[IN-DEPTH ANALYSIS] Gold: Will Tariffs Push Gold Prices Down? No, They Will Only Benefit Gold

Executive Summary

With the continuous rise in gold prices and the sharp drop in gold prices at the beginning of the "reciprocal tariffs" announcement, many economists, analysts and investors expect that the turning point of the gold price trend has arrived. This article studies the trend of gold prices from three perspectives caused by tariffs (gold's monetary properties, U.S. stagflation risks and global central bank holdings) as well as the scale of U.S. debt and real interest rates. Through comprehensive analysis, we believe that gold prices still have room to rise.

Source: Refinitiv, Tradingkey.com

* Investors can directly or indirectly invest in the gold market through physical gold, gold stocks, passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Introduction

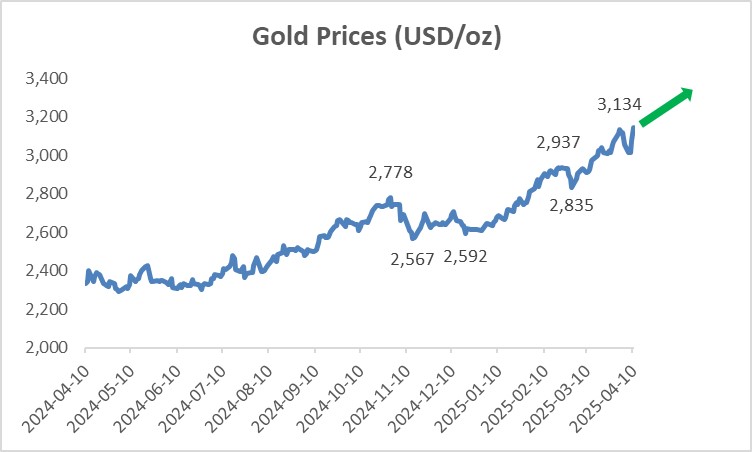

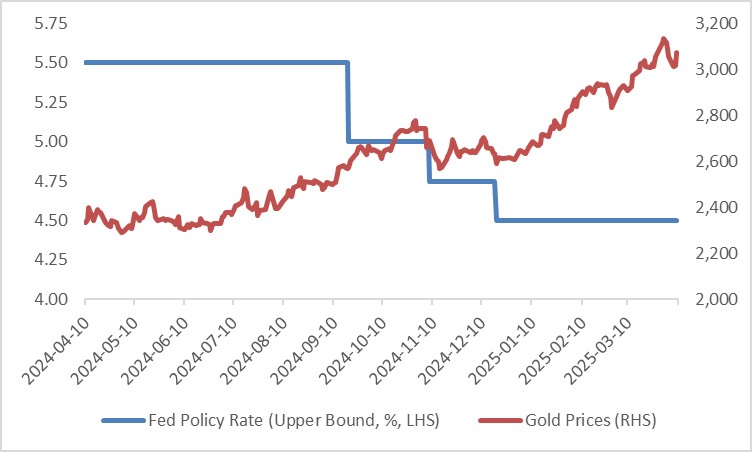

Since the beginning of last year, the price of gold has risen by 51.6% to its highest point on 1 April this year. However, recently gold prices have fluctuated sharply due to the release of Trump's "reciprocal tariffs". This is mainly due to the influence of both positive and negative driving forces. On the one hand, high tariffs are leading to a slowdown in global economic growth and gold will show its safe-haven standard, which benefits its prices. On the other hand, additional tariffs have caused a recent stock market drop and investors have sold gold to raise capital to make up for losses in assets such as stocks. In addition, Federal Reserve Chairman Powell warned that high tariffs may lead to the risk of re-inflation. This warning has made investors expect that the Federal Reserve is less likely to cut interest rates sharply, further suppressing the price of gold (Figure 1). Looking ahead, will the net impact of high tariffs on gold prices be positive or negative? This article starts with "reciprocal tariffs" and analyses other factors to study and predict future gold prices.

