February PCE Inflation Preview: Short-Term Concerns Overblown, Tariffs Remain the Focus

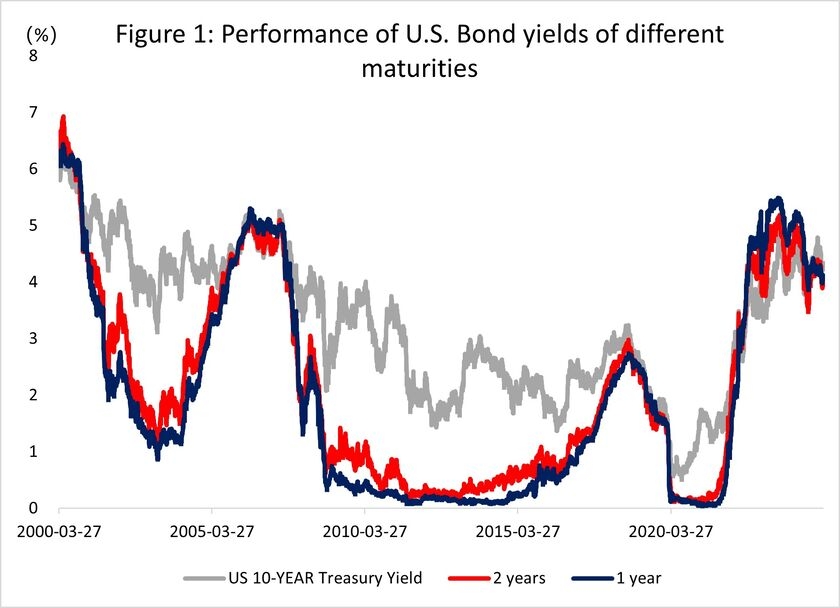

TradingKey——Following the Fed’s decision last week to hold rates steady while slowing its QT,Donald Trump also emphasized the "flexibility" and "negotiability" of the current tariff policies in an effort to ease excessive markettension. As a result of these two developments, the U.S. stock market stabilized and rebounded in the short term. The 10-year U.S. Treasury yield rose gradually, but the 1-year and 2-year yields underperformed —reflecting continued pessimism in the market regarding future inflation driven by tariffs and the risk of an economic recession. This week, investor focus is shifting to the U.S. Department of Commerce's upcoming release of the February PCE price index on Friday (March 28). However,we believe this data is unlikely to become the focal point of short-term market trading, as the core driving variables have not yet emerged.

Our reasons are as follows:

PCE Price Volatility and Expectations Already "Priced In"

While CPI and PCE trends have historically aligned over the long term, February’s CPI subcomponents showed that cooling inflation was driven primarily by energy, housing, and transportation services. In contrast, the PCE index assigns less weight to these categories and places greater emphasis on durable goods and healthcare services. As a result, February’s PCE and Core PCE readings are likely to diverge from CPI trends. Market consensus expects headline PCE growth to remain steady at 2.5% year-over-year (YoY), while Core PCE is projected to edge up slightly to 2.7% YoY.

Data Sources: Reuters, TradingKey As of: March 26, 2025

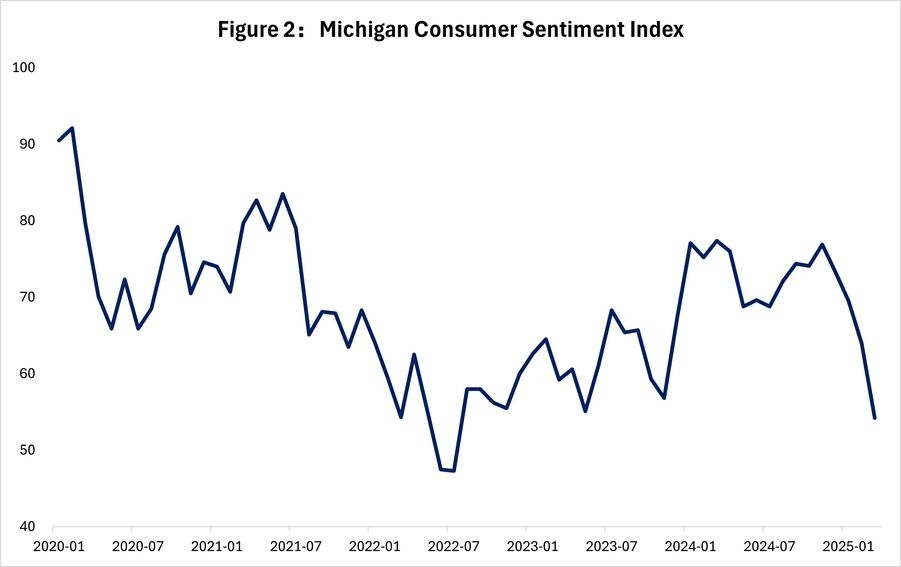

Consumer Sentiment Weakens, but Economic Resilience Persists

Aggressive tariff rhetoric from the Trump administration and widespread corporate layoffs have dampened U.S. consumer confidence for several consecutive months. However, the economy remains resilient, supported by a robust labor market and healthy household balance sheets.

