Moderate): Normal sentiment.

- 20–25 (Medium): Rising concern.

- 25–30 (High): Increasing market volatility.

- Above 30 (Extreme High): Extreme market volatility and panic.

Historically, a VIX reading below 20 suggests market stability and calm investor sentiment, while values above 30 are typically associated with elevated fear, uncertainty, and heightened market volatility.

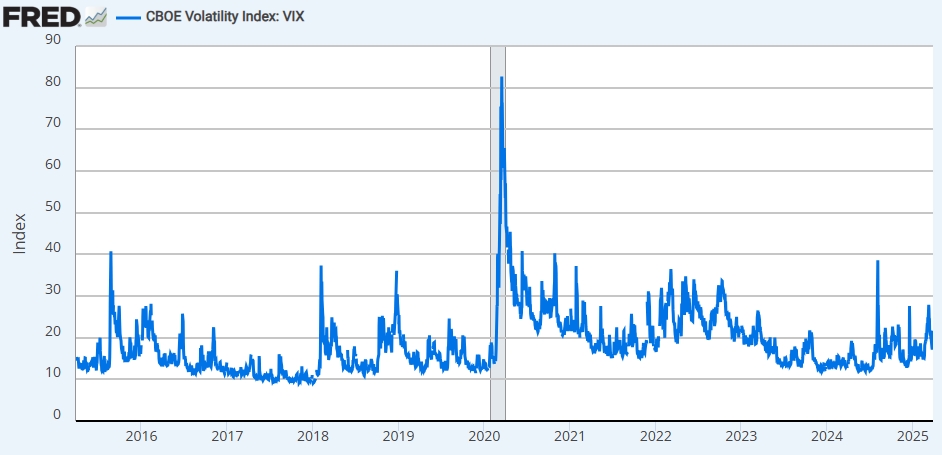

CBOE VIX Index, Source: Stlouisfed

Not necessarily. The relationship between the VIX and the stock market is not perfectly or consistently inverse.

- Increased Volatility After Sharp Rebound

During the recovery phase following a market crash, both the VIX and stock prices can rise simultaneously. For example, between March and April 2020, after the Federal Reserve introduced massive stimulus measures, the S&P 500 rebounded while the VIX remained elevated above 40. - Sideways Movement Amid High Volatility

In high-volatility environments, investors often struggle to find clear direction amid fluctuating economic data and shifting policy signals. While overall market uncertainty increases, this does not always translate into a one-sided market decline. - Diverging Investor Sentiment

When market outlooks become highly polarized, demand for both bullish and bearish options rises, pushing the VIX higher. In such cases, stock market performance ultimately depends on the balance of power between bulls and bears.

- Quantitative Tool for Market Sentiment

Changes in the VIX intuitively reflect investor panic or greed, helping to identify market turning points. - Risk Warning Mechanism

The long-term average of the VIX is 19.5. Breaking above 20 signals increasing market volatility, while breaking above 40 indicates extreme panic. - Contrarian Indicator

Historically, VIX peaks often correspond to stock market bottoms, presenting contrarian investment opportunities. - Risk Management

High VIX levels are accompanied by sharp market swings. Investors can use VIX-related products to hedge their risk exposure and reduce potential losses.

- Not a Directional Predictor

The VIX reflects expectations of market volatility but does not indicate the direction of price movement. High readings can accompany either significant gains or losses. - Short-Term Effectiveness

The VIX is better suited for capturing near-term market movements and is highly sensitive to short-term sentiment shifts, such as news releases and economic data announcements. Long-term analysis should be used in conjunction with fundamental factors. - No Causal Relationship

The VIX is a result of market volatility, not its cause. Judging stock market trends requires considering other factors. - Overreaction

During extreme events—such as financial crises or geopolitical conflicts—the VIX can spike rapidly, though it may sometimes exaggerate short-term risks. - Mean Reversion

The VIX exhibits strong mean-reverting behavior: extremely high levels tend to revert downward, while extremely low levels typically rebound. - Model Assumptions

The VIX is calculated based on the Black-Scholes option pricing model, although some of its underlying assumptions are difficult to achieve in practice.

- 2008 Global Financial Crisis

During the 2008 financial crisis, the collapse of Lehman Brothers, the bursting of the real estate bubble, and the freezing of credit markets triggered extreme stock market volatility. Investors rushed to buy put options to hedge their exposure, pushing the VIX to a record high of 89.53 on October 24, 2008. The S&P 500 fell nearly 40% between October 2008 and March 2009. - 2011 European Debt Crisis

In 2011, Europe experienced a sovereign debt crisis, with Greece, Spain, and other countries burdened by unsustainable debt levels, threatening the stability of the eurozone and the broader global financial system. The VIX index surged to 48 on August 8, 2011, and the S&P 500 dropped more than 21% that month. - 2020 COVID-19 Market Crash

In early 2020, the global outbreak of COVID-19 brought economic activity to a near halt, triggering widespread panic across financial markets. The VIX index reached its second-highest historical level of 82.69 on March 16, 2020, while the S&P 500 plummeted 35% during that month.

Conversely, periods of low volatility and market calm are also reflected in the VIX. In 2017, strong global economic growth and accommodative central bank policies kept the VIX hovering around 10, while the S&P 500 posted a 20% annual gain.

The VIX index is a calculated index and cannot be traded directly. However, the development of financial instruments such as futures, options, and ETFs has made it possible for investors to gain indirect exposure to VIX movements.

- VIX Futures: Standardized futures contracts based on the VIX, introduced by the CBOE in March 2004.

- VIX Options: Option contracts based on VIX futures, allowing investors to buy or sell VIX futures at specific prices.

- VIX ETFs: Well-known VIX ETFs include ProShares’ VIXY (long), UVXY (1.5x long), SVXY (0.5x short), and Volatility Shares’ SVIX (short).

- VIX ETNs: Typical VIX exchange-traded notes include Barclays iPath’s VXX (short-term long) and VXN (medium-term long).

- Hedging Market Risk

When economic data weakens or specific events raise expectations of heightened market volatility or stock declines, investors can go long on the VIX—by purchasing VIX call options, VIX futures, or VXX—to hedge against risks in their equity positions. - Mean Reversion Strategy

Given the VIX’s tendency to revert to its long-term average (18–20), opportunities for reversion may arise: - When the VIX is extremely high, expect market stability or a rebound. Use a short-volatility strategy (sell VIX futures, sell VIX call options, short VXX, or buy SVIX).

- When the VIX is extremely low, expect increased market volatility. Use a long-volatility strategy (buy VIX call options or buy VXX).

For experienced investors, advanced strategies include futures term structure arbitrage (e.g., exploiting contango or backwardation conditions) and volatility skew trading, which involves arbitraging differences in implied volatility across various strike prices.

Recommended Articles