Figure 1: Fed Policy Rate and Gold Prices

Source: Refinitiv, Tradingkey.com

2. The release of "reciprocal tariffs"

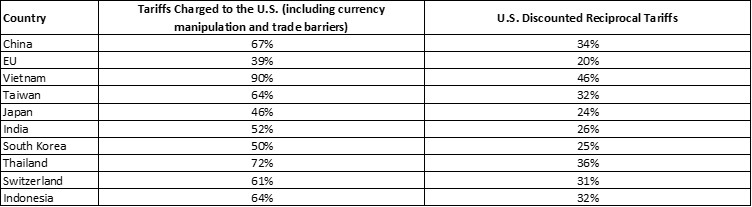

On 2 April, Trump signed an executive order to implement a comprehensive new reciprocal tariff policy, with about 100 countries on its list. There are two types of new tariffs: First, from 5 April, a tariff of at least 10% would be imposed on all imported goods. The countries only subject to this base tariff include the United Kingdom, Singapore, Brazil, Australia, New Zealand, Turkey, Colombia, Argentina, El Salvador, the United Arab Emirates and Saudi Arabia. Second, from 9 April, higher tariffs would be imposed on "worst offenders". Figure 2 gives examples of the worst offenders and the additional tariffs imposed on them. The scale of this "reciprocal tariff" policy has increased by more than expected and is seen as the largest change in the international trade order since the end of World War II. Although Trump suspended new tariffs on most countries for 90 days on 9 April, we believe that high tariffs are the main theme of the current global situation and are difficult to reverse fundamentally.

Figure 2: Examples of Worst Offenders

Source: Refinitiv, Tradingkey.com

3. Tariff Perspective I: Gold’s Monetary Properties

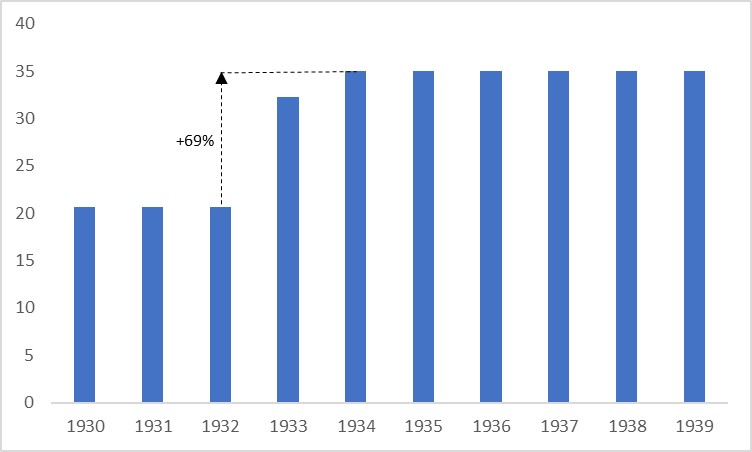

The essence of imposing tariffs is to raise the prices of imported goods so that consumers buy more American-made goods. From an economic perspective, this is a disguised way to depress the domestic currency relative to goods. As gold is denominated in US dollars, the decline in the purchasing power of the US dollar will push up the price of gold. If trading partners take countermeasures (a high probability event) and impose tariffs on each other, the purchasing power of other currencies will depreciate in disguise. This will further lead to higher gold prices. In extreme cases, the 1933-1934 gold price jump may be repeated, although there is no constraint on the gold standard currently (Figure 3).

Figure 3: Gold Prices in the 1930s (USD/oz)