Despite a modest increase over the past year, the unemployment rate remains near pre-pandemic levels, while private-sector wages and disposable income continue to grow steadily. Elevated household net worth— buoyed by sustained strength in equities and real estate—further supports overall economic stability.

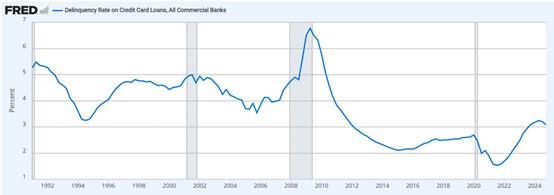

From a debt perspective, mortgage interest payments accounted for less than 5% of disposable income by the end of 2024, and credit card delinquency rates hovered around 3%, mirroring levels seen before the pandemic. Households have largely mitigated the impact of high-interest debt through refinancing strategies employed during thepost-pandemic period.

Figure 3 : Delinquency Rate on Credit Card Loans

Data Sources: Reuters, Federal Reserve Bank of St. Louis and TradingKey As of: March 26, 2025

Trump’s "Tariff Stick" Emerges as the Core Variable

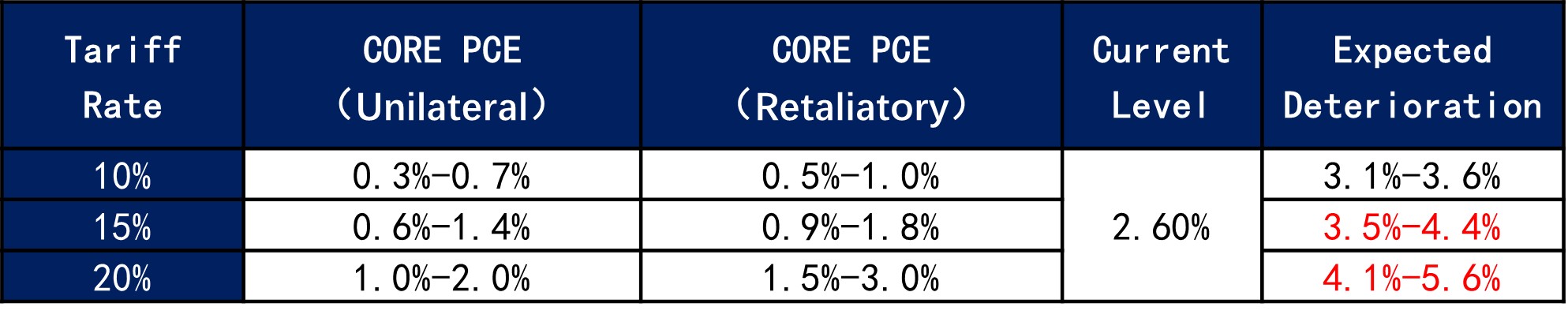

Unlike the “targeted”(mainly referred to China) approach of his first term, Trump’s current trade strategy leans toward "universalization," with the initial tariff phase focusing on Canada and Mexico—the U.S.’s top trading partners—before potentially shifting to China. Sensitivity analysis,based on historical tariff impacts,suggests that across scenarios (10%, 15%, and 20% baseline tariffs), inflation would rise proportionally. If trading partners retaliate with equivalent measures—a likely outcome given current tensions—global supply chains could be disrupted, further exacerbating price pressures.

For example, a 15%+ universal tariff could push headline PCE to 3.5% and Core PCE to 3%, significantly exceeding the Fed’s 2025 forecast of 2.5% and potentially triggering policy tightening.

Elevated inflation would likely dampen consumer spending, compress corporate profits, and destabilize equity valuations amid higher rates and slower growth. In such a scenario,U.S. stocks could face revaluation under a "triple squeeze" of high inflation, elevated rates, and stagnating earnings.

Table 1: Sensitivity Analysis of U.S. Inflation Performance Under Different Tariff Rates

Data Source: TradingKey As of: March 26, 2025

Conclusion

Therefore, investors should closely monitor the implementation of reciprocal tariffs on April 2, as this development is likely to have a greater impact on markets than the upcoming release of the February PCE data, which is unlikely to materially influence the Federal Reserve’s future interest rate path and is likely already priced in by the market.

Although Trump is often seen as a symbol of uncertainty, his team has recently stated in public media that they are willing to"accept market declines and even allow a short-term economic recession."

However, Trump’s well-known negotiating philosophy of “everything is negotiable”may leave a glimmer of hope for easing potentially disastrous tariffs. At the same time, market overreactions have begun to constrain his policy flexibility, tying his hands to some extent.

Recommended Articles