Source: Refinitiv, Tradingkey.com

4. Tariff Perspective II: The US faces the risk of stagflation

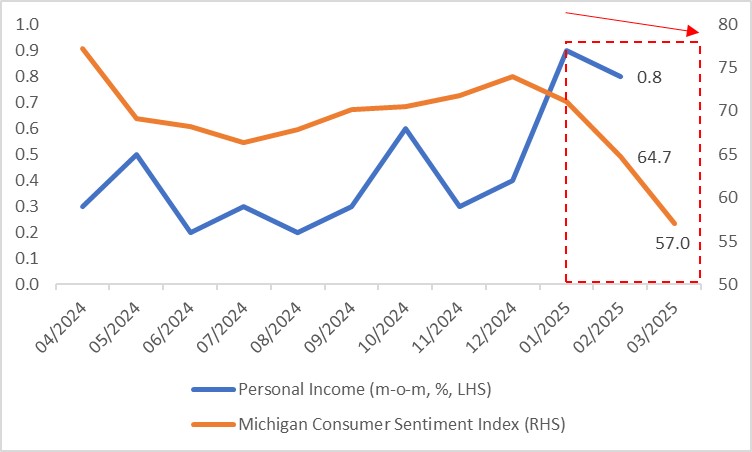

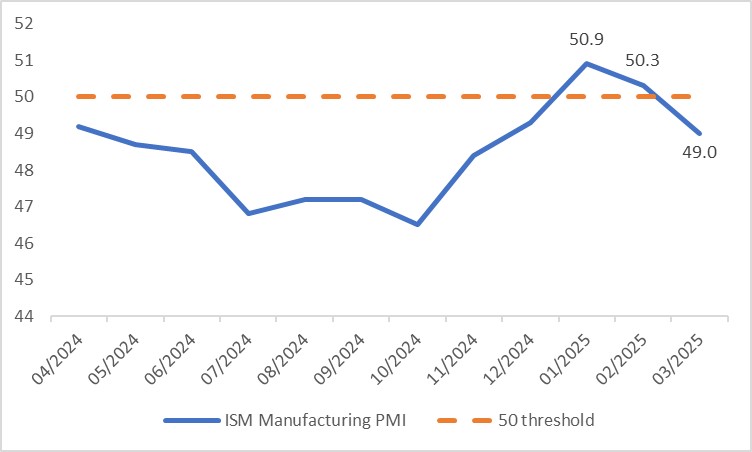

The tariffs imposed by the United States on Canada, Mexico and China at the beginning of this year as well as the "reciprocal tariffs" announced by Trump on 2 April, plus the retaliatory tariffs of trading partners will lead to the risk of stagflation in the United States. The so-called stagflation refers to low growth and high inflation. In terms of growth, the slowdown in personal income growth on the income side dragged down the Michigan Consumer Confidence Index and the year-on-year growth rate of retail sales on the consumer side fell from 4.2% in January to 3.1% in February (Figure 4.1). This consumption weakness has been transmitted to the production side and the ISM manufacturing PMI fell below the 50 threshold in March (Figure 4.2). It is expected that this deteriorating consumption-production cycle will continue.

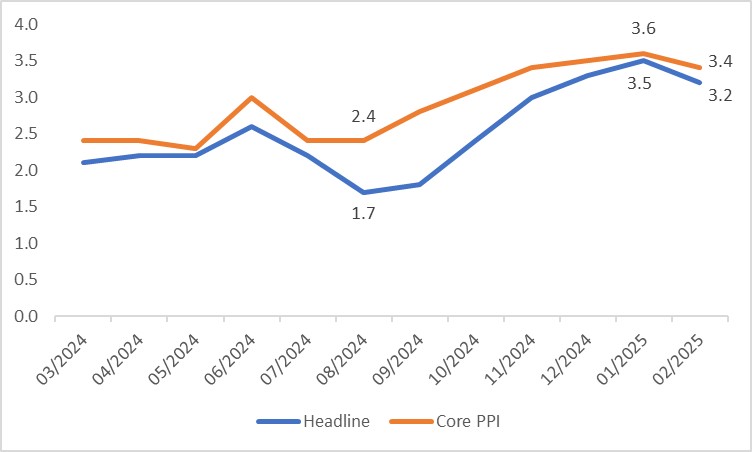

In terms of inflation, tariffs have not yet been significantly transmitted to CPI, but have pushed up the producer price index (PPI). Although PPI fell slightly in February, the upward trend of the headline and core PPI has not changed (Figure 4.3). In the future, if producers pass on costs to consumers, CPI may face upward pressure in the coming months.

One aspect of stagflation - low growth will cause gold to show its safe-haven properties. On the other aspect, high inflation will make gold show its value-preserving properties. In short, against the backdrop of increasing stagflation risks, gold prices may continue going up.

Figure 4.1: U.S. Personal Income and Michigan Consumer Sentiment Index

Source: Refinitiv, Tradingkey.com

Figure 4.2: U.S. ISM Manufacturing PMI

Source: Refinitiv, Tradingkey.com

Figure 4.3: U.S. PPI (y-o-y, %)

Source: Refinitiv, Tradingkey.com

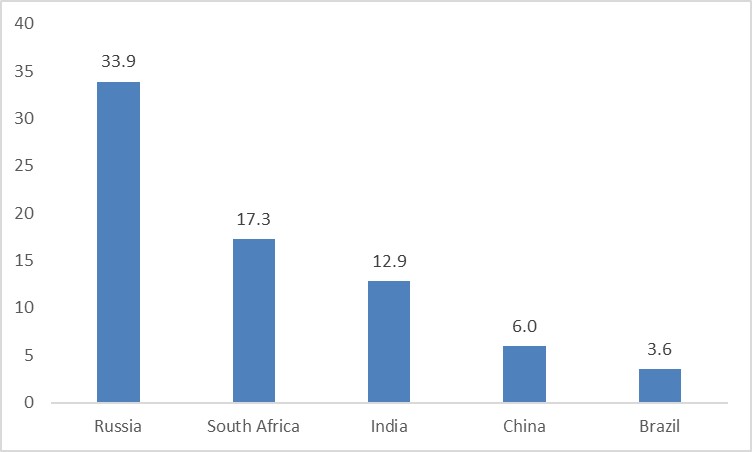

5. Tariff Perspective III: Global Central Banks Increase Gold Reserves

The current global monetary system dominated by the US dollar is showing cracks. There are two reasons: 1) The introduction of "reciprocal tariffs" has led to a weakening of trading partners' confidence in the US dollar's status as a global reserve currency; 2) The United States froze Russia's dollar assets due to the Russia-Ukraine war, which caused other countries to worry that the same thing might happen in their countries in the future.

The shaky status of the US dollar has directly led to central banks in various countries increasing their holdings of gold as a reserve asset. With the continuous increase in holdings, the proportion of gold in the reserve assets of developed countries has reached about 27%. Although developing countries are only about 9%, the increase in holdings in recent years is much higher than that of developed countries. In terms of volume, the Polish Central Bank purchased 90 tons of gold in 2024, becoming the world's largest buyer. In the same year, China purchased 44 tons. In terms of reserve share, the Reserve Bank of India has increased its gold reserves from 8.1% to 12.9% in the past two years (Figures 5.1 and 5.2). If the central bank's purchases continue, this will continue to push up gold prices from the demand side. It is worth noting that as the proportion of gold held by global central banks increases, their willingness to continue to increase their holdings will decrease. This is coupled with the fact that central banks are continuing to increase their holdings of Crypto. Therefore, the impact of this tariff perspective on gold may be smaller than the Tariff Perspective I and II mentioned previously.

Figure 5.1: Global Central Bank Gold Reserves (thousand tonnes)

Source: Refinitiv, Tradingkey.com

Figure 5.2: Gold (% of foreign reserves)

Source: Refinitiv, Tradingkey.com

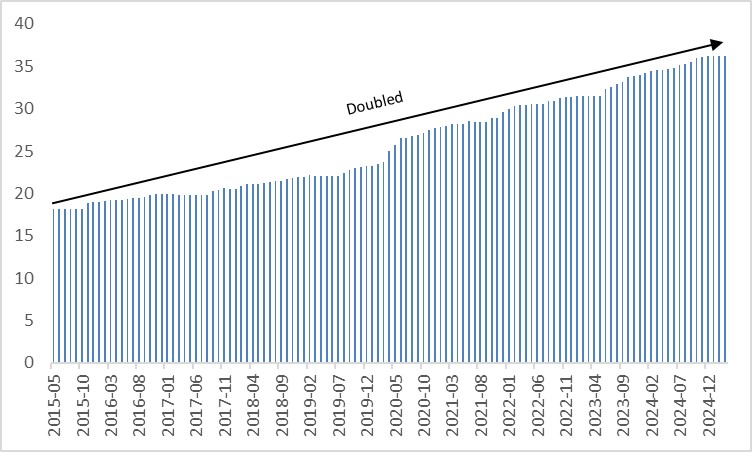

6. Additional Perspective I: The Massive Scale of U.S. Debt

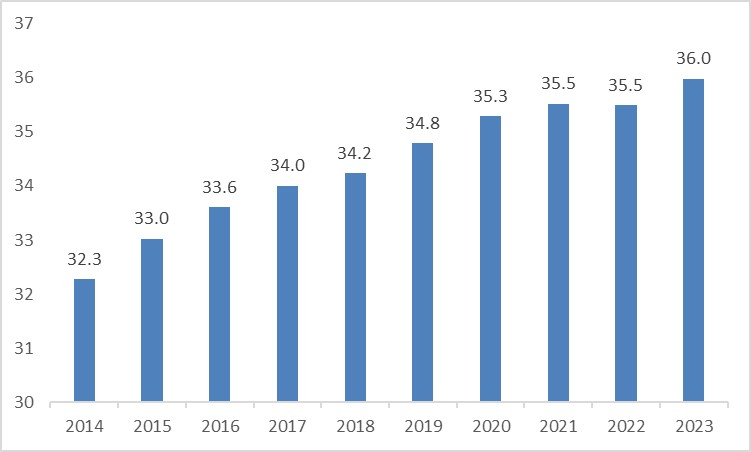

The dominance of the U.S. dollar as the global reserve currency is declining year by year, mainly due to the continued rise in U.S. debt. By the end of March 2025, Total U.S. National Debt reached an unprecedented high of $36.2 trillion. Compared with 10 years ago, this figure has doubled (Figure 6). Its interest expenditure has also exceeded defence expenditure. Looking forward, if the U.S. government takes further tax cuts, it is expected that the U.S. National Debt will continue to increase. The continuous rise in U.S. debt has made investors worry about its sustainability. Central banks, governments and investors are increasingly eager to find alternatives to U.S. dollar assets and gold is undoubtedly one of the best alternative assets.

Figure 6: Total U.S. National Debt (trillion USD)

Source: Refinitiv, Tradingkey.com

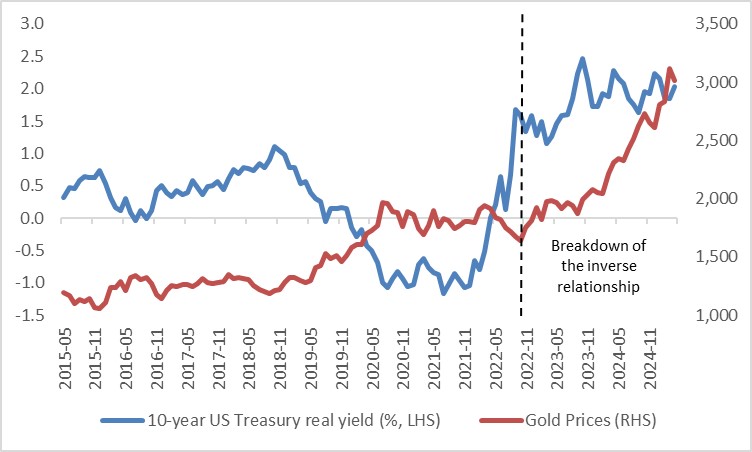

7. Additional Perspective II: Real Interest Rates

In theory, the real interest rate is equivalent to the opportunity cost of holding gold. When the interest rate falls, the opportunity cost of holding gold is lower, which provides support for the gold prices and vice versa. In history, when stagflation appeared, the Federal Reserve often adopted a tight monetary policy to fight inflation first. In the current economic context, the Federal Reserve is likely to slow down the rate cuts (the possibility of rate hikes is not high). Under the influence of high inflation, the real interest rate will fall, which may benefit gold prices. However, it is worth noting that after 2022, the real interest rate has had less impact on gold prices (Figure 7). Therefore, as mentioned above, the main reasons for our bullish view on gold are still high tariffs, stagflation and high debt.

Figure 7: U.S. Treasury Real Yield and Gold Prices

Source: Refinitiv, Tradingkey.com

Recommended Articles